Binance

Binance Hyperliquid

Hyperliquid Kraken

Kraken BingX

BingX ADA

ADA DOGE

DOGE LINK

LINK TAO

TAO TRX

TRX XMR

XMR ZEC

ZECWhat Are Crypto Funding Rates?

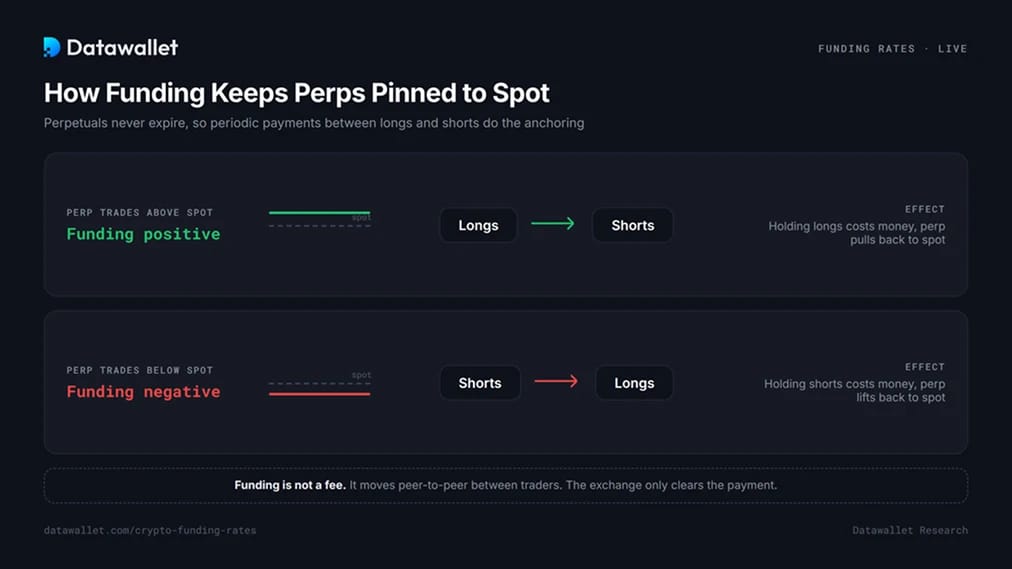

A funding rate is the periodic payment exchanged between long and short traders on a perpetual futures contract. Perpetuals never expire, so no settlement date forces the contract price back to spot. Funding does that job instead.

When the perpetual trades above the spot index, longs pay shorts, making longs expensive to hold and pulling the contract back toward spot. When it trades below, shorts pay longs and the pressure reverses. The payment moves between traders; the exchange only clears it. Funding is not a fee.

Because positioning sets the rate, it doubles as one of the cleanest sentiment gauges in crypto. The table above is a live map of who is paying whom, per coin, per venue.

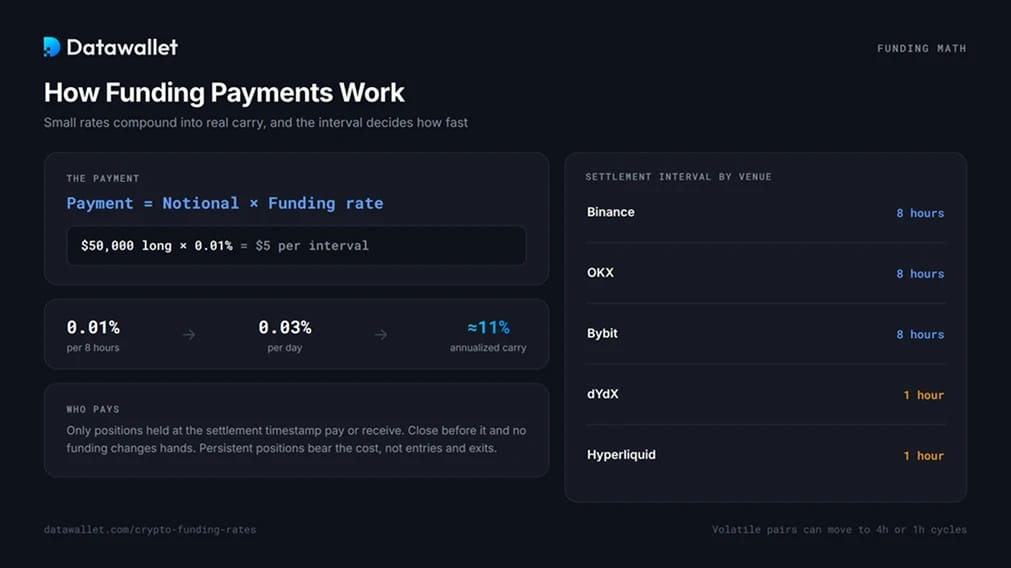

How Funding Payments Work

The payment is position notional multiplied by the funding rate at settlement. A $50,000 BTC long at 0.01% pays $5 to the short side that interval. Held through three settlements a day, small rates become real carry: 0.01% every 8 hours is roughly 11% annualized.

Three details matter in practice:

- Intervals differ by venue. Binance, OKX, and Bybit settle every 8 hours as standard, with volatile pairs sometimes moved to 4-hour or 1-hour cycles. dYdX and Hyperliquid settle hourly, so the same quoted rate costs three times as much per day if it persists.

- Only holders at the timestamp pay or receive. Close before settlement and no funding changes hands. Persistent positions bear the cost, not entries and exits.

- The rate has two components. Most exchanges combine a premium index, measuring the perp's gap to spot, with a fixed interest component of typically 0.01% per interval. That is why rates cluster near 0.01% in calm markets rather than at zero.

Positive vs Negative Funding Rates

Positive funding means the perpetual trades above spot and longs pay shorts. Mildly positive is crypto's neutral state, since leveraged traders skew long by default. Persistently elevated rates flag crowded longs, and extreme readings have historically clustered near local tops, where one sharp dip cascades through over-leveraged positions. Our Bitcoin liquidation heatmap shows where that leverage would clear.

Negative funding means the perpetual trades below spot and shorts pay longs. It signals bearish positioning, hedging demand, or both. Deeply negative rates are rarer and less stable than their positive mirror: a crowded short book pays to stay short, and any bounce forces covering that accelerates the move. Crypto's most violent rallies routinely start from deeply negative funding.

Neither sign is a trade on its own. The rate shows where the crowd is, and the crowd is right during trends and wrong at extremes.

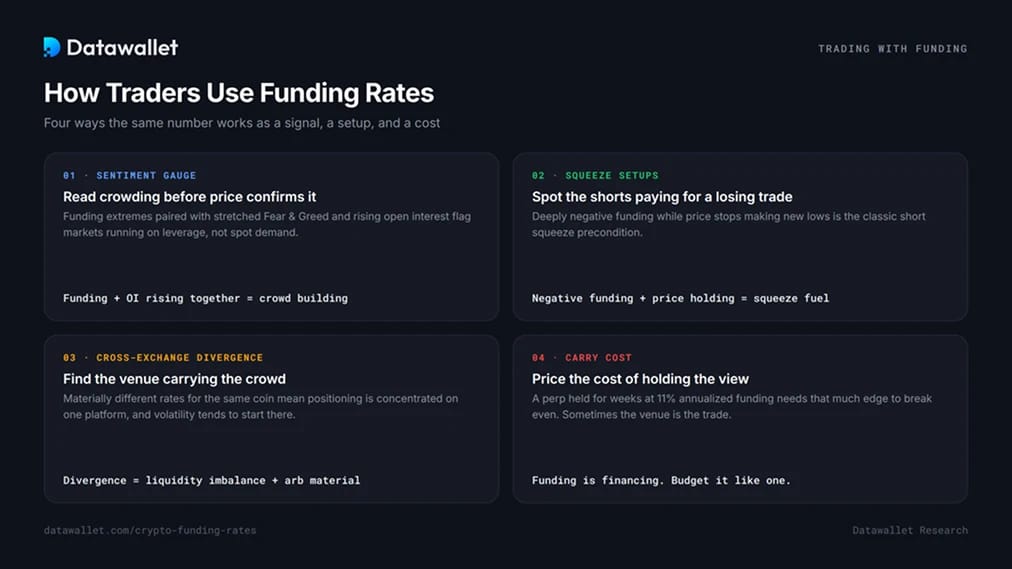

How Traders Use Funding Rates

- Sentiment and crowding gauge. Funding extremes paired with stretched Fear and Greed readings flag markets running on leverage rather than spot demand. Rising open interest alongside extreme funding confirms new leveraged money piling into the crowded side.

- Squeeze setups. Deeply negative funding while price stops making new lows is the classic short squeeze precondition: shorts are paying to hold a position that has stopped working.

- Cross-exchange divergence. Materially different rates for the same coin mean positioning is concentrated on one venue. Divergence often precedes volatility on the platform carrying the crowded side, and feeds the arbitrage below.

- Carry cost management. A perp held for weeks at 11% annualized funding needs that much edge just to break even, sometimes reason enough to choose a cheaper venue. Fee and funding structures vary widely across the best crypto futures exchanges.

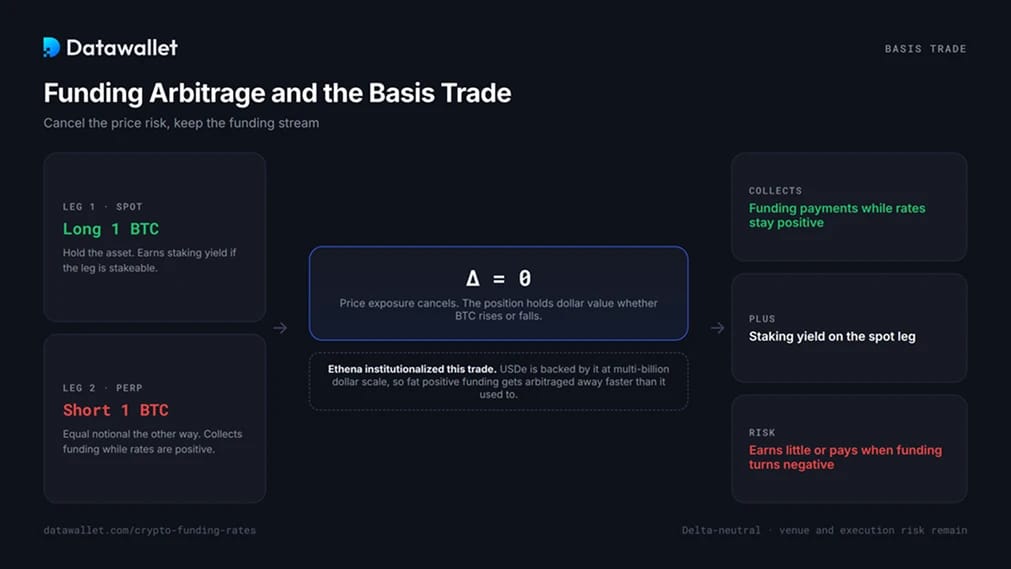

Funding Arbitrage and the Basis Trade

Funding payments are an income stream, and a whole corner of the market exists to harvest them. The cash-and-carry basis trade buys the asset in spot and shorts equal notional in perps. Price exposure cancels, and the position collects funding while rates stay positive, plus staking yield if the spot leg is stakeable.

Ethena institutionalized this trade: its USDe synthetic dollar is backed by exactly this structure at multi-billion dollar scale, paying harvested funding to sUSDe holders. The consequence for everyone else is that positive funding gets arbitraged away faster, and returns on the trade have compressed as funding cooled from its late-2024 highs. The same structure runs on the best perp DEXs, where settlement is hourly.

The cross-exchange version, long where funding is negative and short where it is positive, carries venue and execution risk but no directional exposure. The divergences in the table above are where it starts.

The 2026 Funding Regime

Funding through 2026 has spent long stretches negative across majors, reversing the structurally positive regime of the 2024 bull phase. Negative BTC, ETH, and SOL rates across most venues reflect a market paying for downside protection and momentum shorts rather than leveraged upside.

Two implications follow. Position traders holding longs are being paid to wait, which lowers the cost of patient accumulation but says nothing about timing. Carry traders earn little or pay when funding is negative, which is why delta-neutral yields compress in bear phases, and why funding flipping back to sustained positive territory is itself an early regime signal worth watching on this page.

Final Thoughts

Funding rates are the perpetual market's price of conviction: a live measure of which side is crowded and what it pays for the privilege. Read them as carry when you hold, sentiment when you wait, and raw material when you arbitrage. Tracked across venues alongside open interest and liquidation structure, funding gives a fuller picture of market leverage than price alone ever will.

Frequently Asked Questions

How often are funding rates paid?

Every 8 hours on most centralized exchanges, at fixed UTC timestamps. Some venues move volatile pairs to 4-hour or 1-hour intervals, and dYdX and Hyperliquid settle hourly. You only pay or receive if you hold the position at settlement.

Is the funding rate a fee charged by the exchange?

No. Funding is a peer-to-peer transfer between longs and shorts. The exchange calculates and clears it but keeps nothing. Trading fees are separate.

What is a normal funding rate?

Around 0.01% per 8-hour interval, the baseline built into most exchange formulas. Rates persistently several multiples above that signal crowded longs; sustained negative rates signal crowded shorts. Persistence matters more than any single print.

Why do funding rates differ between exchanges?

Each venue calculates funding from its own order book, so the rate reflects positioning on that exchange. A coin can be net long on one platform and net short on another, the exact divergence arbitrageurs trade away.

Do funding rates affect spot holders?

Not directly, since funding only applies to perpetual positions. Indirectly, extreme funding drives the liquidation cascades and squeezes that move spot price, which is why spot traders watch it too.

Can you earn yield from funding rates?

Yes, through the basis trade: long spot, short equal notional in perps, collecting funding while price exposure cancels. Returns depend on funding staying positive, and the trade earns little or loses during negative regimes like much of 2026.