Compare Top Swiss Crypto Exchanges

1. Bybit

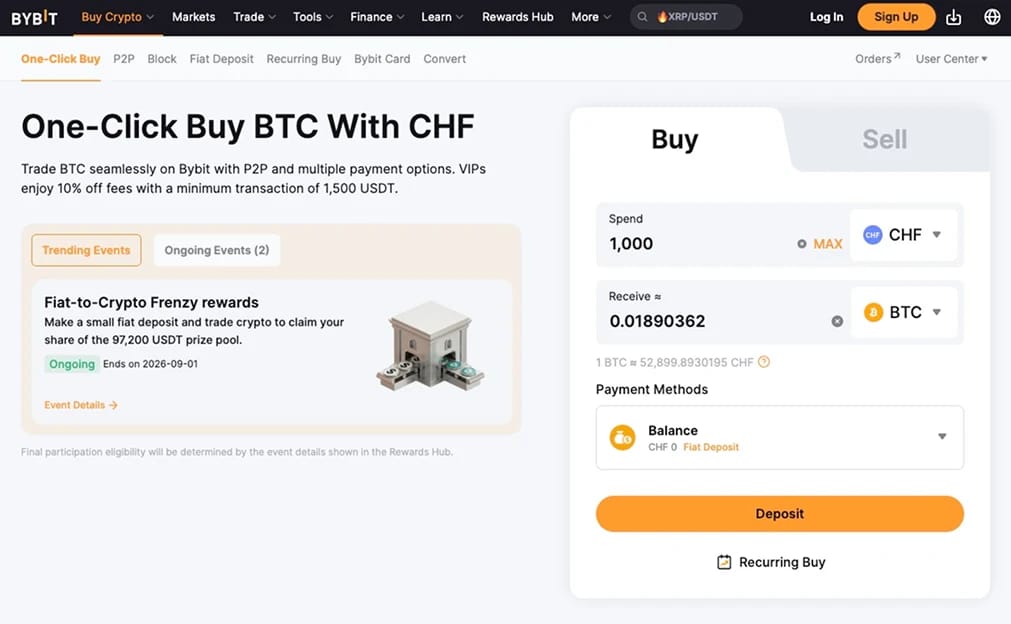

Bybit takes the top spot for sheer capability, since no platform a Swiss user can open matches it for range. It lists 2,800+ assets across spot, perpetuals, and options at a flat 0.1% spot fee, then layers copy trading, grid bots, and Bybit Earn on top. Switzerland is outside Bybit's restricted list, so a standard global account can be opened without using Bybit.eu, and the depth covers everything from a first Bitcoin buy to futures trading in one place.

Funding is more flexible than Bybit's reputation suggests. Swiss users can deposit CHF directly via zen.com's payment partner, alongside SEPA for euros, cards, Apple Pay, Google Pay, and Samsung Pay. We linked a zen.com account and funded CHF in one click, with the balance tradable within minutes at a markup well below a card buy. Cards and one-click purchases work too, at a spread closer to 2%.

Two things are worth considering. Bybit holds no FINMA authorization, so a dispute leaves you with the platform's own support and nothing local behind it; however, Bybit does hold a MiCA license to operate across Europe. Every swap also counts as a disposal, so export your trade history regularly rather than rebuilding a year's worth later. Our Bybit review covers the wider product set.

Pros

- 2,800+ assets across spot, futures, options, copy trading, and Earn at 0.1% fees.

- Direct CHF deposits via zen.com, plus SEPA, cards, Apple Pay, Google Pay, and Samsung Pay.

- Monthly Proof-of-Reserves audits back customer balances on a 1:1 basis.

Cons

- The CHF rail runs through zen.com, a separate provider you link before funding.

- No FINMA licence, leaving no Swiss regulator behind the platform.

- The derivatives-first layout nudges new users toward leverage.

2. Kraken

Kraken is the pick for Swiss users who rank custody safety above coin count, and it backs that with the cleanest funding setup for the franc. The exchange has operated since 2011 without a major breach, publishes Proof-of-Reserves audits confirming client balances are backed 1:1, and keeps most assets in cold storage. For anyone parking a meaningful amount on an exchange rather than in self-custody, that record carries real weight.

The funding advantage is specific to Switzerland. Through its partnership with Bank Frick in Liechtenstein, Kraken accepts direct CHF transfers over the SIC system, settles them in real time during banking hours, and lets you trade against CHF or an EUR/CHF pair. Our CHF test deposit from a Swiss account arrived as tradable francs the same business day, and the withdrawal back cleared without an FX leg.

Kraken Pro offers spot pricing at 0.40% maker and 0.80% taker on base volume across 475+ assets, with staking and an OTC desk for size. The full breakdown sits in our Kraken review. The only downside is that the listing policy is conservative, so newer small caps arrive late or never, and the instant-buy screen outside Kraken Pro carries a spread that a limit order avoids.

Pros

- A 14-year operating record with audited 1:1 reserves and cold storage.

- Direct CHF deposits over SIC, plus CHF and EUR/CHF pairs that remove the dollar conversion.

- Kraken Pro pricing, staking, and an OTC desk for larger orders.

Cons

- A cautious listing approach means fewer altcoins than the global venues here.

- Instant buys outside Kraken Pro carry a spread that punishes casual orders.

- CHF transfers settle in real time only during Swiss banking hours, not overnight.

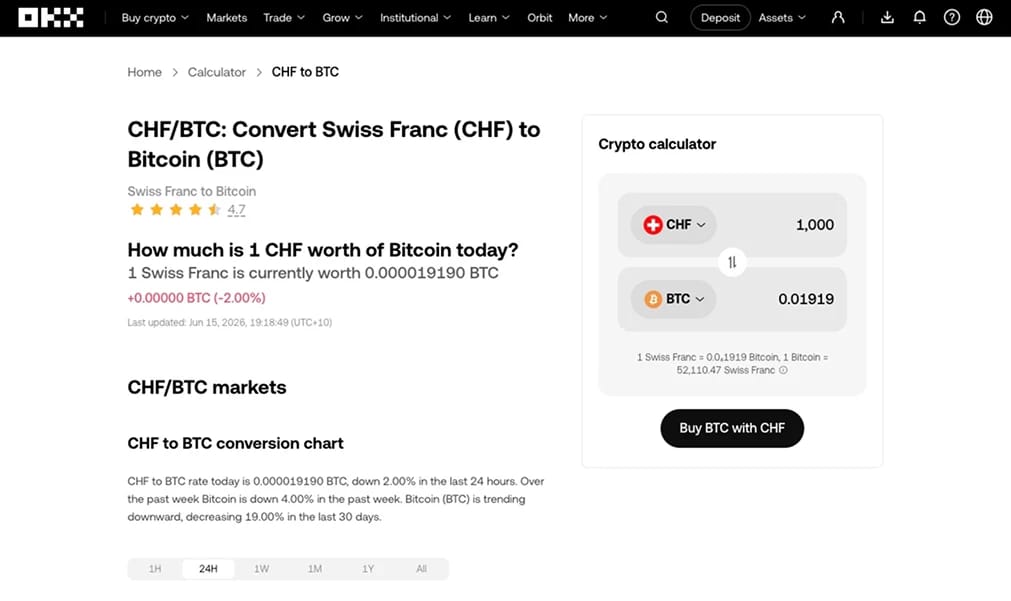

3. OKX

OKX is the cost leader and the pick for anyone looking to move beyond simple holding. Spot fees of 0.08% maker and 0.10% taker are the lowest among the major platforms serving Switzerland, and the app includes a Web3 wallet that opens access to DeFi, DEX trading, and on-chain tokens without a separate install. For Switzerland's large population of engineers and on-chain users, that single-app setup removes real friction.

The franc is available via cards or the P2P marketplace, since OKX has no direct CHF bank channel. Our P2P test, settled by bank transfer, was released from escrow in roughly ten minutes at a spread within 2% of the mid-market USDT price. The exchange publishes monthly Proof-of-Reserves attestations and lists over 350 spot assets, along with a full derivatives suite.

The drawback for Switzerland mirrors Bybit: bank-transfer funding is weaker than Kraken's, so cards or a USDT transfer remain the practical entries. OKX also settled with US authorities in early 2025 over anti-money-laundering failures, a compliance mark the cleaner records here do not carry, and the Web3 layer adds surface area a first-time buyer never needs. The platform is covered end-to-end in our OKX review.

Pros

- 0.08% maker and 0.10% taker fees, the cheapest order-book pricing on this list.

- Integrated Web3 wallet for DeFi and DEX access from one app.

- Monthly Proof-of-Reserves with a consistent publication history.

Cons

- No direct CHF channel, so cards and P2P are the only franc entries.

- The 2025 US settlement weighs on an otherwise solid record.

- Web3 depth adds complexity that a simple spot buyer can skip.

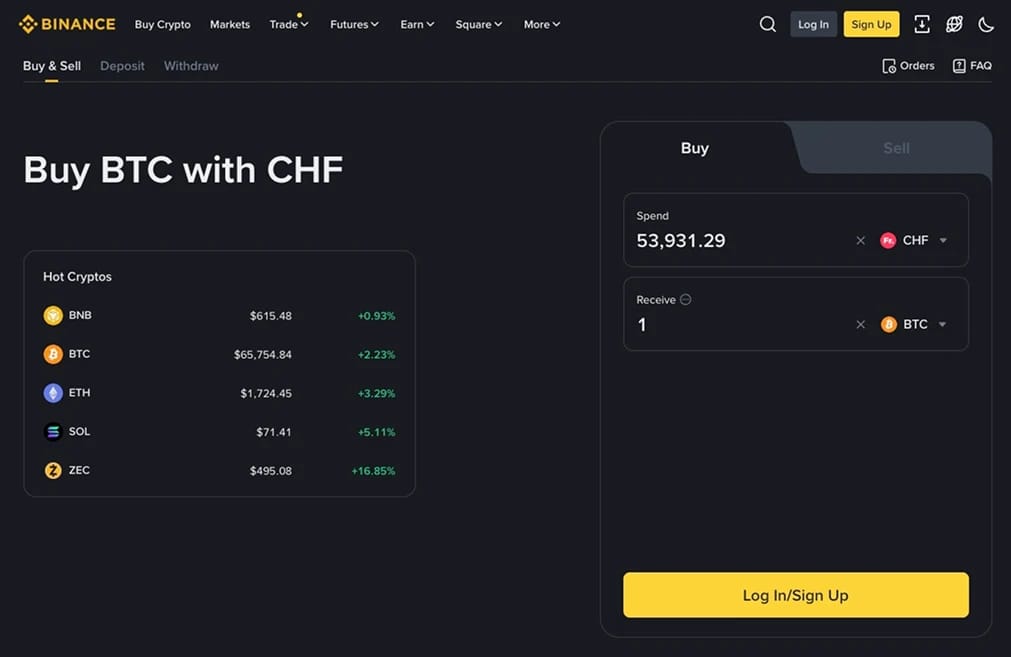

4. Binance

Binance brings the deepest order books in the industry, and on majors, that depth matters. Fills on BTC and ETH barely move the price at sizes that would visibly shift thinner books, 500+ assets trade at 0.1% before BNB discounts, and Earn, Launchpool, and Auto-Invest round out the passive side. For pure liquidity, nothing else here competes. It’s the world’s largest exchange, with over 320 million users.

The honest framing for Switzerland is funding. Binance does not support direct CHF or EUR bank deposits for Swiss residents, so francs reach the platform through a card or a P2P order. Many local users fund a euro balance through a service like Revolut and bridge from there, which works but adds a conversion step and an extra account to the chain.

History adds the other caveat. The 2023 US settlement remains the heaviest compliance mark in the industry, and the weak fiat path means Binance suits a trader who already holds stablecoins more than a saver funding from a Swiss bank for the first time. Fee tiers and products are unpacked in our Binance review.

Pros

- The deepest spot liquidity of any platform that a Swiss user can reach.

- 500+ assets at 0.1% spot fees with Earn, Launchpool, and a long-running SAFU fund.

- Card and P2P funding work once an account is verified.

Cons

- No direct CHF or EUR bank deposits for Swiss residents.

- The 2023 US settlement remains the industry’s heaviest compliance mark.

- Feature sprawl makes the app slow to learn for a first purchase.

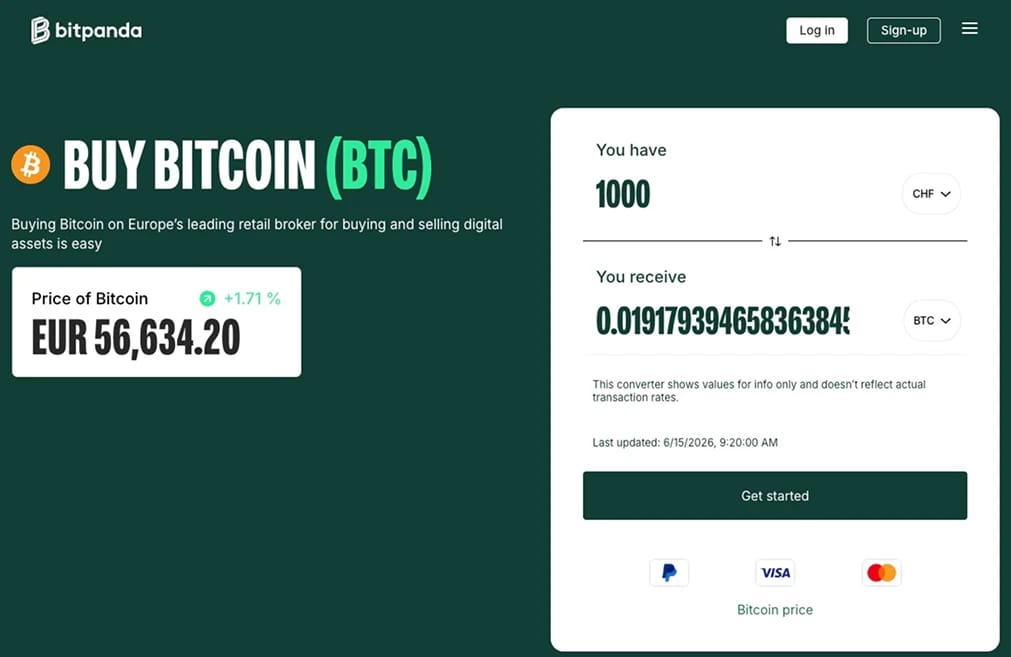

5. Bitpanda

Bitpanda is the broker for people who want crypto alongside other asset classes in a single account. The Vienna-based platform has held a MiCA license since early 2025 and ships a clean, beginner-friendly app. Alongside 600+ cryptocurrencies, it offers fractional contracts for stocks and ETFs, precious metals, and a Bitpanda Card for spending balances, all managed together.

Both CHF and EUR bank transfers settle with ease, and cards, Apple Pay, and Google Pay cover faster top-ups. We verified a Swiss ID without issue and had a SEPA deposit tradable the next business day. Per-product availability is listed on our Bitpanda countries page.

Cost is the catch. Standard buys and sells carry a premium of around 1.49% built into the price, more than ten times the 0.1% order-book fee on Bybit or Binance. That gap barely registers on a CHF 50 monthly savings plan and bites hard on a CHF 5,000 position, so size your usage to match.

Pros

- MiCA-licensed, with crypto, stocks, ETFs, and metals in one regulated account.

- Polished app with SEPA, card, Apple Pay, and Google Pay funding.

- Swiss identity documents were accepted smoothly for verification.

Cons

- The 1.49% buy/sell premium is the most expensive pricing on this list.

- The interface can still feel dense for a beginner.

- Spread-based pricing is less transparent than an open order book.

6. SwissBorg

SwissBorg is the home option, built in Lausanne and aimed at Swiss residents who want a simple way to hold crypto without juggling a full exchange. The app accepts direct CHF bank transfers, routes orders across multiple venues to improve the quote, and adds yield, auto-invest, and portfolio tools in a mobile-first layout that suits occasional rebalancing rather than active day trading.

The franc support is the local draw. A CHF transfer lands without the euro or dollar detour that most global platforms impose, and verification with Swiss documents is straightforward. SwissBorg operates under Swiss anti-money-laundering supervision and lists 100+ assets, fewer than the global venues but enough for a mainstream portfolio.

Pricing is where it loses ground. The all-in spread runs roughly 0.5% to 1.5% depending on membership tier, well above a Kraken Pro limit order, and the curated asset list rules it out for anyone chasing long-tail tokens. As a clean, Swiss-franc-native on-ramp for holders, though, it fills a gap the offshore platforms leave open.

Pros

- Direct CHF bank transfers with no forced conversion to euros or dollars.

- A Swiss-built, mobile-first app with smart order routing and yield products.

- Swiss AML supervision and easy verification with local documents.

Cons

- Tiered spreads of 0.5% to 1.5% sit above order-book pricing.

- 100+ assets trail every global platform here.

- Yield products advertise variable rates that deserve a close read before committing.

How to Choose a Crypto Exchange in Switzerland

For Swiss investors, the main question is not which exchange lists the most coins. It is how cheaply and reliably you can move francs in and out, and then whether the platform matches how you actually plan to use crypto.

- Decide whether you need direct CHF or can accept a conversion. Kraken, Bybit, Bitpanda and SwissBorg take francs straight from a Swiss account; OKX and Binance accept cards, euros, or a stablecoin transfer, each adding a markup or an FX step. Send a small amount first, since acceptance varies between banks.

- Test your own bank before scaling up. Swiss banks differ in how they treat transfers to crypto venues, and a small credit card purchase confirms whether yours clears before you commit size. If your bank already offers in-app trading, such as PostFinance or Swissquote, compare its spread against an exchange limit order before defaulting to convenience.

- Keep acquisition records from the first buy. Private capital gains are tax-free, but you still declare every holding for wealth tax at its 31 December value, and staking or mining income is taxed when received. Save exchange statements and transfer confirmations so the cantonal declaration is a copy job, not a reconstruction.

- Match the platform to what you do. Long-term holders fit Kraken plus a hardware wallet, active traders fit Bybit or OKX, multi-asset investors fit Bitpanda, and franc-first beginners fit SwissBorg. Anyone buying stablecoins specifically should read our guide to buying USDT in Switzerland.

Crypto and Bitcoin Regulation in Switzerland

Switzerland regulates crypto through existing financial law adapted for digital assets, supervised by FINMA. The framework is among the clearest in the world:

- The DLT Act: In force from 1 August 2021, with the ledger-based securities provisions live since February 2021, the Distributed Ledger Technology Act amended several federal laws to give tokenized assets legal certainty.

- Token classification: FINMA sorts every token into one of three categories: payment, utility, or asset, plus a hybrid residual. Bitcoin and Ether are payment tokens and are not treated as securities, whereas asset tokens that behave like equity or debt are subject to securities law. The classification follows the token's economic function, not its label.

- AML obligations: Service providers dealing with Swiss clients are financial intermediaries under the Anti-Money Laundering Act and must verify identity and monitor transactions. Customer identification thresholds for crypto transactions sit low, which is why even modest offshore deposits trigger KYC.

- Banks are in, not out: Unlike most jurisdictions, Swiss banks may offer crypto directly. PostFinance and Zürcher Kantonalbank launched trading and custody in 2024, UBS opened Bitcoin and Ethereum trading to select private clients in January 2026, and roughly 20 banks now provide some form of crypto service.

- CARF reporting from 2026: From 1 January 2026, Swiss crypto service providers began collecting transaction data under the OECD's Crypto-Asset Reporting Framework, with automatic exchange of that information starting to phase in. Federal draft amendments proposing dedicated stablecoin-issuer and crypto-institution licenses were also under consultation into early 2026.

Individuals face no restriction on using offshore platforms, but those platforms owe nothing under Swiss law. A FINMA-supervised bank or a licensed Swiss provider is the only channel backed by a domestic regulator.

How is Crypto Taxed in Switzerland?

Switzerland's tax treatment is the headline reason it earns the "crypto nation" label. The Federal Tax Administration applies the following to private individuals:

- No capital gains tax: Crypto counts as a private wealth asset, the same category as stocks and bonds, so a private investor pays nothing on the gain when selling. Buy Bitcoin at CHF 10,000 and sell at CHF 50,000, and the CHF 40,000 profit is tax-free.

- The professional-trader line: The exemption only holds if you stay on the private side of FTA practice. The safe-haven tests include holding assets for at least six months, an annual turnover below five times your portfolio value at the start of the year, gains under half your total income, no debt financing, and derivatives used only for hedging.

- Wealth tax applies regardless: Cantons and municipalities levy an annual wealth tax on total assets, including crypto, valued at market price on 31 December. The FTA publishes year-end rates for major coins. The rate is modest and cantonal allowances apply, but every holding must be declared.

- Income tax on rewards: Staking, mining, lending, and airdrop rewards are taxed as income at their franc value when received, across federal, cantonal, and municipal layers. Salary paid in crypto is treated the same way.

Set against the regimes in our best low-tax crypto countries guide, Switzerland sits near the top for private holders, though the professional-trader boundary is where people get caught.

This is general information rather than tax advice, so confirm your status with a Swiss tax adviser, since the private-versus-professional call is made canton by canton.

Cryptocurrency Adoption in Switzerland

Few countries have woven crypto into mainstream finance as deeply as Switzerland. The numbers and the institutions both reflect it:

- A large user base: Statista Market Insights projects user penetration near 45% for 2026, equivalent to more than 4 million people holding or using digital assets, well above the global average.

- Crypto Valley: The canton of Zug anchors a blockchain cluster that has spread to Zurich, Geneva, and Ticino, producing around 17 unicorns from a population a fraction of larger rivals. Zug itself accepts crypto for certain tax and administrative payments, settling through regulated intermediaries.

- Lugano's Plan B: Built with Tether, the Ticino city's initiative has onboarded hundreds of merchants to accept Bitcoin and USDT and lets residents pay for some municipal services in crypto, the most concrete everyday-payment experiment in the country.

- Banking depth: Roughly 20 banks offering crypto, more than any other nation, gives Switzerland a regulated retail layer most markets lack. PostFinance alone opened 36,000 crypto custody accounts and processed over 565,000 trades in its first year, and Swissquote now draws around a tenth of its revenue from digital assets.

The fuller global picture sits on our crypto adoption statistics page. What sets Switzerland apart is less the headline rate than the institutional plumbing behind it.

How to Buy Bitcoin in Switzerland

The clean path pairs direct franc funding with records the cantonal tax office will accept. The sequence we use:

- Open an account: Franc-first buyers should start with Kraken or SwissBorg for direct CHF, euro savers can use SEPA into Kraken or Bitpanda; and traders already holding stablecoins can fund Bybit, OKX, or Binance by transfer.

- Clear KYC: A passport or ID card plus a selfie verified within hours on every platform we tested. Enter your name exactly as printed, diacritics included where the form accepts them.

- Deposit funds: Send a direct CHF transfer over SIC where supported, a EUR SEPA payment, or a card purchase for speed. Start small to confirm your bank passes the payment, then scale, and keep the confirmation as your acquisition record.

- Buy BTC: Use the order-book screen and place a limit order on BTC/CHF, BTC/EUR, or BTC/USDT. Instant-buy screens price through spreads of 1% or more that a limit order sidesteps.

- Secure assets: Anything you are not actively trading belongs in your own wallet. Our best crypto wallets guide covers hardware and software options.

Exiting reverses the path: sell into CHF, withdraw to your Swiss account, and declare the year-end holding and any income rewards on your cantonal return.

Final Thoughts

Switzerland offers a rare mix: a clear law, a tax regime that exempts private capital gains, and a banking system that has chosen to participate rather than block access. The constraint is mechanical, since only some platforms move francs cleanly, and that is what shapes the trade-offs below.

Bybit leads for all-round capability, with the widest product range and the lowest flat fees a Swiss user can reach. Kraken is the security and direct-CHF pick, OKX wins on cost, Binance on liquidity, Bitpanda covers investors who want crypto alongside stocks and metals, and SwissBorg is the homegrown option.

For a broader regional view, our guide to the best crypto exchanges in Europe covers the MiCA-regulated market across Europe.

Our Methodology

We assessed each platform by repeating the steps a Swiss resident takes in practice: registering with a passport or ID card, funding through direct CHF, EUR SEPA, cards, and stablecoin transfers, executing spot trades, and withdrawing francs to a local account. Six criteria set the rankings:

- Trust Score: A 5-point rating weighing security history, reserve transparency, regulatory standing, and years of operation.

- CHF Funding Access: Whether the franc moves in directly or through a conversion, tested across SIC transfers, SEPA, Swiss-issued cards, and P2P settlement for speed and cost.

- Fees: Headline maker and taker rates plus the full round-trip cost, including spreads, card markups, and any FX leg the franc meets.

- Asset Range: Coverage from majors and stablecoins through long-tail tokens, derivatives, and adjacent asset classes.

- Tax Practicality: Whether statements hold up as acquisition and year-end valuation evidence under Swiss wealth and income tax rules.

- Local Usability: KYC friction with Swiss documents, app performance, and the quality of the CHF exit path.

We balanced funding access against product depth, security, and cost rather than letting any single axis decide, because no platform here tops every category. Testing ran from March to June 2026.

.webp)