Can I Buy USDT in India?

Yes. Buying, holding, and trading USDT is legal. Cryptocurrency is not recognised as legal tender, but it is classified as a Virtual Digital Asset (VDA) under Section 2(47A) of the Income Tax Act, with no restriction on individuals owning or trading it through registered platforms in India that comply with FIU-IND requirements.

India sits at the top of Chainalysis's 2025 Global Crypto Adoption Index for the second year running, ranking first across all four sub-indices. Total on-chain transaction volume reached roughly $338 billion in the 12 months to June 2025, with APAC growing 69% year over year.

The practical friction is not legality but the banking layer. Offshore exchanges cannot plug directly into Indian banking rails, so they settle INR deposits through licensed domestic payment aggregators (Bybit uses Onmeta), through P2P merchants, or through card gateways. This is why the user experience differs sharply between platforms even though they all ultimately sell the same USDT.

How to Buy Tether (USDT) in India

The cleanest way to buy USDT from India is through a FIU-registered exchange that handles INR deposits via UPI or IMPS rather than forcing every trade onto P2P. Bybit fits this well because it is registered as a VDASP with FIU-IND, settles UPI deposits through Onmeta in minutes, and deducts the 1% TDS automatically on sales.

I tend to use UPI for smaller top-ups because it clears instantly and skips the card surcharge, and IMPS bank transfer for larger amounts where I want a clean reference number sitting in my bank statement for later reconciliation.

Steps to buy Tether (USDT) on Bybit from India:

- Create an Account: Sign up on Bybit and complete Identity Verification Level 1 using your PAN card and Aadhaar. Most FIU-registered platforms also run a penny-drop bank verification to confirm your account name matches your PAN, so align the two before you start or you will hit rejection.

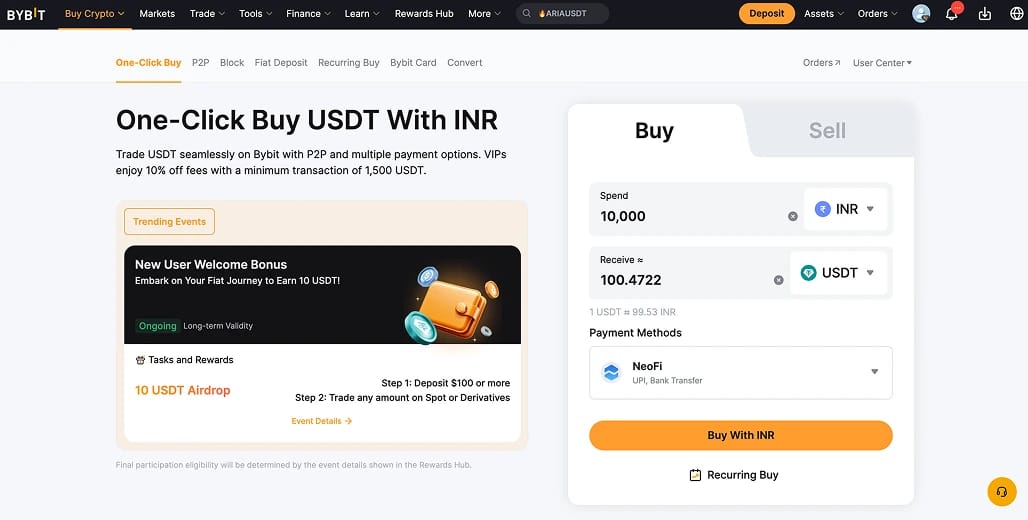

- Deposit INR: Go to Buy Crypto and select One-Click Buy with UPI, IMPS, or bank transfer. Deposits settle through Onmeta and typically credit your Funding wallet within a few minutes during banking hours.

- Pick Your Pair: Once INR reflects, use One-Click Buy for an instant USDT conversion, or open the USDT/INR spot order book if you want a tighter price on larger amounts.

- Receive USDT: USDT lands in your Funding wallet. From there you can trade it, hold it, or withdraw to a personal wallet on TRC-20 (cheapest) or ERC-20.

INR to USDT Fees

The headline 0.1% spot fee is only part of what you pay. Deposit method, spread on the instant-buy quote, the 1% TDS on the sell side, and the 30% VDA tax at year-end all compound into the real cost.

Deposits

- UPI: 0% Bybit fee. Onmeta applies a small processing spread baked into the quoted rate, typically under 1%. Instant settlement.

- IMPS / Bank Transfer: Same Onmeta rails, comparable effective cost to UPI. I prefer this for larger tickets because the IMPS reference number on your statement is cleaner documentation if anyone asks later.

- P2P Trading: No platform fee. Merchants typically include a 0.5% to 2% markup over spot depending on liquidity conditions. Bybit's verified merchant filter and completion rate are the numbers that matter here. I never trade with anyone below a 95% rate or under a few hundred completed orders.

- Credit / Debit Card: 2% to 3.5% surcharge through third-party gateways. Useful when UPI is down at odd hours, rarely worth the markup otherwise.

Withdrawals

- Crypto: Blockchain network fee applies. TRC-20 USDT is usually under $2. ERC-20 costs significantly more depending on Ethereum gas.

- INR off-ramp: Sell USDT to INR on the spot book, then withdraw through UPI or IMPS. The 1% TDS is deducted automatically by Bybit as your registered VDASP.

Trading

- Spot maker / taker: 0.10% at the standard tier. VIP volume discounts apply above $100k 30-day volume.

- 18% GST on fees: Since July 7, 2025, Bybit applies an 18% Goods and Services Tax on top of trading and service fees for Indian residents, in line with the CGST Act. This bumps the effective spot fee to roughly 0.118% rather than 0.10%. CoinDCX, Binance, and KuCoin apply equivalent GST when serving Indian users.

All-in cost for a UPI deposit plus a spot buy typically lands under 1.7%, before you factor the 1% TDS that lands on the eventual sell.

Best USDT Exchanges in India

Indian users have three other FIU-registered USDT exchanges worth considering, depending on whether you want deeper P2P liquidity, a fully domestic setup, or a different fee structure.

Regulatory Status of USDT in India

Crypto operates under a compliance framework in India rather than a dedicated licensing regime. The foundation is the March 2023 PMLA notification from the Ministry of Finance, which brought Virtual Digital Asset Service Providers (VDASPs) into the scope of the Prevention of Money Laundering Act, 2002. Any exchange serving Indian customers, including offshore platforms, must register with FIU-IND as a reporting entity.

Three authorities share oversight:

In December 2023, FIU-IND issued show-cause notices to nine offshore exchanges including Binance, KuCoin, Huobi, Kraken, Gate.io, and Bitstamp, and ordered the Ministry of Electronics and IT (MeitY) to block their URLs. The registration path that followed was effectively pay-a-penalty-and-register:

- Binance registered in August 2024 after a fine of around ₹18.82 crore (approximately $2.25 million)

- KuCoin registered after a smaller fine of about $41,000

- Bybit registered in February 2025 after settling a ₹92.7 crore fine (roughly $1 million) and resumed Indian operations on February 25, 2025

- OKX and Bitstamp closed their Indian services rather than register

As of FY 2024-25, 49 exchanges are FIU-IND registered, comprising 45 domestic and 4 offshore platforms. This is the register to check before depositing any funds.

Crypto is not recognised as legal tender. Using USDT to pay for goods and services domestically is not permitted, but holding and trading it is unrestricted.

Tax Implications of USDT in India

India has one of the harshest crypto tax regimes globally, and it catches stablecoin users particularly hard because crypto-to-crypto trades are taxable events even when no INR is realised.

The core provisions, introduced in Union Budget 2022 and carried through Budget 2026 unchanged:

- 30% flat tax + 4% cess on all VDA gains under Section 115BBH. Effective rate of 31.2%, regardless of holding period.

- No deductions apart from cost of acquisition. You cannot deduct gas fees, trading fees, or any other expense.

- No loss offsetting. Losses from VDAs cannot offset gains from other VDAs or any other income, and cannot be carried forward. Each transaction is taxed independently.

- 1% TDS (Section 194S) on the transfer of any VDA, applied once aggregate transactions exceed ₹50,000 per financial year for "specified persons" (individuals and HUFs without business income, or with business turnover up to ₹1 crore / professional receipts up to ₹50 lakh) or ₹10,000 per financial year for everyone else. FIU-registered exchanges deduct this at source automatically.

- Schedule VDA reporting in your ITR-2 or ITR-3. Gains are declared separately from other capital gains and must be reconciled against the TDS statements issued by your exchange.

- 18% GST on exchange fees, applied by both domestic and offshore VDA Service Providers serving Indian residents under the CGST Act. This is a separate consumption tax levied on trading fees, withdrawal fees, and spreads, not on the asset value itself.

Reporting is tightening on both sides. Exchanges face new penalties from April 1, 2026 for late or inaccurate crypto-asset filings under Section 509, and FIU-IND is building tools to detect unregistered offshore providers. Practically, this means more of your trade data flows to the tax authority by default.

💡For active users: log every transaction in INR terms (buy date, sell date, INR value on each side), reconcile against exchange TDS statements quarterly, and consult a CA familiar with VDA rules if your annual volume exceeds ₹50 lakh.

Why Indians Use USDT

In most countries, USDT is a trading instrument. In India, it does several jobs at once:

- Dollar access without LRS friction: The Liberalised Remittance Scheme caps outward remittances from resident individuals at $250,000 per financial year, with TCS (Tax Collected at Source) kicking in above a threshold. USDT bypasses LRS entirely because blockchain transfers are not currently classified as foreign remittance under FEMA, though this remains a grey area worth watching as the CBDT tightens VDA reporting.

- Freelancer and IT services payments: India received $129 billion in remittance inflows in 2024, the largest in the world for the year, and runs a $224 billion IT services export economy per NASSCOM's FY25 estimates. A meaningful slice of that flow is developers, consultants, and agencies billing international clients. Receiving USDT and selling on a compliant exchange often clears faster and cheaper than SWIFT, which can take 2 to 5 days and cost ₹500 to ₹2,000 per transfer.

- Trading base currency: Almost every crypto pair on global exchanges is quoted in USDT. If you want to trade anything beyond BTC, ETH, and a handful of INR pairs on domestic exchanges, USDT is the base you need.

- Rupee weakness hedge: The INR has depreciated from around 75 to over 93 against the USD since early 2020, hitting fresh record lows in March 2026. Holding a portion of savings in dollar-denominated value has become a practical hedge for professional-class Indians, and USDT is the easiest way to do it without a brokerage account. Many users I speak to treat their USDT balance less like a trading position and more like a dollar savings account.

One Risk Worth Calling Out: Bank Account Freezes

The single biggest operational risk for Indian crypto users is not legality or tax. It is the bank account freeze.

When you sell USDT on P2P, the INR you receive comes from another user's bank account. If that user was a scam victim and they later file a cybercrime complaint at 1930 or cybercrime.gov.in, the cyber cell can trace funds forward and freeze every account that touched them, including yours. The freeze happens under Section 102 of the CrPC on suspicion alone, without prior notice.

I know multiple people this has happened to. Getting the account unfrozen involves bank statements, exchange trade confirmations, a visit to the cyber cell with documentation, and sometimes a Magistrate Court petition. The process takes weeks.

Mitigation:

- Buy through a registered exchange with direct UPI/IMPS rails (Bybit via Onmeta, CoinDCX via UPI) rather than P2P wherever possible. Receiving funds from a licensed aggregator carries near-zero freeze risk compared with receiving from an unknown counterparty.

- If you must use P2P, stick to verified merchants with long histories, high completion rates (95%+), and large completed order counts.

- Screenshot every trade (order ID, counterparty ID, exchange confirmation) and keep them for at least 6 months.

- Avoid single large P2P sells. Split into multiple tranches across sessions and counterparties.

Buying USDT is almost always safe. Selling is where the exposure concentrates, so plan the exit before you enter the position.

Final Thoughts

Buying USDT in India is legal, regulated, and operationally simple through FIU-registered platforms. The hard parts sit on either side of the trade: choosing a deposit path that does not touch risky P2P counterparties, tracking every conversion in INR for Schedule VDA, and planning the off-ramp carefully to avoid bank freeze exposure.

Bybit works well as a default for most Indian users because it is FIU-registered, supports direct UPI and IMPS deposits through Onmeta, deducts the 1% TDS automatically, and carries the deepest USDT liquidity in this market. Binance, KuCoin, and CoinDCX each cover alternative profiles if you want deeper P2P markets, different derivatives, or a fully domestic setup.

Whatever you pick, treat crypto in India like the compliance-heavy asset class it has become. Keep clean records, reconcile TDS statements every quarter, budget for the 30% tax at year-end, and never mistake an exchange's dashboard for a substitute for your own transaction ledger.