Compare Top Crypto Exchanges in Bangladesh

1. Bybit

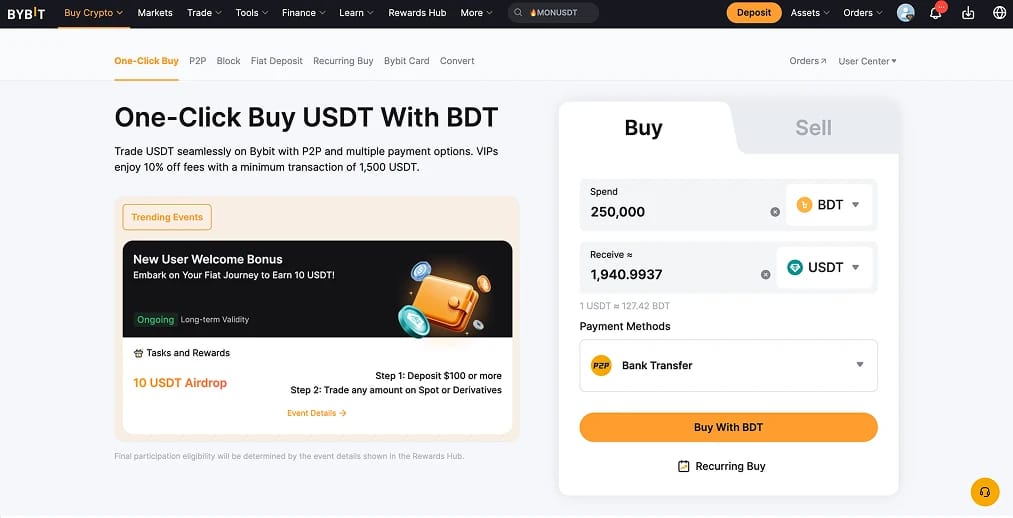

Bybit handles the full journey from BDT to crypto better than any rival we tested. The P2P marketplace supports bKash, Nagad, Rocket, and direct bank transfers, so the path from taka into USDT is about as clean as it gets in Bangladesh right now.

From there, you get 2,500+ cryptocurrencies across spot, perpetual futures (up to 200x leverage), options, copy trading, and much more. The mobile app also has a Lite mode that strips out the complexity, which matters here. Many first-time users in Bangladesh are onboarding on their phones, and the full Pro interface can be overwhelming if you have never traded before.

I spent time testing Bybit Earn and the USDT flexible savings rates were competitive. If your plan is to hold stablecoins and earn a modest return rather than actively trade, it does the job. The Web3 wallet also opens up DeFi access without needing MetaMask or any third-party tool.

Pros

- P2P desk covers bKash, Nagad, Rocket, and bank transfer. These are the mobile financial services Bangladeshi users actually rely on day to day.

- Spot fees from 0.1% and futures maker fees among the lowest globally.

- Proof-of-reserves reporting adds a layer of transparency that matters when you are trusting an offshore platform.

Cons

- No direct bank wire or card path in taka. BDT deposits only work through the P2P marketplace.

- Product menu is dense enough to confuse newer users unless they switch to Lite mode immediately.

- Not a long-term custody solution. Move large holdings to a hardware wallet.

2. Binance

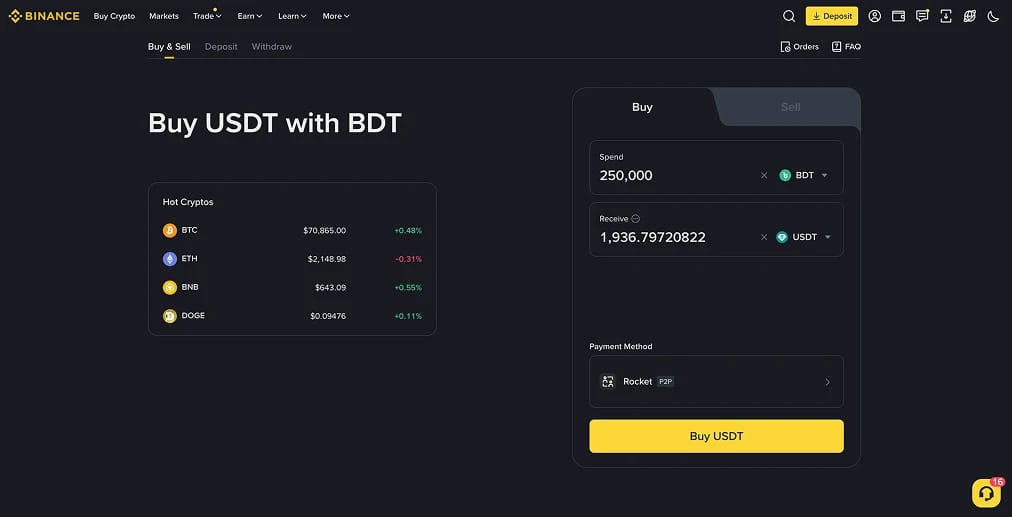

If you have used Binance P2P in Bangladesh, you already know why it belongs near the top of this list. The BDT merchant count and order volume are significantly higher than any other platform, which means tighter USDT pricing and faster trade completion. That liquidity is the whole reason Binance became the default exchange for so many Bangladeshi users over the years.

When we ran comparisons, Binance P2P had more active BDT merchants, more payment options (bKash, Nagad, bank transfer, and sometimes cards), and more completed orders than Bybit, OKX, or Bitget. It is not close. Where Bybit wins on overall product quality, Binance wins on the single thing that matters most in Bangladesh: getting taka in.

Once funded, you get 500+ assets, spot, margin, and futures with 125x leverage, plus Launchpool, Binance Earn, Copy Trading, and Auto-Invest for cost-averaging. Order book depth is the best in the industry, so execution on BTC/USDT and ETH/USDT pairs is clean even in volatile sessions.

Pros

- Deepest P2P desk for BDT available anywhere. More merchants, more payment methods, faster fills.

- bKash, Nagad, bank transfers, and card payments all supported through P2P and third-party routes.

- Order book liquidity keeps spreads tight on major pairs.

Cons

- Ongoing regulatory scrutiny across multiple jurisdictions creates platform risk worth watching.

- Feature overload can bury beginners who just want to convert BDT to Bitcoin.

- P2P dispute resolution during busy periods has room to improve.

3. KuCoin

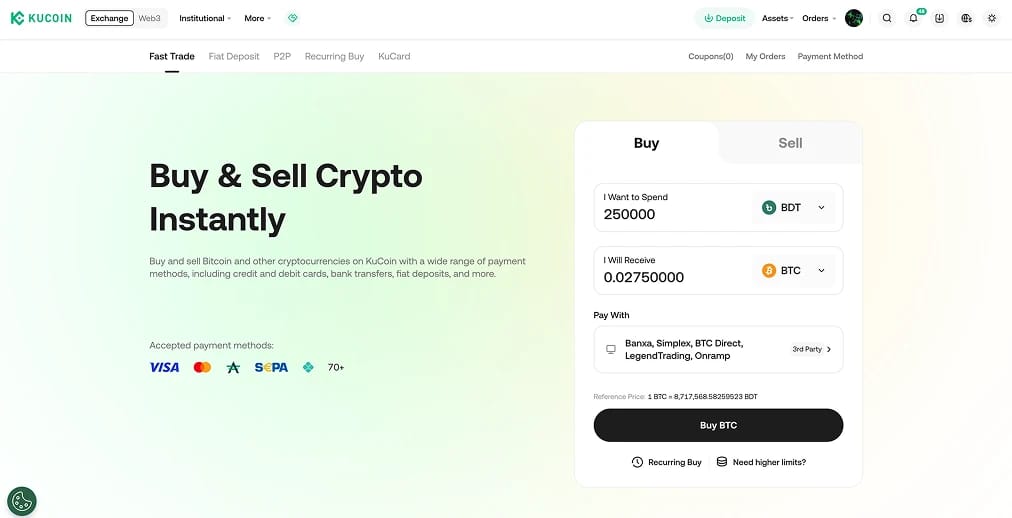

KuCoin fills a different gap. If you want broader altcoin access without wading through Gate's 4,400+ listings, this is the middle ground. Over 1,000 cryptocurrencies are listed, and KuCoin has a track record for getting smaller-cap projects on the platform early through its GemSPACE hub.

You can start with as little as $1, which is meaningful in a market where many newer traders want to test the waters before committing real money. Card purchases and P2P services are both available, though the BDT P2P depth is noticeably thinner than what you will find on Bybit or Binance. If your Visa or Mastercard works for international transactions, the direct card buy path is there.

Beyond spot trading, KuCoin covers margin, futures (up to 100x), and a decent trading bot suite. KuCoin Earn has flexible and fixed savings, crypto lending, and some promotional staking rewards with high APYs. The interface is less cluttered than Binance, making it easier for anyone, from beginners to advanced users.

Pros

- 1,000+ cryptocurrencies with early access to emerging altcoins through GemSPACE.

- $1 minimum means you can test the platform without meaningful risk.

- Card deposits offer an alternative when P2P is inconvenient.

Cons

- BDT P2P liquidity is thin compared to Bybit and Binance. Expect fewer merchants and slower fills.

- No major regulatory licenses. You are relying on the platform's track record, not an external regulator.

- Bangladeshi bank cards get declined on international crypto purchases often enough that you should test small first.

4. OKX

OKX is the one to look at if you have outgrown basic spot buying and want a single platform that bridges CEX trading with on-chain DeFi. The built-in OKX Wallet is non-custodial and connects to protocols, NFT marketplaces, and dApps across 130+ chains without leaving the app.

On the centralized side, you get spot, margin, perpetual and expiry futures, and options. The TradingView integration is genuinely one of the best out there, and it makes a difference if charting is part of your workflow. OKX P2P supports bank transfer and card payments in BDT, but the merchant count is smaller. Expect fewer options and slower trade times compared to Bybit or Binance.

Where OKX clicks is for someone who wants to trade on a CEX, then self-custody their assets, stake on-chain, explore yield farming, and interact with DeFi protocols, all from one interface. The base spot fee of 0.08% is also the lowest in this comparison.

Pros

- Web3 wallet built into the platform for direct DeFi, NFT, and dApp access.

- 0.08% spot fees, the lowest base rate on this list.

- TradingView integration is a real advantage for technical traders.

Cons

- BDT P2P merchant volume lags Bybit and Binance. Fills take longer and pricing can be wider.

- The Web3 layer adds complexity that most casual buyers will never touch.

- If all you need is a quick BTC purchase through bKash, this is more platform than the job requires.

5. Bitget

Bitget is where copy trading is the actual product, not a secondary feature tacked onto a spot exchange. The platform has leaned into social and systematic trading harder than anyone else on this list, and the infrastructure around it (strategy selection, performance transparency, risk controls) reflects that.

The BDT P2P desk supports bKash, Rocket, Perfect Money, and AirTM. Merchant count is decent and the flow works. Once you are funded, you get spot and futures across 800+ cryptocurrencies, bot trading, and launchpool access. Nothing unusual there.

What caught my attention on the trust side: Bitget published a February 2026 proof-of-reserves report showing a 169% total reserve ratio and disclosed a protection fund averaging roughly $447 million. For an exchange operating without local regulatory cover in Bangladesh, those signals carry weight.

Pros

- Copy trading built as a first-class product. Strategy selection, performance history, and risk management tools are well above average.

- P2P supports bKash, Rocket, Perfect Money, and AirTM for workable BDT on-ramping.

- Proof-of-reserves and a large protection fund provide better trust signals than most offshore competitors.

Cons

- Copy trading can lead users into leverage exposure they have not properly sized. The ease of it is the risk.

- Product suite skews toward active trading. Not the right fit if you just want to buy and sit.

- BDT P2P liquidity does not match Bybit or Binance.

6. Gate

Gate is on this list for one reason: it lists more than 4,400 cryptocurrencies, which is roughly double what you will find on Binance and nearly five times OKX. If you are chasing smaller altcoins or newly listed tokens that never make it to mainstream exchanges, Gate almost always has them.

The catch in Bangladesh is funding. Gate does not offer BDT P2P. Your path in is through credit/debit cards or Google Pay, and those transactions process in USD. That means your bank card needs to work for international payments. Several major Bangladeshi banks, including Dutch-Bangla Bank and Islami Bank, have been known to block transactions to crypto platforms entirely.

If you can get past the funding hurdle, Gate is solid. Spot, futures (100x), margin, copy trading, and Simple Earn products are all available. Proof-of-reserves reports have consistently shown a reserve ratio above 125%, and the platform has been running since 2013 without a major breach.

Pros

- Largest token selection of any exchange on this list. Over 4,400 cryptocurrencies.

- Consistent proof-of-reserves transparency since the feature became an industry norm.

- Long operating history with no major security incidents.

Cons

- No BDT P2P marketplace. You are entirely dependent on card payments working.

- Bangladeshi bank cards frequently get blocked for crypto purchases. Funding is unreliable.

- The interface feels busy and the sheer listing volume can overwhelm newer users.

How to Choose a Crypto Exchange in Bangladesh

Picking an exchange here is not the same as picking one in Singapore or the UK. No local licensing exists, there is no regulated on-ramp, and no consumer protection framework covers you if something goes wrong. The standard "choose a regulated platform" advice barely applies, because none of these platforms are regulated by Bangladesh Bank.

So the decision comes down to practical questions. Can you actually get taka onto the platform? How deep is the P2P book? What happens if KYC gets flagged? And can you pull your money out cleanly when you want to exit?

Step 1: Check BDT P2P liquidity before anything else

Most guides skip this. In Bangladesh, direct BDT bank wires to crypto exchanges are effectively impossible. Most major banks block the transaction or flag your account. P2P is the primary funding method.

Open the P2P section before committing. Check whether BDT is listed, how many active merchants exist, and whether they accept the payment methods you actually use. If bKash or Nagad is how you move money, you need real order volume behind those options, not a few listings with wide spreads.

Bybit and Binance had the strongest BDT P2P markets when we tested. Bitget and OKX were usable but thinner. Gate and KuCoin lean on card payments, which introduces different friction.

Step 2: Check if your Bangladeshi bank blocks crypto purchases

Planning to use Visa or Mastercard? Test with a small amount first. These banks have been reported to block crypto exchange transactions:

Smaller banks tend to be less restrictive, but nothing is guaranteed. Sometimes the transaction fails silently. Other times your bank calls you. Either way, you do not want to find out when it matters.

Step 3: Complete KYC with your NID or passport early

Finish identity verification before sending money to the platform. Most exchanges require it before P2P, withdrawals, or higher limits unlock. In Bangladesh, that means an NID, passport, or driver's license, plus a selfie.

Common rejection reasons: Name mismatches between your NID and exchange profile. Blurry document photos. Manual review queues that drag for days. Getting stuck mid-verification with funds already deposited is the scenario to avoid.

Step 4: Calculate the real cost of converting BDT to crypto

P2P merchants set their own rates. USDT pricing is often 1% to 3% above global spot, and it shifts with time of day, merchant competition, and payment method.

But the P2P spread is only one layer:

- P2P markup (BDT to USDT): 1% to 3% above spot

- Exchange spot trading fee: 0.08% to 0.2%

- BTC network withdrawal fee: Varies by exchange

A platform advertising 0.1% spot fees can still cost more if its P2P merchants charge wider markups or withdrawals are expensive. Compare the full cycle, not the headline.

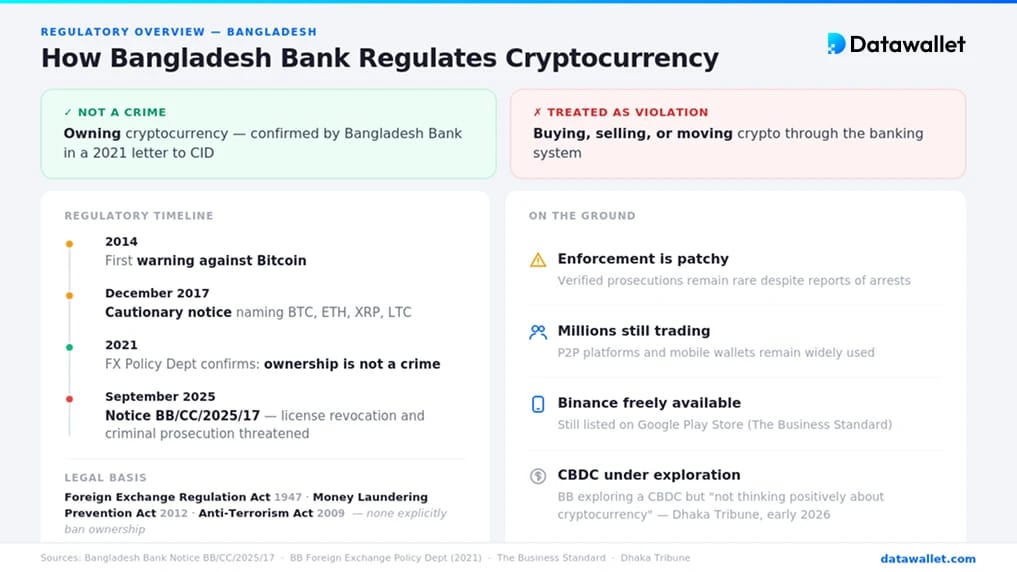

How Bangladesh Bank Regulates Cryptocurrency

Bangladesh is one of the most restrictive countries in the world for cryptocurrency. Bangladesh Bank first warned against Bitcoin in 2014, then issued a formal cautionary notice in December 2017 naming Bitcoin, Ethereum, Ripple, and Litecoin. By September 2025, Warning Notice No. BB/CC/2025/17 escalated the language to license revocation and criminal prosecution for any entity facilitating crypto transactions.

The legal basis sits across three laws: the Foreign Exchange Regulation Act, 1947, the Money Laundering Prevention Act, 2012, and the Anti-Terrorism Act, 2009. But none of them explicitly ban owning crypto. Bangladesh Bank's Foreign Exchange Policy Department confirmed this in a 2021 letter to the CID: ownership is not a crime. The transactions are the problem. Buying, selling, or moving crypto through the banking system can be treated as a violation.

In practice, enforcement is patchy. Verified prosecutions remain rare despite reports of arrests. Millions keep trading through P2P and mobile wallets. The Business Standard noted that Binance is still freely available on the Google Play Store. Bangladesh Bank is exploring a CBDC, but Dhaka Tribune reported in early 2026 that the regulator is "not thinking positively about cryptocurrency at this time."

How the NBR Taxes Cryptocurrency in Bangladesh

Bangladesh has no dedicated cryptocurrency tax law. The National Board of Revenue (NBR) has not issued specific guidance on crypto gains, and the tax status of digital assets remains formally unclear.

In practice, the NBR applies the Income Tax Ordinance of 1984 to all income, including asset disposals. This creates a legal contradiction: gains from selling crypto could be treated as taxable, but declaring them means disclosing activity the central bank considers unauthorized. That tension has not been resolved.

What we can piece together from existing law:

- Capital Gains: Profits from selling crypto may attract approximately 15% tax for individuals. The NBR has not confirmed this rate applies to digital assets specifically.

- Income Tax: Mining, staking, or running a crypto-related operation falls under standard slabs from 0% to 30%. The tax-free threshold for FY 2025-26 is 375,000 BDT.

- VAT: The standard 15% rate exists, but whether it applies to crypto transactions has not been defined.

- Record-Keeping: Worth doing regardless. If Bangladesh introduces a formal crypto framework later, clean records will matter.

Most Bangladeshi crypto users do not report gains, and tax enforcement has been minimal. But the government can technically penalize you for the unauthorized transaction and the unreported income simultaneously. If your holdings are significant, talk to a local tax professional.

Cryptocurrency Adoption Statistics in Bangladesh

Despite the ban, Bangladesh has quietly become one of the world's top crypto-adopting nations. The Chainalysis 2025 Global Crypto Adoption Index ranked the country 13th out of 151, up from 17th the year before. Only India ranked higher in South Asia. TRM Labs placed Bangladesh 14th, noting that adoption persists through underground channels despite capital controls and enforcement risk.

Roughly 3.1 million Bangladeshis now hold crypto wallets. The drivers are practical, not speculative:

- Freelancer payments: Bangladesh has one of the largest freelancing populations globally. Many receive international payments in USDT because it is faster and cheaper than bank wires or Payoneer.

- Remittance demand: The country received over $30 billion in remittances in FY2025. Traditional channels average 6.5% in fees. Crypto is cheaper even after P2P spreads.

- Inflation hedging: As foreign reserves dipped through 2024-2025, stablecoins became a way to park dollar-denominated value outside the banking system.

- Young, mobile-first population: Median age around 28, rapid smartphone growth, and normalized digital payments through bKash and Nagad. The step from mobile money to P2P crypto is short.

This is not a market built on speculation. It is built on people solving real problems with real constraints.

.webp)

How to Buy Bitcoin in Bangladesh

Buying Bitcoin here comes down to finding a P2P path that works with bKash, Nagad, or bank transfer, getting verified without issues, and converting BDT to BTC without giving up too much in the spread. Here is the process we follow:

- Pick a platform with strong BDT P2P liquidity: Open the P2P section first. Check BDT merchant count, payment methods, and recent completion rates. Bybit and Binance consistently perform best. If the desk looks thin, move on.

- Complete KYC before funding: Finish verification with your NID, passport, or driver's license before attempting any P2P trade. Some exchanges lock P2P behind KYC, and a stuck verification with money in limbo is the outcome you want to avoid.

- Buy USDT through P2P: The cleanest path is buying USDT first through P2P using bKash, Nagad, or bank transfer. Compare merchant pricing carefully. USDT rates can vary by 1-3% depending on the merchant and time of day. Always use escrow. Never trade outside the platform.

- Trade USDT for BTC on spot: Once USDT is in your wallet, place an order on the BTC/USDT pair. Limit order for price control, market order when speed matters. Skip the one-click "buy crypto" screen. The spread hidden inside it costs more than a spot trade.

- Withdraw to self-custody: Not actively trading? Move your BTC off-exchange to a personal wallet. Hardware wallets like Ledger or Trezor are the strongest option. Double-check the withdrawal fee and network selection before confirming.

This gives you the most reliable, cost-effective path into Bitcoin from Bangladesh. Avoid card routes that may get blocked and informal OTC agents who operate outside escrow.

Final Thoughts

Buying crypto in Bangladesh takes more planning than most countries. No regulatory safety net, no licensed local exchange, and no guarantee your bank will cooperate. But the platforms in this guide are practical choices if you approach it correctly.

Start with the P2P desk, not the marketing page. If the platform cannot reliably get BDT, nothing else about it matters. Bybit and Binance are strongest on that front. If your focus is on altcoins, KuCoin and Gate offer a broader selection. For Web3 or copy trading, OKX and Bitget are worth a look.

Before depositing anything, complete KYC, test your payment method with a small amount, and compare the full cost of converting BDT to crypto across a few platforms. That groundwork will save you more than any fee table comparison.

%2520(1).webp)