Compare Top Crypto Exchanges in Morocco

1. Bybit

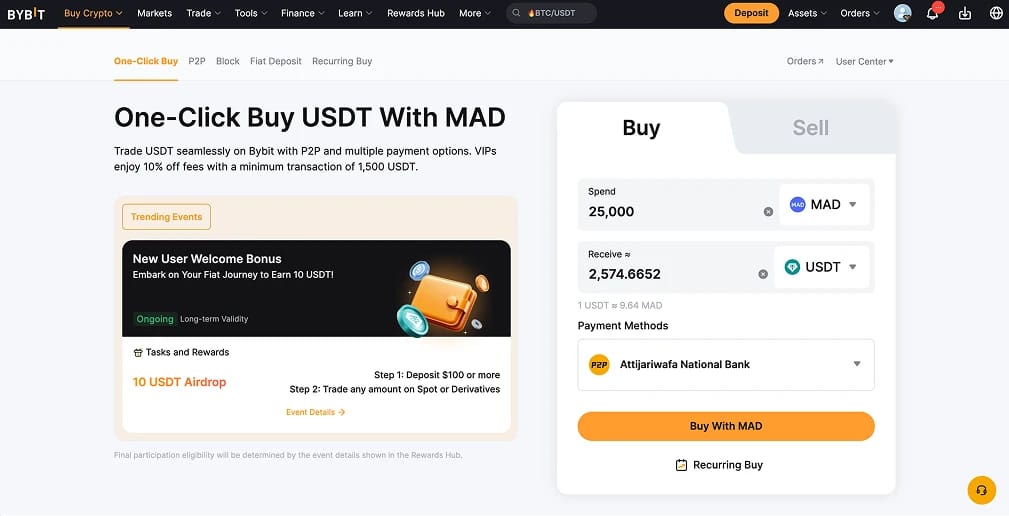

Bybit is the platform I send most first-time buyers in Morocco to. The MAD P2P desk has been live since 2022, the merchant pool keeps expanding through Bybit's MENA Fast Track programme, and the buy/sell flow is cleaner than most rivals. Spot fees are a flat 0.1% maker and taker.

What makes Bybit work in Morocco is the breadth of payment options on the MAD desk. Bank transfers from Attijariwafa, BCP, CIH, and BMCE are common, with Wafacash, Wise, and card listings depending on the merchant. The interface is available in French, which matters more than people realise once you are dealing with KYC documents and dispute resolution.

I funded a 2,000 MAD test order through a verified merchant via CIH transfer. Escrow released in twelve minutes. The USDT/MAD rate sat 1.5 to 2.5% above the implied dirham/dollar mid-market rate, in line with what you would expect on any P2P desk for a controlled currency.

Beyond the on-ramp, Bybit covers 2,500+ assets across spot, perpetual futures up to 200x leverage, copy trading, and a Web3 wallet that bridges into DeFi without leaving the app. Bybit also publishes monthly proof-of-reserves attestations, a meaningful signal when you are trusting an offshore platform with no Moroccan licence.

Pros

- MAD P2P desk supports the major Moroccan banks plus Wafacash and Wise, with French-language interface and support.

- Spot fees of 0.1% maker and taker, futures fees among the lowest in the industry.

- Monthly proof-of-reserves disclosures and a recovered security posture after the February 2025 cold wallet incident.

Cons

- No direct card or bank wire in MAD outside the P2P marketplace.

- Not licensed by Bank Al-Maghrib, like every foreign exchange Moroccans use.

- The product menu is dense. Beginners should switch to Lite mode immediately.

2. Binance

Binance has the deepest MAD/USDT P2P book of any exchange operating in Morocco by a wide margin. The platform added MAD support in April 2020 and has expanded its MENA payment methods through 2024 and 2025 to cover Wafacash, CashPlus, and most major Moroccan bank transfers. If you have used Binance P2P here, you already know merchant counts during Casablanca and Rabat business hours are several times what Bybit or Bitget show.

The depth shows up in pricing. In side-by-side March 2026 comparisons, Binance MAD/USDT spreads ran 0.3 to 0.8% tighter than the next nearest competitor on orders between 1,000 and 10,000 MAD. On larger orders the gap widens. For anyone moving meaningful size in dirhams, that is the practical reason Binance is still the default.

The trade-off is regulatory exposure. Binance does not hold a Bank Al-Maghrib licence, and the Office des Changes still treats unauthorised crypto trading as a foreign exchange violation. The platform is reachable from Morocco without a VPN, but using it puts you in the same legal grey zone as every other Moroccan crypto user. Once funded, you get spot, margin, futures with up to 125x leverage, Launchpool, Earn, Auto-Invest, and the deepest order books in the industry on BTC/USDT and ETH/USDT.

Pros

- Deepest MAD P2P book available anywhere. More merchants, tighter spreads, faster fills.

- Wide payment method coverage including Wafacash, CashPlus, Wise, and most Moroccan bank transfers.

- Order book liquidity on majors keeps execution clean even in volatile sessions.

Cons

- Regulatory scrutiny across multiple jurisdictions creates platform risk worth monitoring.

- Feature set is heavy. New users frequently get lost finding the basic spot tab.

- P2P dispute resolution during peak hours can drag. Stick to merchants with high completion rates.

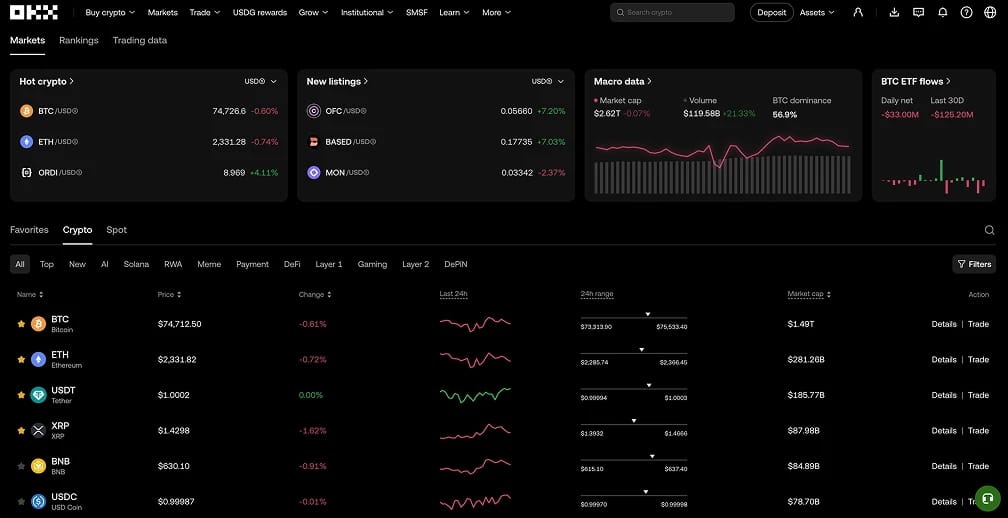

3. OKX

OKX is the exchange to look at if you want one platform handling both centralised trading and on-chain DeFi. The built-in OKX Wallet is non-custodial, supports 130+ chains, and connects directly to dApps, NFT marketplaces, and DEX aggregators without MetaMask or any third-party tool.

OKX P2P supports MAD through bank transfer and card listings, but the merchant count is noticeably thinner than Binance or Bybit. Expect fewer options and slightly wider spreads, particularly outside Moroccan business hours. On orders under 1,000 MAD that gap matters. On larger orders the rates tighten.

Where OKX clicks is the centralised-to-on-chain bridge. You can buy USDT through P2P, swap to ETH on spot, then move it into a DeFi protocol or stake it through OKX Wallet without leaving the app. Spot fees start at 0.08%, the lowest base rate in this comparison, and the TradingView integration is genuinely best in class for charting. OKX publishes monthly proof-of-reserves disclosures that hold up against any platform on this list.

Pros

- Built-in Web3 wallet bridges centralised trading and DeFi without third-party tools.

- 0.08% base spot fee, the lowest in this comparison.

- Monthly proof-of-reserves and a clean, well-organised pro interface.

Cons

- MAD P2P merchant count lags Bybit and Binance. Spreads on smaller orders run wider.

- Web3 features add complexity that pure stablecoin holders will never use.

- For a quick BTC purchase via Moroccan bank transfer, this is more platform than the job needs.

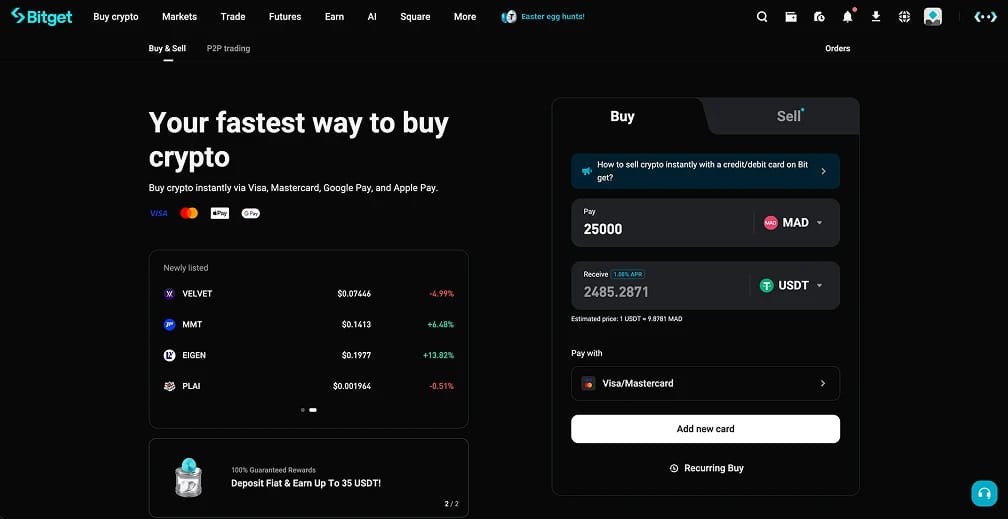

4. Bitget

Bitget earns its place through copy trading, built as a first-class product rather than a side feature. Strategy selection is deeper than rivals, performance history is transparent, and the risk controls let you size exposure properly. For Moroccan traders who want to follow a system without building their own bot, this is the best implementation in the region.

MAD P2P on Bitget covers bank transfers from major Moroccan banks plus Wise and a handful of e-wallets. Merchant count is decent without being deep. I funded a test order via Wise and escrow released in eight minutes. Once funded, you get spot and futures across 800+ cryptocurrencies, grid and DCA bots, and launchpool access.

The trust signals stand out for an offshore platform with no local regulatory cover. Bitget's February 2026 proof-of-reserves report showed a 169% total reserve ratio, and the protection fund averages above $400 million backed by 6,500 BTC. For Moroccan users with no Bank Al-Maghrib safety net, those cushions matter.

Pros

- Best-in-class copy trading product with strong strategy selection and risk management.

- $400M+ protection fund and 169% proof-of-reserves ratio provide stronger trust signals than most offshore platforms.

- French-language interface and customer support in line with how most Moroccan users navigate the platform.

Cons

- MAD P2P merchant count does not match Binance or Bybit. Off-peak liquidity can thin out.

- Copy trading makes it easy to take leverage exposure you have not properly sized.

- Feature set tilts toward active trading. Less of a fit for buy-and-hold users.

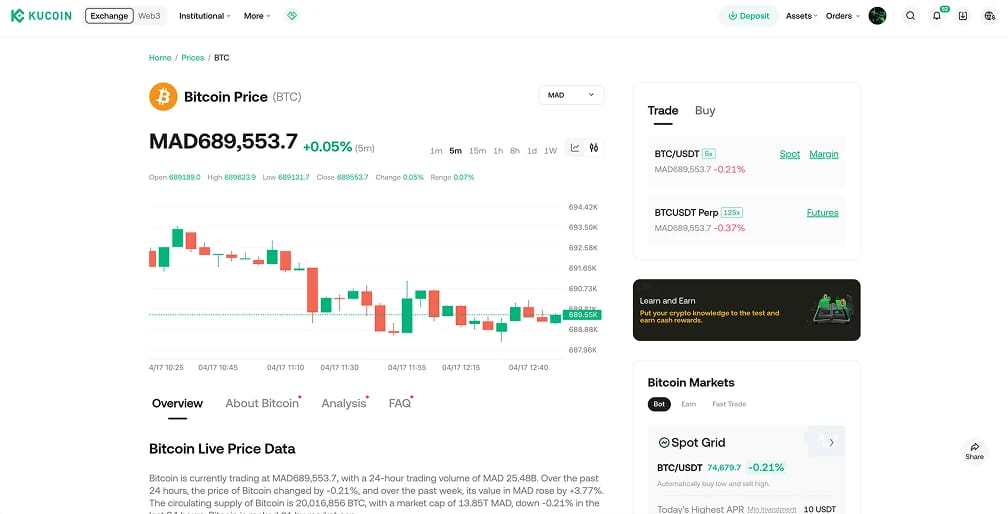

5. KuCoin

KuCoin sits in the middle of this list. The MAD P2P desk is functional but thin, and most Moroccan KuCoin users I know fund elsewhere first and move USDT in via TRC20 transfer. As a primary on-ramp it is harder to recommend. As a secondary venue for altcoin exposure, it earns its slot.

KuCoin lists over 1,000 cryptocurrencies, and the GemSPACE listing hub consistently picks up smaller-cap projects earlier than Bybit or Binance. If your strategy involves rotating into newer narratives, this is where you find names before they hit the major exchanges. Spot fees start at 0.1%, futures go up to 100x, and the trading bot suite covers grid, DCA, and rebalance strategies.

KuCoin's operating entity Peken Global pleaded guilty in January 2025 to operating an unlicensed money transmitting business in the US, paying $297 million in penalties and exiting the American market for two years. The compliance programme has been rebuilt since, but for Moroccan users weighing how much to leave on the platform, it is worth pricing in.

Pros

- 1,000+ assets with early access to emerging altcoins via GemSPACE.

- $1 minimum order makes it easy to test the platform without meaningful risk.

- Mature trading bots and a useful Earn product for yield on idle USDT.

Cons

- MAD P2P liquidity is thin. Most users fund via TRC20 transfer from another platform.

- January 2025 unlicensed money transmission guilty plea is worth factoring in when sizing balances.

- Better as an altcoin venue than a primary MAD on-ramp.

6. Gate

Gate is on this list for one reason: 4,400+ cryptocurrencies, roughly nine times what you get on Binance and over twelve times OKX. If you are hunting newly listed tokens or smaller-cap altcoins that never reach the majors, Gate almost always has them.

The catch in Morocco is funding. Gate does not run a meaningful MAD P2P desk, so the way in is credit or debit cards processed in USD, or a crypto deposit from another exchange. Visa and Mastercard sometimes work, but international crypto purchases are exactly the kind of foreign exchange flow Bank Al-Maghrib monitors, and several major banks flag or decline them outright. Test small first.

If you can get past the funding hurdle, Gate is solid on the trading side. Spot, futures up to 100x, margin, copy trading, and Simple Earn are all available. Gate has been operating since 2013 without a major security breach, and proof-of-reserves disclosures have consistently shown a reserve ratio above 125%.

Pros

- Largest token selection of any exchange on this list. Over 4,400 cryptocurrencies.

- Operating since 2013 with no major security incidents and consistent proof-of-reserves above 125%.

- Strong futures and copy trading products for active traders.

Cons

- No meaningful MAD P2P. You are dependent on card payments or crypto deposits from another platform.

- Moroccan bank cards frequently decline or trigger fraud alerts on international crypto purchases.

- The interface feels busy and the sheer listing volume can overwhelm new users.

How to Choose a Crypto Exchange in Morocco

Picking an exchange in Morocco is not the same as picking one in France or Spain. There is no licensed local platform yet, no consumer protection if something goes wrong, and no clean legal path under the current 2017 framework. The standard "choose a regulated platform" advice from European guides barely applies because none of these platforms are licensed by Bank Al-Maghrib or registered with the AMMC.

The decision comes down to four practical questions.

Step 1: Test the MAD P2P desk before depositing anything

Open the P2P section before committing to a platform. Filter for MAD, count active merchants during Moroccan business hours, and check the spread against the implied USDT/MAD rate. A healthy desk shows at least 20 active merchants during the day, spreads within 1.5 to 2.5% of mid-market, and completion rates above 95% on the merchant profiles you are considering.

Binance and Bybit consistently have the deepest MAD desks. Bitget is workable. OKX and KuCoin run thinner. Gate effectively does not have one.

Step 2: Test card payments with a small amount first

Planning to use a Visa or Mastercard from a Moroccan bank? Test with the smallest possible purchase first, ideally under 100 MAD. Cross-border crypto purchases are exactly what Bank Al-Maghrib actively monitors, and several Moroccan banks have been reported to decline or freeze them. The major banks worth being cautious with include:

Smaller banks and payment institutions tend to flag transactions less aggressively, but nothing is guaranteed. If your card gets blocked once, expect an awkward conversation with the fraud desk.

Step 3: Complete KYC properly with a CNIE or passport

Every exchange on this list requires identity verification before you can use P2P or withdraw at scale. In Morocco that means your Carte Nationale d'Identité Électronique (CNIE) or passport, plus a selfie and sometimes proof of address. Common reasons verification stalls: name mismatches between your CNIE and account profile, blurry document photos, or the Latin transliteration of an Arabic name not matching exactly across documents. Get those aligned before uploading.

The new draft framework under Bill 42.25 is moving toward stricter KYC, not looser. The direction of travel is more identification, not less.

Step 4: Calculate the real round-trip cost

Headline trading fees of 0.1% are the smallest piece of what you actually pay. The real cost lives in three layers:

- The P2P spread on the way in (MAD to USDT): typically 1.5 to 3% above the mid-market rate

- The exchange spot trading fee: 0.08% to 0.2%

- The withdrawal fee plus the P2P spread on the way out

A platform advertising 0.1% spot fees can easily cost 4 to 5% all-in once you factor both ends of the round trip. Run a small MAD to USDT to MAD cycle on any platform you are considering and measure the slippage. That number is the only one that matters for an honest fee comparison.

How Morocco Regulates Cryptocurrency

Morocco's crypto framework is in transition. The 2017 ban remains the operative law, but Bill 42.25 is moving through Parliament and will reshape the market through 2026 and 2027.

The Current Ban

The current rules rest on a November 2017 notice from the Office des Changes declaring that cryptocurrency transactions violate exchange regulations. The basis traces back to Morocco's foreign exchange controls, which restrict how dirhams can leave the country and which foreign currencies Bank Al-Maghrib recognises. Crypto sat outside that perimeter, and the ban closed the gap.

Enforcement has been uneven. Individuals trading on unlicensed platforms face fines between MAD 20,000 and MAD 100,000, businesses up to MAD 500,000. In practice, enforcement has targeted businesses, OTC operators, and large-scale users rather than individuals running personal P2P trades. The legal exposure is still real, particularly for cross-border flows.

Bill 42.25 and What Changes

The shift began in November 2024, when Bank Al-Maghrib Governor Abdellatif Jouahri confirmed a draft crypto law was in preparation. In November 2025, the Ministry of Economy and Finance published Bill 42.25 for public consultation, jointly developed with Bank Al-Maghrib and the AMMC. The bill is modelled on the EU's MiCA framework and aligned with FATF, BIS, and IMF recommendations.

Under Bill 42.25:

- AMMC licenses and supervises Crypto-Asset Service Providers (CASPs), oversees token issuance, and enforces market integrity rules.

- Bank Al-Maghrib retains authority over stablecoins and asset-referenced tokens.

- ANRF, a new National Financial Intelligence Agency, handles AML and CFT compliance.

- CASPs must be incorporated in Morocco, hold minimum capital around MAD 3 million, and process transactions in dirhams only. Direct MAD-to-USD or EUR conversion within the platform is not permitted, preserving the original foreign exchange control objective.

Timeline and Limitations

Parliamentary review runs through Q1 and Q2 2026, with potential adoption by mid-year. The AMMC will then publish implementing regulations, and the first licences are likely to be issued in late 2026 or early 2027. Until then, foreign exchanges remain unlicensed and P2P stays in the grey zone.

Two limitations matter. First, Bill 42.25 does not legalise crypto for payments, so Bitcoin will remain prohibited as a means of settling goods and services. Second, the bill excludes DeFi, NFTs, and crypto mining. Mining stays banned because it sits at the intersection of foreign exchange controls (imported hardware, exported electricity) and energy policy.

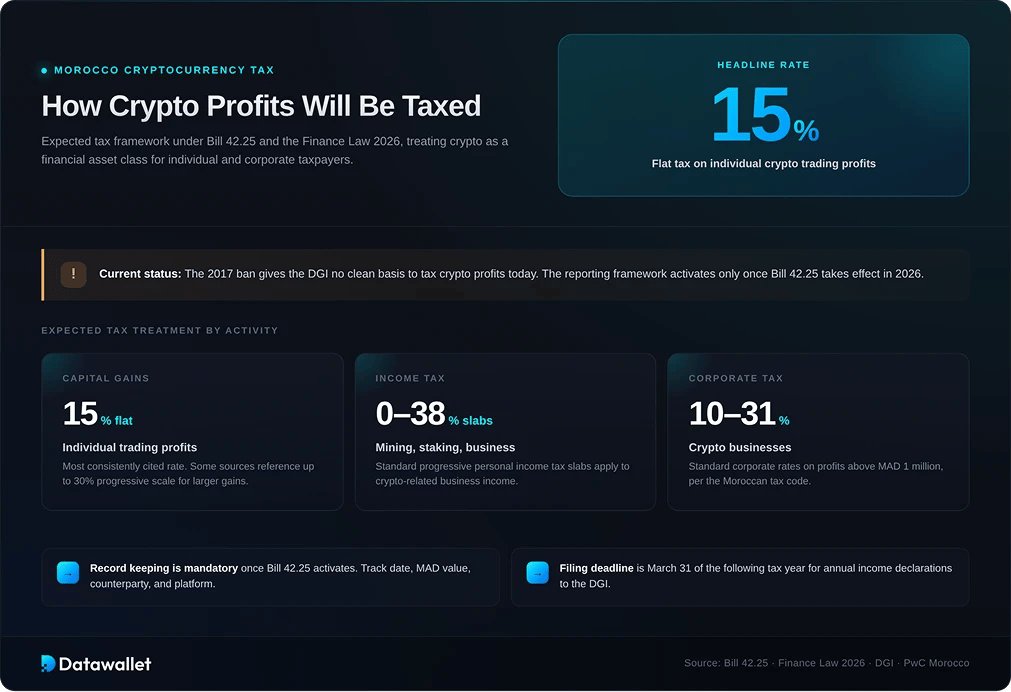

How Morocco Taxes Cryptocurrency

Morocco has no dedicated cryptocurrency tax regime as of April 2026. The 2017 ban created an awkward dynamic: the Office des Changes treats crypto transactions as illegal under foreign exchange law, but the Direction Générale des Impôts (DGI) has been preparing a parallel framework under the broader regulatory reform.

The expected framework, tied to the Bill 42.25 timeline and the Finance Law 2026, treats crypto as a financial asset for tax purposes:

- Capital gains: A flat rate around 15% on individual crypto trading profits is the most consistently cited figure in published draft guidance. Some sources reference a higher progressive scale up to 30% for larger gains, though the final rate has not been confirmed in legislation.

- Income tax: Mining, staking, and crypto-related business income would fall under standard progressive personal income tax slabs, which run from 0% to 38% depending on bracket. The corporate tax range is 10% to 31% on profits above MAD 1 million, per the PwC Morocco tax summary.

- VAT: The standard 20% VAT is unlikely to apply to crypto transactions themselves under the proposed framework, in line with EU treatment.

- Record keeping: Mandatory once the framework is in force. Even before it takes effect, keeping clean records of every transaction (date, MAD value, counterparty, platform) makes future compliance considerably easier.

In practice, most Moroccan crypto users do not currently report gains because the 2017 ban gives the DGI no clean basis to assess crypto income. That gap closes once Bill 42.25 takes effect. If your holdings are meaningful and you plan to convert at scale, talk to a Moroccan tax professional before filing season. The transitional period between the old and new regimes is exactly when documentation matters most.

Cryptocurrency Adoption in Morocco

Morocco is one of the more interesting crypto adoption stories in North Africa. Despite the 2017 ban, the country climbed to 24th in the Chainalysis 2025 Global Crypto Adoption Index, up from 27th the year before. That makes Morocco the highest-ranked country in North Africa, ahead of Algeria, Tunisia, and Egypt.

Around six million Moroccans hold crypto wallets, or roughly 16% of the population, representing 60% growth over five years. The market is projected to reach $292 million in 2026.

The drivers are practical, not speculative:

- Remittance demand: Morocco received around $12.8 billion in remittances in 2024, with France alone accounting for the largest single corridor through the 1.5 million-strong Moroccan diaspora. Western Union and bank wires charge 3 to 5%. USDT on TRC-20 brings that closer to 1.5 to 2.5% all-in, including the conversion spread.

- USDT as a dollar proxy: The dirham trades within a 5% band of a basket weighted 60% to the euro and 40% to the US dollar, with foreign exchange controls limiting how Moroccans can hold or move dollar-denominated value. USDT has become the workaround.

- Underbanked population: Morocco has historically had one of the lower banking penetration rates in the region, particularly outside the major cities. For the population already operating in cash, mobile-first crypto via Wafacash and CashPlus is a shorter step than traditional banking.

- Young, mobile-first demographics: Median age around 29, mobile penetration above 120% of population, and rising internet access. The cohort most likely to adopt crypto is also the largest demographic group in the country.

Adoption is balanced rather than concentrated. Chainalysis notes Morocco ranks similarly across retail centralised activity (20th globally), total centralised value (23rd), DeFi (25th), and institutional flows (28th), suggesting a diversified user base rather than concentration in any single use case.

%201.webp)

How to Buy Bitcoin in Morocco

Buying Bitcoin from Morocco in 2026 comes down to finding a reliable MAD funding path, completing KYC without issues, and converting cleanly without giving up too much in spread. Here is the process I follow:

- Pick a platform with a deep MAD P2P desk: Open the P2P section first. Check MAD merchant count, payment methods, and recent completion rates. Bybit and Binance consistently perform best. If the desk looks thin, move on.

- Complete KYC before funding: Finish verification with your CNIE or passport before attempting any P2P trade. Some exchanges lock P2P behind KYC, and a stuck verification with money in escrow is the scenario you want to avoid.

- Buy USDT through P2P: The cleanest path is buying USDT through P2P using a Moroccan bank transfer, Wafacash, or Wise. Compare merchant pricing carefully. USDT/MAD rates can vary by 1 to 3% depending on the merchant and time of day. Always use the platform's escrow. Never trade outside it.

- Trade USDT for BTC on spot: Once USDT is in your wallet, place an order on the BTC/USDT pair. Limit order for price control, market order when speed matters. Skip the one-click "buy crypto" screen. The spread baked into it costs more than a normal spot trade.

- Withdraw to self-custody: If you are not actively trading, move your BTC off-exchange to a hardware wallet. Ledger and Trezor are the strongest options. Double-check the network selection and withdrawal fee before confirming.

That gives you the most cost-effective way into Bitcoin from Morocco today. Avoid card payments when possible, and stay away from informal OTC operators on Telegram or WhatsApp that sit outside any escrow system.

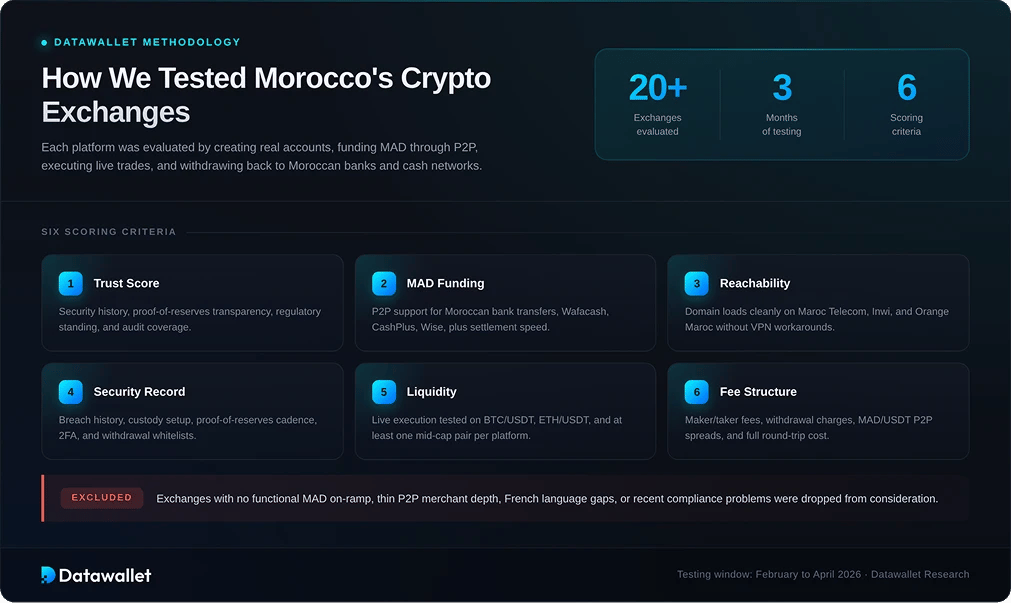

Our Methodology

We evaluated over 20 crypto exchanges available in Morocco by creating accounts, funding MAD through P2P, executing trades, and withdrawing back to Moroccan bank accounts and cash pickup networks. Each platform was scored across six criteria:

- Trust Score: Our proprietary rating (out of 5) weights security history, proof-of-reserves transparency, regulatory standing, platform longevity, and audit coverage. Exchanges with published reserves and clean operating histories scored highest.

- MAD Funding Methods: Confirmed bank transfer, Wafacash, CashPlus, Wise, and card support through P2P, while testing settlement speed, merchant depth, and spread against mid-market USDT.

- Access and Reachability: Checked whether the domain loads cleanly on Moroccan ISPs (Maroc Telecom, Inwi, Orange Maroc), and whether the platform functions without workarounds for users in Casablanca, Rabat, and Marrakech.

- Security Track Record: Reviewed breach history, custody setup, proof-of-reserves cadence, and account protections like 2FA and withdrawal whitelists.

- Assets and Liquidity: Tested execution by placing market and limit orders on BTC/USDT, ETH/USDT, and at least one mid-cap pair.

- Fee Structure: Compared maker/taker fees, withdrawal charges, P2P spread on MAD/USDT, and the all-in cost of a dirham-to-USDT round trip.

We excluded exchanges with no functional MAD on-ramp, thin P2P merchant depth, French language gaps that made the platform unusable for the average Moroccan user, or serious recent compliance problems. Testing ran from February to April 2026.

Final Thoughts

Crypto in Morocco in 2026 is a market in transition. The 2017 ban is still on the books, Bill 42.25 is moving through Parliament, and the first licensed platforms are 12 to 18 months away. Until then, every Moroccan crypto user is operating in the same grey zone, choosing between offshore platforms with no local regulatory cover.

The exchanges in this guide are the practical choices for that environment. Start with the MAD P2P desk, not the marketing page. If a platform cannot reliably get dirhams in and out, nothing else matters. Bybit and Binance are strongest on funding. OKX is the right pick for one app bridging centralised trading and DeFi. Bitget makes sense for copy trading and stronger trust signals than most offshore platforms. KuCoin and Gate are secondary venues worth keeping an account on if you trade altcoins seriously.

Whatever platform you settle on, complete KYC properly, test your funding method with a small amount first, and measure the full round-trip cost before committing meaningful capital. That groundwork will save you more than any fee table ever will.