Who is Chamath Palihapitiya?

Chamath Palihapitiya is a Sri Lankan-born Canadian and American venture capitalist, the founder and CEO of Social Capital, and a co-host of the All-In Podcast, which has become one of the most influential business and political shows in the United States.

He occupies an unusual position in finance. He is credited with one of the great growth-engineering runs in tech history, having driven Facebook from roughly 50 million users past 700 million, and is blamed for a SPAC boom that left most retail participants underwater. Both reputations are earned, and his net worth reflects the whiplash between them.

What we find most distinctive about Chamath is how publicly he keeps score. He posts annual performance letters, discloses losses on his own podcast, and admits mistakes with a bluntness most fund managers avoid. That transparency cuts both ways, because his misses are as documented as his wins.

.webp)

Chamath Palihapitiya's Background

Chamath's path runs from a refugee household in Ottawa through AOL, Facebook, venture capital, SPAC mania, and now a second act centered on AI infrastructure and a redesigned blank-check vehicle.

Early Life and Education

Chamath Palihapitiya was born on September 3, 1976, in Galle, Sri Lanka. His family moved to Ottawa when he was five, where his father sought refugee status amid Sri Lanka's civil conflict. Money was tight; he worked at Burger King as a teenager to help support the household.

He attended Lisgar Collegiate Institute and then the University of Waterloo, graduating in 1999 with a degree in electrical engineering. His first job was trading derivatives at BMO Nesbitt Burns, a brief detour before he moved to California.

AOL and Facebook

At AOL, Chamath ran the instant messaging division covering AIM and ICQ, becoming the company's youngest vice president at 26. In 2007, he joined Facebook, leading the growth team through the platform's most explosive years.

The growth playbook his team developed, obsessive measurement of activation, retention, and viral loops, became standard practice across consumer tech. He left Facebook in 2011 and sold his remaining stock in 2014. He has since been one of the company's harshest critics, telling a Stanford audience in 2017 that the tools he helped build were tearing at the social fabric.

Building Social Capital

Chamath founded The Social+Capital Partnership in 2011, raising successive funds and backing companies including Slack, Yammer, and Box. The same year, he paid $25 million for a 10% stake in the Golden State Warriors, joining Joe Lacob's ownership group shortly after its $450 million takeover.

In 2018, he stopped accepting outside capital and converted Social Capital into a holding company investing in his own balance sheet. That decision is why his wealth is so opaque today. There are no fund filings to audit, only the positions he chooses to discuss.

The SPAC Era

In 2017, Chamath and Ian Osborne launched Social Capital Hedosophia, the first in a planned series of SPACs with tickers ranging from IPOA to IPOZ. IPOA merged with Virgin Galactic in 2019, and the follow-ups brought Opendoor, Clover Health, and SoFi to public markets during the 2020 to 2021 frenzy.

The aftermath was brutal. Virgin Galactic fell more than 95% from its highs, Clover collapsed, and in 2022, he wound down two unmerged SPACs, returning roughly $1.6 billion to investors. Of his completed deals, only SoFi trades meaningfully above its $10 offer price. He sold early in several cases, including 6.2 million Virgin Galactic shares for about $213 million in March 2021.

His Warriors exit followed a different kind of pressure. After his January 2022 comments about the Uyghur genocide drew widespread condemnation, he sold his remaining stake in mid-2022, a position that had appreciated roughly tenfold over eleven years.

The Comeback: Groq and AEXA

Two events define his current chapter. The first is Groq, the AI inference chip company that Social Capital backed with $10 million in 2017 and another $52.3 million in 2018, investments that gave the firm close to one-third ownership at the time. In December 2025, Nvidia agreed to pay about $20 billion in cash for Groq's assets, IP license, and senior team, the largest transaction in Nvidia's history.

The second is his SPAC return. In September 2025, American Exceptionalism Acquisition Corp (AEXA) raised $345 million on the NYSE to target AI, energy, defense, and decentralized finance. The structure answers his critics directly: no warrants, sponsor shares that only vest if the stock rises 50% above the IPO price, and just 1.3% of the offering allocated to retail.

.webp)

Chamath Palihapitiya's Net Worth in 2026

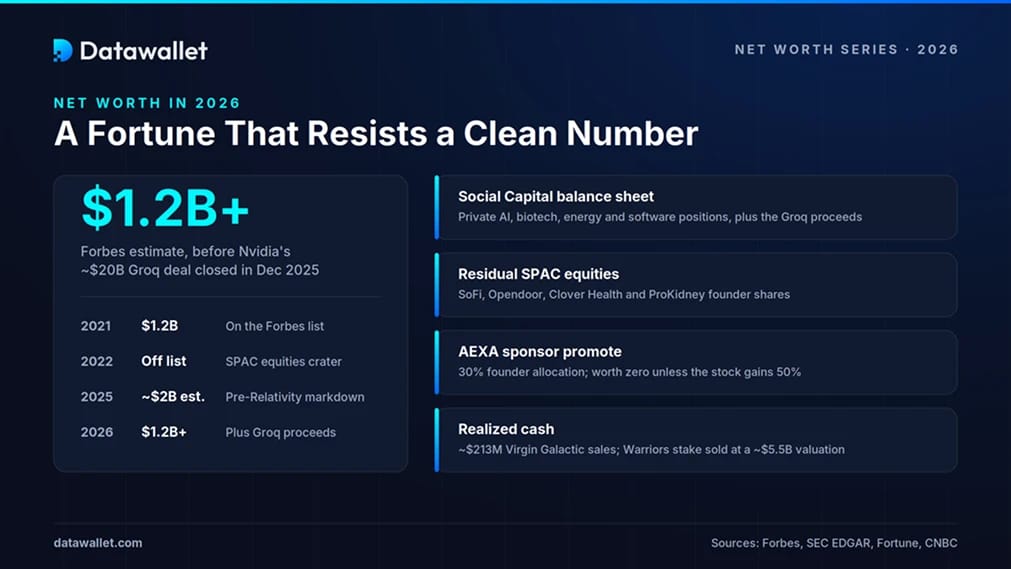

Chamath Palihapitiya's net worth in 2026 sits somewhere between $1.2 billion and several multiples of that, and the honest answer is that nobody outside Social Capital knows precisely.

We checked his trajectory across the available estimates, and the swings are extreme even by tech standards. Forbes pegged him at $1.2 billion in 2021, then dropped him from its billionaires list entirely in 2022 as his SPAC-linked equities cratered.

Estimates recovered toward $2 billion by 2025 before the Relativity Space writedown, where he disclosed on All-In that he had lost roughly $380 million after the rocket company's recapitalization led by Eric Schmidt.

The main components of his wealth today are:

- Social Capital balance sheet: His holding company spans private positions in AI, biotech, energy, and software, including the Groq proceeds. He has described the portfolio in annual letters but discloses no audited totals.

- Public equities from SPAC sponsorship: Residual founder shares positions in SoFi, Opendoor, Clover Health, and ProKidney, visible through SEC insider filings but worth a fraction of their 2021 marks.

- AEXA sponsorship: His sponsor position in the new SPAC carries a 30% founder allocation, but it is worth nothing unless the post-merger stock appreciates 50%.

- Realized cash: Past exits add up, including about $213 million from personal Virgin Galactic sales and a Warriors stake sold across 2021 and 2022 at a franchise valuation near $5.5 billion, against a $25 million entry.

Chamath Palihapitiya's Investment Portfolio

Chamath's portfolio runs through Social Capital, which he converted into a permanent-capital holding company in 2018. Per his 2024 annual letter, the firm managed about $2.1 billion against $1.4 billion in paid-in capital, and his 2025 letter describes repositioning it as an "unexploitable portfolio" for the AI era.

The positions that matter most:

- Groq (exited): Social Capital's $62.3 million across 2017 and 2018 became the portfolio's defining win when Nvidia paid about $20 billion for Groq's assets in December 2025.

- 8090: A self-funded incubator announced in January 2024 to rebuild enterprise software with AI at a fraction of normal cost. Its flagship Software Factory product shipped in February 2026, and he framed 2025 as the year he scaled it.

- Residual SPAC equities: Founder shares positions in SoFi, Opendoor, Clover Health, and ProKidney remain visible through SEC filings, though only SoFi has held up.

- Relativity Space (written down): The 3D-printed rocket maker absorbed roughly $380 million of his capital before Eric Schmidt's recapitalization wiped out earlier holders in 2025.

- AEXA: His sponsor stake in the $345 million SPAC is structured so founder shares vest only at a 50% premium to the IPO price.

The pattern across two decades is consistent: a small number of concentrated, often illiquid bets, held through volatility that would force most fund managers to sell.

Chamath Palihapitiya's Crypto Holdings

Chamath's crypto story is mostly about Bitcoin he no longer owns. He started buying in 2012 and 2013, both personally and through Social Capital, and by late 2013, TechCrunch reported he held about $5 million in BTC, then one of the largest known individual positions in the world.

He later distributed and sold those holdings, a decision he has publicly regretted. In November 2024, with Bitcoin past $90,000, he called the sale a "three or four billion dollar" mistake on All-In. We struggle to think of another investor who has quantified a missed crypto position that precisely, on the record, against his own interest.

His current exposure is structural rather than direct. He has long argued that Bitcoin's role is to displace gold while stablecoins absorb dollar payment rails, a thesis that now looks prescient given how the stablecoin market has scaled.

AEXA explicitly lists decentralized finance among its target sectors, and he has pointed to Circle's public-market success as evidence that DeFi's next phase runs through regulated, listed companies. He has also said he prefers holding equities of companies that own crypto over managing coins and wallets himself.

Final Thoughts

Chamath Palihapitiya's net worth resists the clean, tickable number that someone like Brian Armstrong carries, and that opacity is by design. Once he closed Social Capital to outside money, he traded accountability to limited partners for total discretion, and the public is left triangulating between Forbes estimates, SEC filings, and whatever he volunteers on a podcast.

The 2026 picture is stronger than the 2022 one by a wide margin. The Groq outcome vindicates the kind of early, concentrated hardware bet that his SPAC record had overshadowed, and AEXA's restructured incentives suggest he absorbed at least some of the criticism.

Whether the second act ends differently from the first depends on a deal he has not yet announced. What we would watch is not the headline number but the same thing that has always driven it: one or two outsized, illiquid positions that either compound quietly for a decade or unwind in public.

.webp)