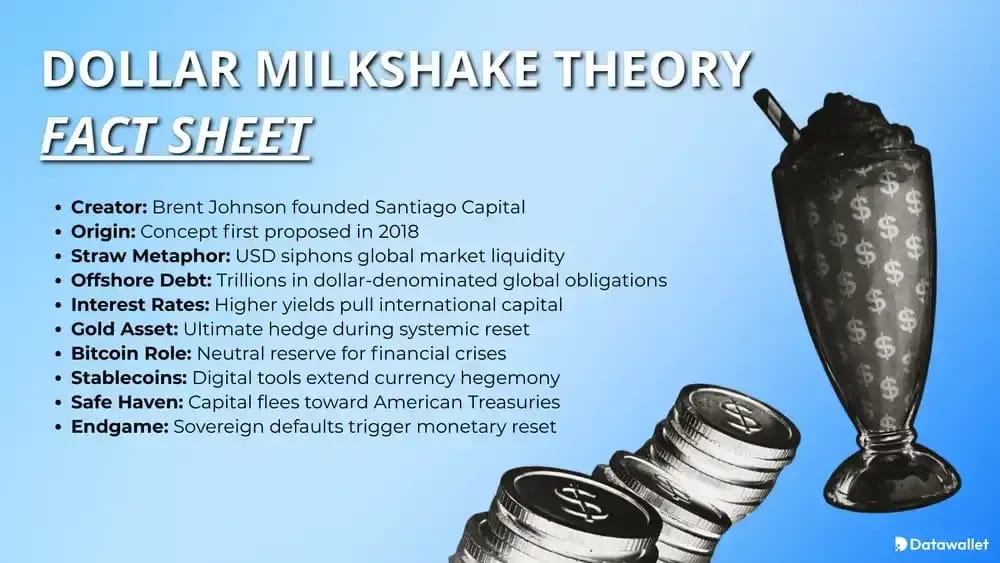

What is the Dollar Milkshake Theory?

The Dollar Milkshake Theory is a macro framework from Brent Johnson, founder of Santiago Capital, using a “milkshake” metaphor: global liquidity mixes together, but the US dollar acts as the straw that concentrates demand during stress, giving the United States an unusually strong financial pull.

Johnson says he introduced the idea in presentations around October 2018 and expanded it at the MacroVoices conference in January 2019. The thesis links rising US rates and tighter dollar funding to a self-reinforcing dollar rally.

Under the thesis, rising US rates, scarce offshore dollar funding, and demand for Treasuries can pull liquidity from weaker economies first. The result is a stronger dollar, tighter global conditions, and stress for countries or borrowers carrying dollar liabilities.

Economists do not treat the theory as doctrine, but parts of it overlap with established views on dollar shortages, reserve-currency demand, and crisis flight to safety. Its popularity has been high in macro-investing and crypto circles while mainstream economists remain skeptical.

Dollar Milkshake Theory Components

Core ingredients of the Dollar Milkshake include global liquidity creation, reserve-currency status, offshore dollar debt, eurodollar funding markets, interest-rate differentials, capital flight, safe-haven demand, sovereign debt risk, and the possibility that gold or Bitcoin eventually absorb distrust in fiat assets.

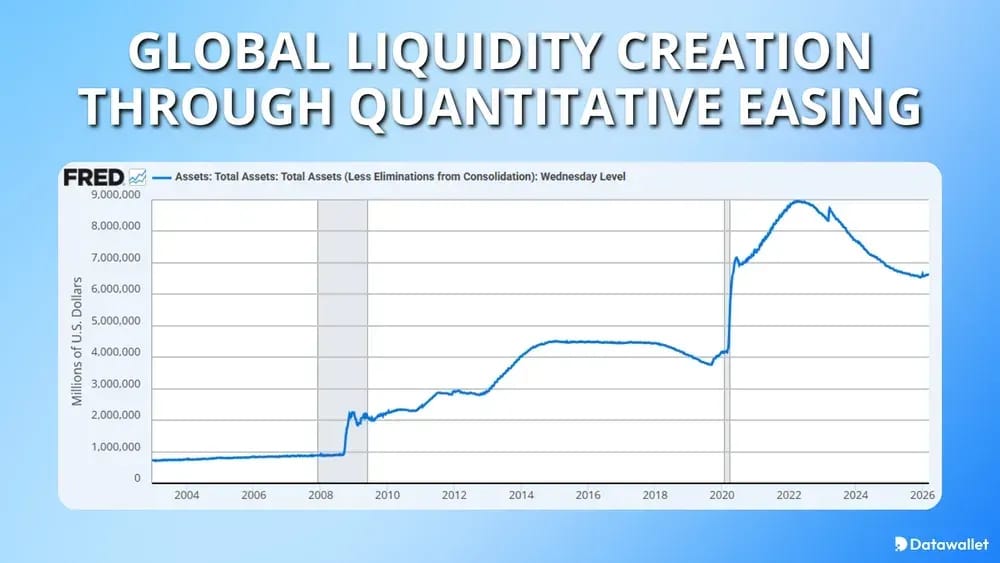

1. Global Liquidity Creation

Johnson’s metaphor starts with the “milkshake” itself: years of quantitative easing, low rates, and coordinated stimulus across major economies. In his framing, central banks filled the world with liquidity, but not all currencies retained equal power once stress returned.

That matters because a shared global easing cycle can inflate asset prices everywhere, then leave capital hunting for the deepest, safest, and most liquid destination. Johnson argues the US system, despite its flaws, still offers the strongest straw during panics.

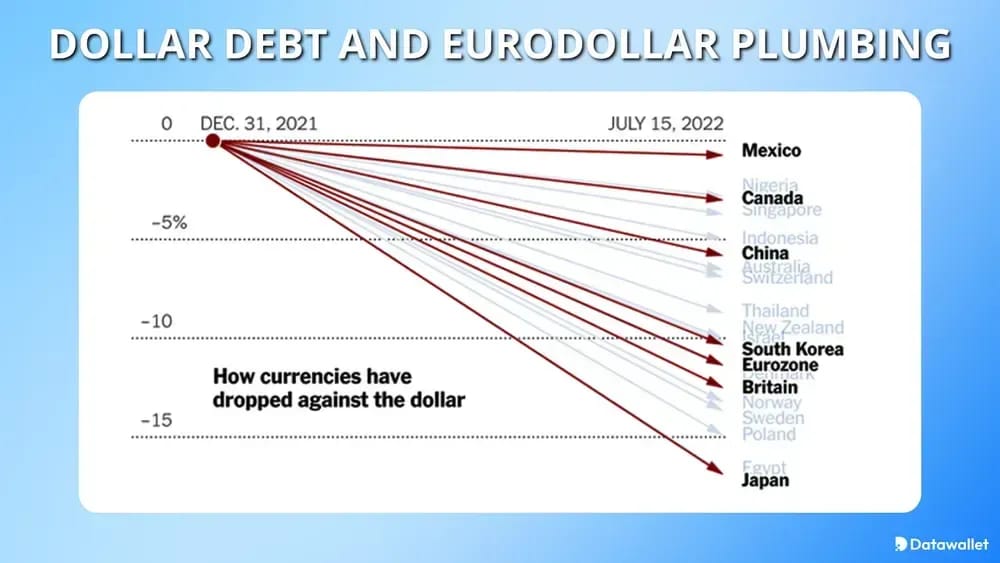

2. Dollar Debt And Eurodollar Plumbing

A major pillar of the theory is the world’s dependence on dollar liabilities outside the United States. BIS research shows large on-balance-sheet and off-balance-sheet dollar obligations across non-US borrowers, making dollar funding conditions globally important.

When refinancing becomes harder, borrowers do not need to love the dollar to need it. They simply need dollars to roll debt, meet collateral calls, or settle obligations, which can intensify squeezes and reinforce dollar strength.

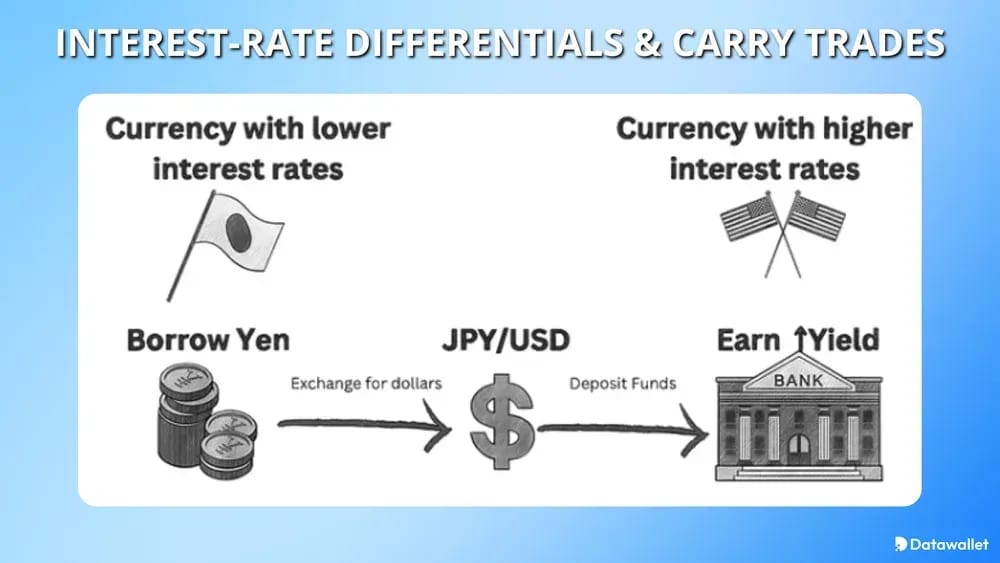

3. Interest-Rate Differentials And Carry Trades

Rate spreads help explain why capital can keep migrating into dollar assets, especially when US yields look safer or more attractive than alternatives.

- Carry Trade Pressure: Higher US yields can pull leveraged capital (carry trade) toward dollar assets and away from fragile local markets when volatility spikes.

- Policy Divergence: Even when other central banks ease too, the Fed’s relative stance can still matter because global investors compare returns, liquidity, and credibility.

- Reflexive Strengthening: A firmer dollar can worsen external debt burdens abroad, which then creates even more emergency demand for dollars.

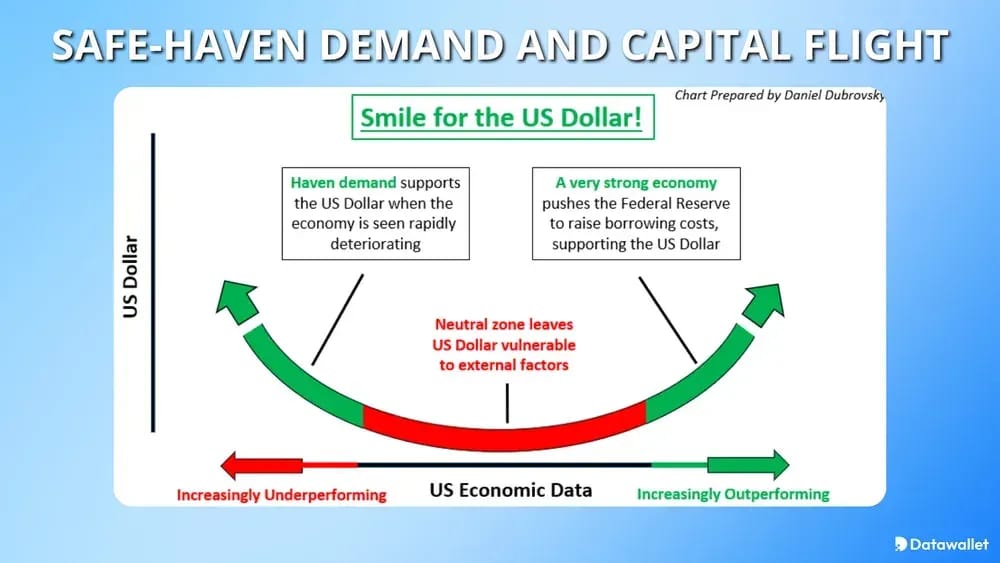

4. Safe-Haven Demand And Capital Flight

The theory also assumes crises redirect capital toward the balance sheets and markets perceived as most liquid, collateral-rich, and globally acceptable.

- Treasury Preference: In stressed markets, investors often still reach for US Treasuries and dollar cash because they remain core collateral in global finance.

- Institutional Inertia: Reserve managers and large allocators may dislike US policy, yet still lack a market with equal scale, convertibility, and legal depth.

- Dollar Shortage Behavior: A funding squeeze can overpower ideological “de-dollarization” talk because operating systems matter more than preferences during panic.

What is the Endgame of the Dollar Milkshake Theory?

Johnson’s Dollar Milkshake Theory framework does not end with unlimited dollar strength. It suggests that confidence in sovereign bonds may eventually migrate toward harder monetary assets such as:

- Gold First: Johnson has repeatedly argued the dollar can outperform other fiat currencies while gold rises against the entire fiat complex.

- Bitcoin Second: Bankless podcast on the Crypto Milkshake summarized Johnson’s view as seeing BTC as a valid store of value, even if it is harder to use as money.

- Not Anti-Dollar by Default: The theory’s late stage is less “dollar dies tomorrow” than “trust in sovereign debt erodes and alternative stores of value gain share.”

Takeaway: At that stage, the dollar may still beat other fiat currencies, but trust can simultaneously migrate into gold, Bitcoin, and other non-sovereign stores of value. The thesis is less about dollar immortality than about hierarchy during a global sovereign debt crisis.

How Does the Dollar Milkshake Theory Impact Bitcoin?

Within Dollar Milkshake framework, Bitcoin is usually not the first winner. It can suffer during the dollar squeeze phase, then benefit later as faith in sovereign debt and fiat stewardship erodes.

Most relevant Bitcoin transmission channels:

- Dollar Liquidity Squeeze: When dollar funding tightens, global risk liquidity usually contracts first, which can pressure Bitcoin before the longer-term store-of-value bid emerges.

- Non-Sovereign Hedge: Bankless summarized Johnson’s view that BTC is a valid store of value when investors start questioning sovereign balance sheets and fiat durability.

- Volatility Sequencing: The theory implies Bitcoin may behave like a high-beta liquidity asset early in stress, then like monetary insurance later. Timing matters.

- Stablecoin Bridge Effect: Johnson’s recent Bankless discussion suggests dollar stablecoins can spread dollar usage globally while still onboarding users into crypto rails.

- Government Constraint Risk: Johnson has also warned that states can still curb blockchain usage, which limits any simplistic “Bitcoin automatically replaces money” narrative.

- Portfolio Competition With Gold: In a sovereign debt scare, Bitcoin may win some flows, but central banks and conservative allocators still tend to prefer gold first.

How Does the Dollar Milkshake Theory Impact Gold?

Gold plays a special role in the Dollar Milkshake Theory because Johnson does not see it as merely the opposite of the dollar. He has argued that the dollar can outperform other fiat currencies while gold still rises against the broader fiat system.

That view becomes more plausible in an endgame centered on sovereign debt distrust rather than simple currency competition. If governments keep issuing debt but buyers increasingly prefer harder reserve assets, gold can absorb demand from central banks, institutions, and private savers.

Dollar Milkshake Theory vs. De-dollarization

Comparing the Dollar Milkshake Theory and De-dollarization reveals contrasting views on global liquidity, structural demand, and geopolitical shifts. This analysis highlights the roles of Bitcoin, Gold, and interest rates in the future global reserve system.

Dollar Milkshake Theory Criticism

The strongest critiques do not reject dollar dominance entirely; they challenge whether Johnson’s framework overstates America’s structural advantage and understates its own balance-sheet vulnerabilities.

Main criticisms worth mentioning:

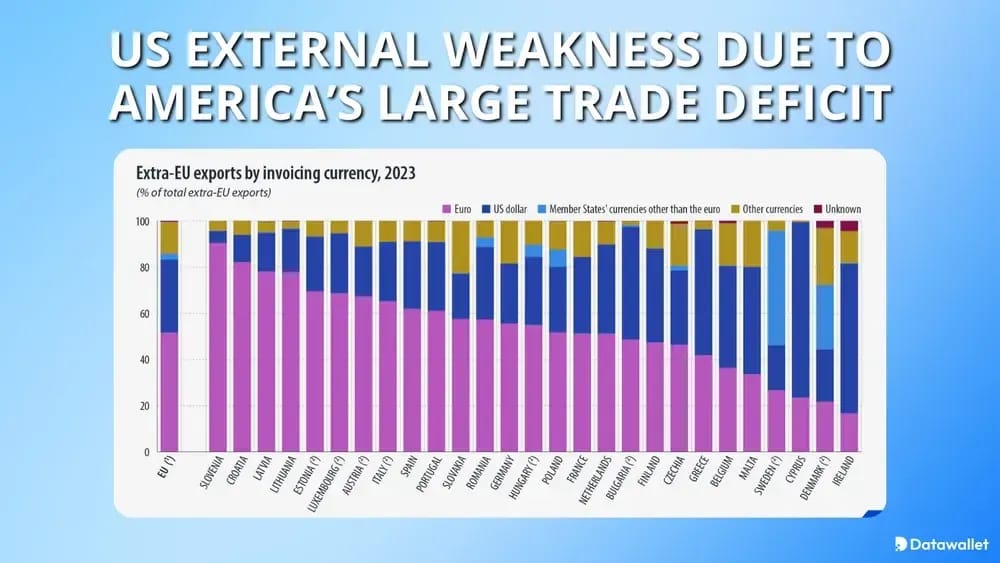

- US External Weakness: Lyn Alden has argued for a less bullish dollar view because of America’s large trade deficit and negative net international investment position.

- Funding is Broader Than a Shortage: BIS researchers noted that even after major money-market reform, non-US banks’ global dollar funding still rose, complicating a simple scarcity narrative.

- De-dollarization Momentum: Skeptics argue sanctions and geopolitics accelerate reserve diversification over time, weakening the “inevitable dollar bid” premise.

- Timing Problem: Even if the theory is directionally useful, it is not a precise model for when capital flight, sovereign stress, or asset rotation happens.

- Alternative Reserve Paths: Critics also argue the world could evolve toward a more multipolar reserve system instead of a single dramatic dollar blowoff.

- Too Market-Narrative Heavy: Mainstream economists generally view it as an investing framework, not a formally tested macro model with consensus academic support.

Who is Brent Johnson?

Brent Johnson is the founder and CEO of Santiago Capital, and his firm describes him as the originator of the Dollar Milkshake Theory. Santiago says he has roughly twenty-five years of financial-market experience across wealth management and private-client advisory work.

Before launching Santiago Capital, Johnson spent more than nine years at BakerAvenue and nine years at Credit Suisse. He is also a frequent conference speaker, appears on macro platforms including Real Vision and Blockworks, and co-hosts Markets Milkshakes and Madness with Jon Kutsmeda.

Final Thoughts

The Dollar Milkshake Theory is best understood as a crisis-sequencing framework: dollar strength first, deeper sovereign stress later, then a migration toward harder stores of value.

Its value lies in connecting dollar plumbing, debt structure, and investor behavior, but readers should treat it as a useful lens rather than settled macro consensus.