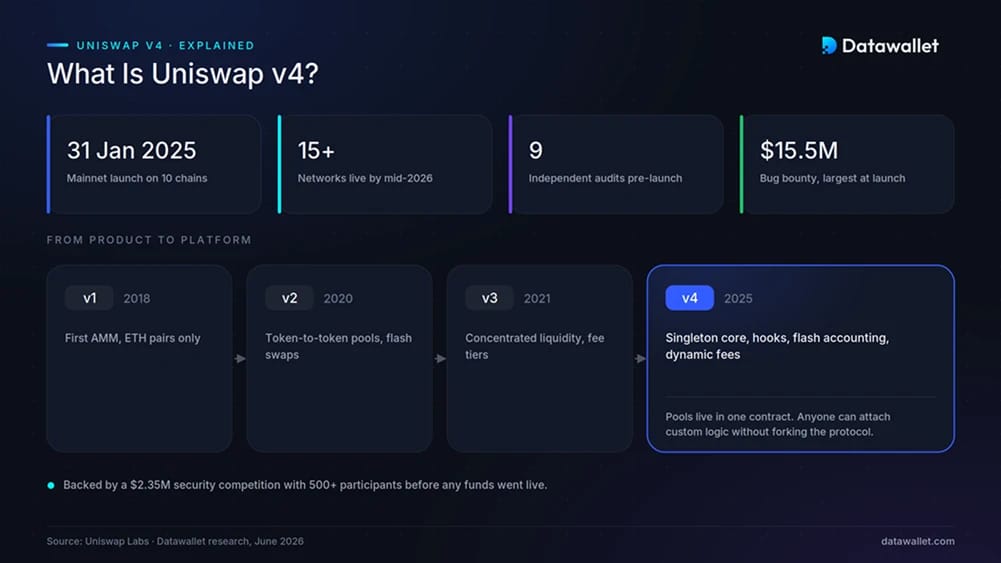

What Is Uniswap v4?

Uniswap v4 is the fourth iteration of the Uniswap protocol, deployed to Ethereum and nine other chains on 31 January 2025 after nine audits, a $2.35 million security competition, and a $15.5 million bug bounty, the largest in the industry at the time.

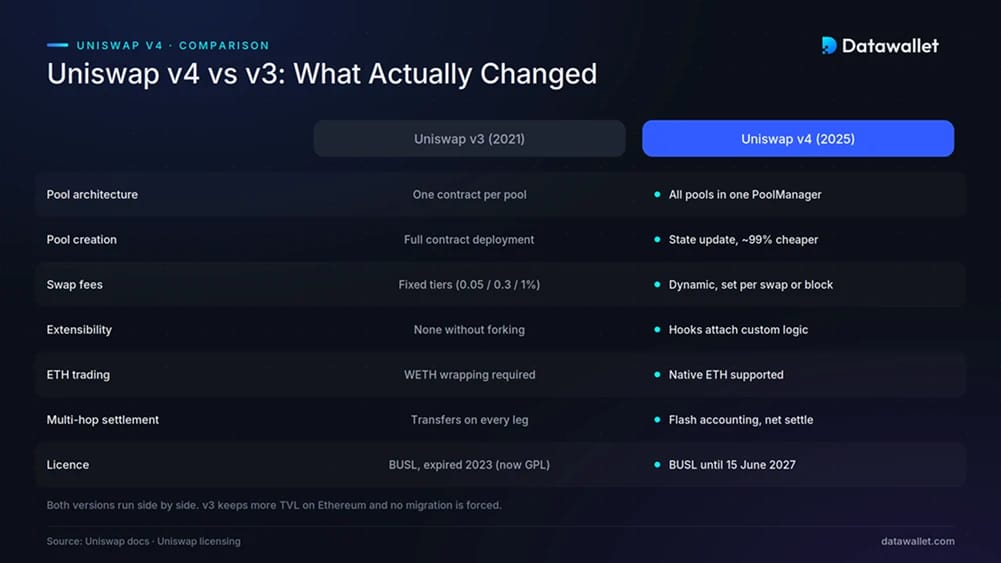

The headline change is architectural. Earlier versions deployed a separate contract for every pool, while v4 runs all pools inside one PoolManager contract and exposes lifecycle callbacks that external contracts can plug into. That design turned Uniswap from a fixed product into a platform: anyone can ship a pool with custom fee logic, MEV protection, or an entirely different pricing curve without forking the protocol.

By mid-2026 v4 is live on more than 15 networks, including Ethereum, Unichain, Base, Arbitrum, BNB Chain, Polygon, Monad, and the payments chain Tempo, and it has overtaken v3 as the default deployment target for new decentralised exchange experiments.

How Uniswap v4 Works

The v4 core whitepaper keeps the concentrated liquidity model from v3 but rebuilds everything around it. Five design choices carry most of the weight.

1. Singleton Architecture

Every v4 pool lives inside the PoolManager contract. Creating a pool is a state update rather than a contract deployment, which cuts pool creation costs by roughly 99% and makes multi-hop swaps far cheaper because tokens no longer move between separate pool contracts on each leg.

2. Flash Accounting

Flash accounting tracks balance deltas internally during a transaction and only transfers net amounts at the end, using the transient storage introduced by EIP-1153. A swap that touches four pools settles with two token transfers instead of eight, which is where much of v4's gas advantage on complex routes comes from.

3. Native ETH Support

v4 restores direct ETH trading, removing the WETH wrapping step that v2 and v3 required. Native ETH transfers are roughly half the gas cost of an ERC-20 transfer, and ETH liquidity is no longer split between ETH and WETH pools.

4. ERC-6909 Claims

The ERC-6909 standard lets users hold token balances inside the PoolManager as claims rather than withdrawing after every action. Active traders and liquidity managers can mint claims once and settle repeatedly against them, skipping repeated external transfers.

5. Dynamic Fees

Where v3 locked each pool into a fixed fee tier, v4 pools can run dynamic fees that adjust per swap or per block. Hook developers use this to charge more during volatility spikes, when toxic arbitrage does the most damage to LPs, and less in calm markets to attract volume.

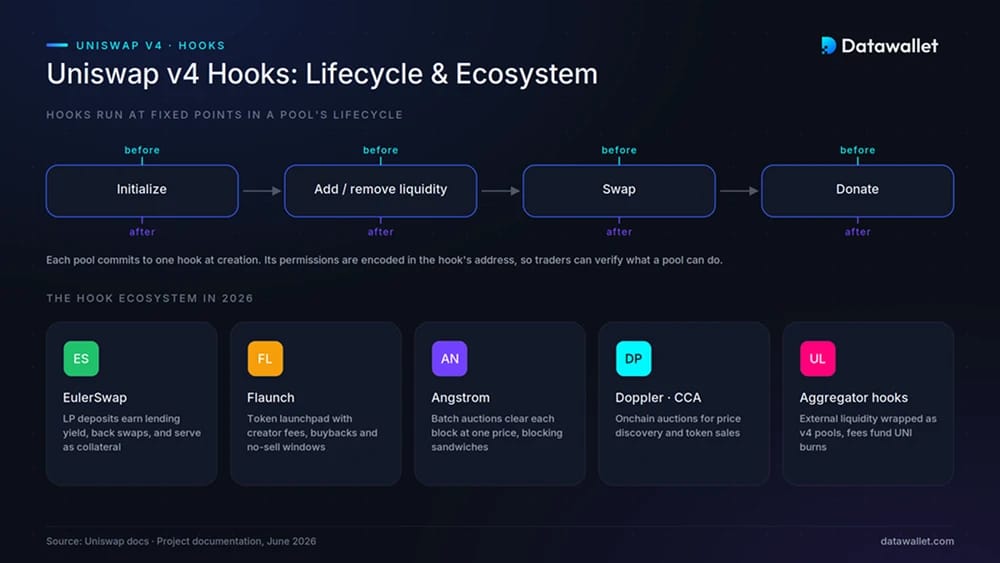

Uniswap v4 Hooks Explained

Hooks are external contracts that run at defined points in a pool's lifecycle: before or after initialisation, swaps, liquidity changes, and donations. Each pool commits to one hook at creation, and the hook's permissions are encoded in its deployment address, so traders can verify exactly what a pool can and cannot do to their swap.

In practice, hooks have become the main story of v4. The protocol itself is intentionally minimal, and the differentiation happens in the layer built on top. The most consequential hook projects we have tracked through 2025 and 2026 include:

- EulerSwap: connects v4 swap execution to Euler's lending vaults, so deposited assets simultaneously earn lending yield, back swaps, and serve as borrowing collateral. It became one of the highest-volume hooks of 2025 by making a single unit of capital do three jobs.

- Flaunch: a memecoin launchpad on Base that uses hooks to redirect trading fees to creators, run automated buybacks through a progressive bid wall, and enforce a short no-sell window at launch.

- Angstrom: built by Sorella Labs, Angstrom batches trades at a uniform clearing price each block to neutralise sandwich attacks and return arbitrage value to LPs, attacking the loss-versus-rebalancing problem that quietly drains passive liquidity.

- Doppler and Continuous Clearing Auctions: auction mechanisms built on v4 for price discovery and token launches. Privacy rollup Aztec ran its token sale through Continuous Clearing Auctions, a fully onchain alternative to centralised launch platforms.

- Aggregator hooks: built by Uniswap Labs, these source liquidity from external onchain venues through a v4 pool interface, effectively turning v4 into a DEX aggregator that collects fees on liquidity it does not own. The first one went live on Tempo in March 2026.

Thousands of hook-enabled pools have now been deployed, spanning everything from compliance-gated institutional pools to NFT games that live entirely inside a hook.

How Trades Execute on Uniswap v4

A swap on the Uniswap interface rarely touches a single v4 pool directly. The Universal Router compares prices across v2, v3, and v4 liquidity in one transaction and splits orders across versions when that improves execution, which is why v4 absorbed volume gradually rather than through a forced migration.

Larger trades increasingly settle through UniswapX, the intent-based system where users sign an order and competing fillers execute it via a Dutch auction. Fillers source from v4 pools, other DEXs, and their own inventory, and they absorb gas costs and failed-transaction risk, so the quoted price is what the user receives. The same mechanism powers cross-chain swaps on the Uniswap interface through an integration with Across.

Third-party aggregators closed the loop during 2025. 1inch, CoW Swap, Paraswap, and Matcha all index v4 pools, including hook-enabled ones their solvers can simulate safely, meaning a v4 pool with competitive pricing receives external volume regardless of which frontend the trader uses.

Uniswap v4 Adoption: The 2026 Numbers

Adoption took time. v4 launched without incentives, and most blue-chip liquidity stayed in v3 through early 2025. The curve steepened from mid-2025 as routing integrations matured and the major aggregators added v4 to their graphs.

As of June 2026, DefiLlama shows v4 has settled around $355 billion in cumulative volume, with about $190 billion on Ethereum mainnet and $70 billion on Unichain. Thirty-day volume sits near $25 billion, and LPs have earned over $260 million in cumulative swap fees.

TVL tells a more complicated story. v4 crossed $1 billion in TVL within 177 days of launch, faster than v3 managed, but currently holds around $615 million. Part of that decline traces to the shutdown of Bunni, formerly the largest LP-focused hook, covered below. v4's design also needs less idle capital per dollar of volume, since hooks like EulerSwap rehypothecate liquidity elsewhere, so TVL understates activity more than it did for earlier versions. You can compare v4 against other venues on our TVL dashboard.

Unichain: The Layer 2 Built Around v4

Unichain is Uniswap Labs' OP Stack layer 2, launched to mainnet in February 2025 as a settlement venue purpose-built for the protocol. It runs one-second blocks and, since August 2025, Flashblocks, which confirm transactions every 200 milliseconds by streaming sub-blocks built inside a trusted execution environment (TEE) co-developed with Flashbots.

The TEE matters beyond speed. Block building happens under verifiable priority ordering rules enforced in hardware, with attestations that third parties can check, and transactions that would revert are filtered out before they cost the user gas. Most rollups sequence transactions in an opaque off-chain process, so Unichain is the first L2 where ordering itself is auditable, which directly limits the sandwich-style MEV that drains traders on other chains.

Economically, Unichain became central to the UNI thesis after UNIfication, since its net sequencer revenue feeds the burn mechanism. Activity is volatile: the chain accounts for about $70 billion of v4's cumulative volume, much of it concentrated in the incentivised campaigns of 2025, and its share of daily v4 volume has since fallen well behind Ethereum and Base as those programmes ended.

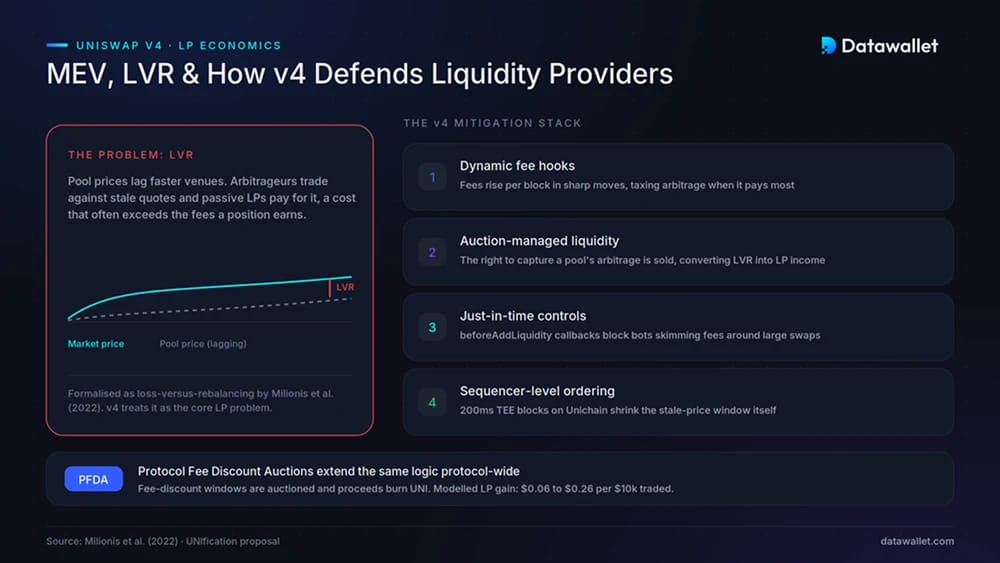

MEV and LP Economics on Uniswap v4

Passive LPs on AMMs lose money to arbitrageurs whenever pool prices lag faster venues, a cost formalised in loss-versus-rebalancing (LVR) research that often exceeds the fees a position earns. v3 gave LPs no tools against this. v4's design treats it as the core problem.

The mitigation stack now in production includes:

- Dynamic fee hooks: pools raise fees per block when prices move sharply, taxing arbitrage at exactly the moments it is most profitable, and lower them in quiet markets to stay competitive for uninformed volume.

- Auction-managed liquidity: hooks can auction the right to set a pool's fee and capture its arbitrage, converting LVR into an upfront payment to LPs. Angstrom applies the related batch-auction approach, clearing each block at one uniform price so sandwiching becomes structurally impossible.

- Just-in-time controls: v4's beforeAddLiquidity callback lets pools restrict JIT liquidity, where a bot deposits and withdraws around a single large swap to skim fees from resident LPs.

- Sequencer-level ordering: on Unichain, priority ordering inside the TEE plus 200ms blocks shrink the window in which stale prices can be picked off, reducing LVR at the infrastructure layer rather than in the pool.

PFDA, the auction mechanism approved under UNIfication, extends the same logic to the protocol level by selling temporary fee discounts and burning the proceeds, so the MEV that previously leaked to searchers and validators is split between LPs and UNI holders instead.

UNIfication and the Fee Switch

The biggest Uniswap development since the v4 launch happened in governance rather than code. On 25 December 2025, the UNIfication proposal from Uniswap Labs and the Uniswap Foundation passed with 125.3 million UNI in favour and just 742 against, ending a multi-year debate over the protocol fee switch.

The package included:

- A 100 million UNI burn from the treasury, representing roughly what would have been burned had fees been on since launch.

- Protocol fees converted into UNI burns, starting with 17% of LP fees on v2 and selected v3 pools on Ethereum from 28 December 2025, then expanding to Optimism, Arbitrum, Base, Zora, and X Layer in March 2026 and to Polygon, BNB Chain, and Celo in June 2026.

- Unichain sequencer fees directed into the same burn mechanism.

- Protocol Fee Discount Auctions (PFDA), an in-development mechanism that auctions short windows of fee-free swapping, internalising MEV that would otherwise leak to searchers. Winning bids fund further burns, and early modelling suggests LP returns improve by $0.06 to $0.26 per $10,000 traded.

- Structural consolidation: Foundation teams moved into Labs, and Labs switched off its 0.25% interface, wallet, and API fees to align entirely with the protocol.

For v4 specifically, the fee switch has not yet been flipped. The rollout deliberately started with v2 and v3 pools, and DefiLlama still records zero protocol revenue on v4 as of June 2026. Governance is extending fee coverage in stages through successive votes, and v4 pools, where dynamic fees and hooks complicate a one-size-fits-all protocol cut, are the harder design problem. PFDA and aggregator hooks are both v4-native mechanisms, so the version is central to where burn revenue is intended to come from longer term.

Uniswap v4 vs v3

v4 keeps v3's concentrated liquidity but changes how it is packaged. v3 pools are isolated contracts with fixed fee tiers and no extensibility, while v4 pools share one contract, settle through flash accounting, and can attach arbitrary hook logic.

For traders the difference shows up as cheaper multi-hop routing and, in hook-enabled pools, protections like MEV-resistant execution that v3 cannot offer. For LPs, v4 enables strategies that were previously impossible onchain, at the cost of needing to understand what each pool's hook does. v3 remains live and still holds more TVL than v4 on Ethereum, with no forced migration, so the two versions will coexist for years.

v4's code sits under a Business Source Licence until 15 June 2027, when it converts to MIT, so direct forks remain restricted until then unless governance grants an exception.

Hook Risk: The Bunni Lesson

Hooks move critical logic outside Uniswap's audited core, and 2025 delivered a hard demonstration of what that means. Bunni, then the largest LP-optimisation hook on v4, was exploited for roughly $8.4 million on 2 September 2025 through a rounding flaw in its liquidity distribution logic, despite audits from Trail of Bits and Cyfrin. Unable to fund a secure relaunch, the team shut the protocol down that October and open-sourced its contracts.

The v4 core has operated without incident since launch, and the exploit touched Bunni's own contracts rather than the PoolManager. The distinction matters for anyone using v4 in 2026: protocol risk and hook risk are separate things, and a pool is only as safe as the least-audited contract attached to it. We treat unaudited or freshly deployed hooks the way we treat unaudited protocols generally, as venues for small, loss-tolerant positions only.

Liquidity fragmentation is the second cost. The same pair can now exist across many v4 pools with different hooks, plus v3 and v2 pools, which thins liquidity per pool and pushes more execution through aggregators and UniswapX.

Final Thoughts

Uniswap v4 has done what it set out to do, which was to stop competing on features and start competing as infrastructure. The interesting products of this cycle, MEV-internalising DEXs, lending-integrated AMMs, onchain token auctions, are being built as hooks rather than as Uniswap rivals, and $355 billion in volume suggests the platform bet is paying off.

The unresolved question is economic. UNIfication finally connected protocol usage to UNI through burns, but v4 itself does not yet contribute protocol fees, and mechanisms like PFDA and aggregator hooks are still being rolled out. How governance prices a protocol cut on pools it does not fully control will define whether v4 becomes the revenue engine the December 2025 vote assumed. For background on the protocol's origins, see our guide on what Uniswap is.