Decentralized exchanges have grown from a niche workaround into core market infrastructure, and Uniswap sits at the center of that shift. It pioneered the automated market maker model that most of DeFi still runs on.

The protocol matters more in 2026 than at any point in its history. The long-dormant fee switch is live, BlackRock has routed a tokenized Treasury fund through Uniswap, and Unichain has pulled much of its trading onto a purpose-built Layer 2.

For investors and researchers, the task is separating durable fundamentals from short-term token narratives. Here is what matters before forming a view on Uniswap. 👇

What is Uniswap?

Uniswap is a decentralized exchange protocol on Ethereum that lets users trade ERC-20 tokens directly from their own wallets. Swapping on the underlying protocol needs no account, no custody handover, and no know-your-customer check.

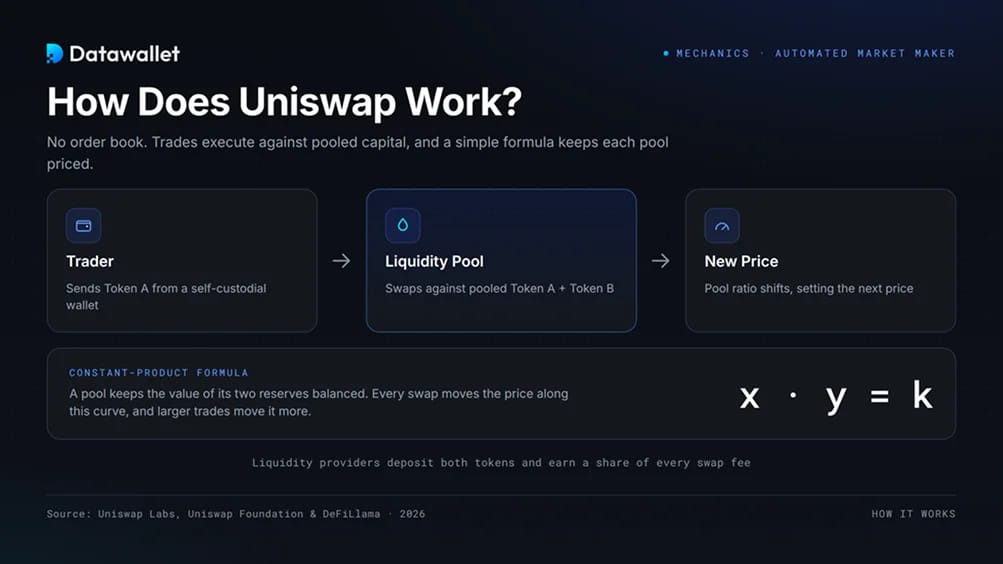

Rather than match buyers and sellers through an order book, Uniswap runs on an automated market maker (AMM). Traders swap against pooled liquidity supplied by other users, and prices adjust from the ratio of assets in each pool.

It launched in November 2018 and is now the benchmark for decentralized exchanges, with more than $3 trillion in lifetime trading volume and over 6 million wallets across its main versions.

Two parts are worth separating. The open-source protocol is a set of immutable smart contracts anyone can use or build on, while Uniswap Labs is the Brooklyn-based company behind the main app, the mobile wallet, and related products.

How Does Uniswap Work?

Uniswap replaces the order book with liquidity pools and a pricing formula, so trades execute against pooled capital instead of a waiting counterparty.

1. Liquidity Pools and the AMM

Every market is a pool holding two tokens, such as ETH and USDC. Liquidity providers deposit both assets and earn a share of trading fees, while a constant-product formula (x * y = k) sets the price and keeps the two sides balanced.

Buying ETH from an ETH/USDC pool adds USDC and removes ETH, pushing the price up along the curve. Larger trades move it more, and that price impact is what a swapper pays for taking liquidity.

2. Concentrated Liquidity

Uniswap V3 introduced concentrated liquidity in May 2021, letting providers commit capital to a chosen price range instead of spreading it evenly from zero to infinity. The same liquidity became far more capital-efficient.

Tighter ranges earn more fees per dollar deployed, but stop earning once price leaves the range. That precision, and the active management it demands, still defines how Uniswap markets are built.

3. Swapping and UniswapX

Most people use the web app or mobile wallet rather than the raw contracts. Behind the interface, a routing engine searches for best execution across pools, fee tiers, and chains.

UniswapX adds an intent-based model. Instead of sending a transaction to one pool, a user signs an order describing the result they want, and fillers compete in a Dutch auction to fill it at the best price, including across chains and from off-chain liquidity.

4. Governance and DUNI

UNI holders govern the protocol, voting on parameters, treasury spending, and major upgrades. Proposals are debated on the governance forum, then executed on-chain through a timelock once they pass.

In 2025 the community formalized its legal structure as DUNI, a Wyoming nonprofit association. That gives the DAO a recognized wrapper for contracts, tax handling, and its relationship with Uniswap Labs.

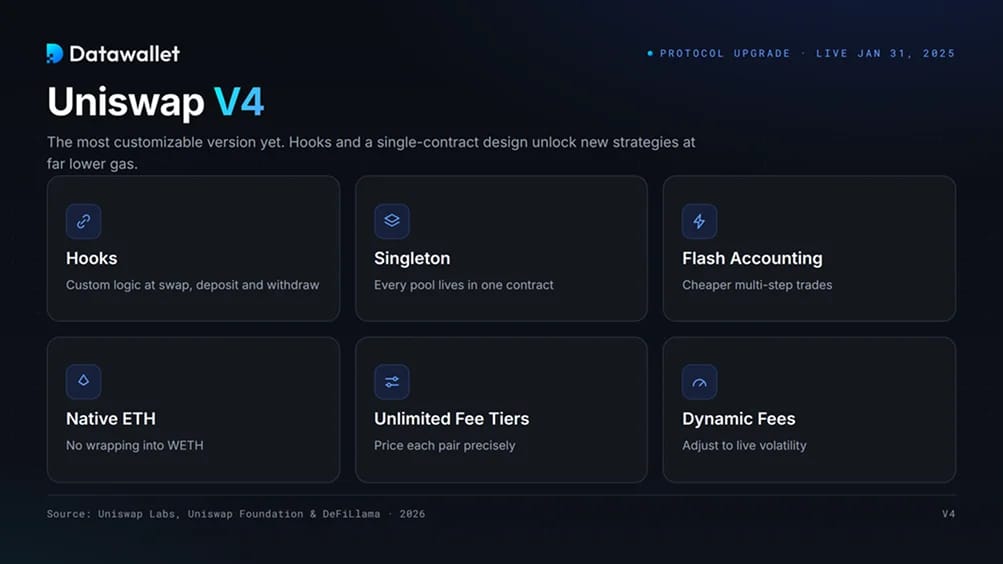

What is Uniswap V4?

Uniswap V4 launched on January 31, 2025 and is the most customizable and capital-efficient version yet. Our Uniswap V4 explainer covers it in full; the headline changes are below.

The headline feature is hooks, contracts that attach custom logic to a pool at set moments, such as before or after a swap, deposit, or withdrawal. Developers use them for on-chain limit orders, volatility-responsive fees, custom oracles, and gated pools for institutional liquidity.

V4 also moves every pool into one contract, the singleton. With a technique called flash accounting, this sharply cuts the gas cost of creating pools and running multi-step trades versus V3's separate-contract model.

Native ETH support removes the need to wrap ETH into WETH on many trades, lowering fees, and unlimited fee tiers let creators price each pair precisely. By 2026, builders had deployed thousands of hook-based pools.

What is Unichain?

Unichain is Uniswap Labs' own Ethereum Layer 2, live on mainnet since February 12, 2025. Built on the OP Stack as part of the Optimism Superchain, the team pitches it as the future home for liquidity across chains.

Unlike a general-purpose rollup, Unichain is tuned for DeFi. It ships with Uniswap V4 deployed natively at genesis, targets one-second blocks, and prices transactions about 95 percent below Ethereum mainnet, per Uniswap Labs.

Its sequencer runs in a Trusted Execution Environment built with Flashbots, making block building verifiable and curbing harmful value extraction. A UNI Validation Network gives holders a direct staking role in securing the chain.

Adoption came through incentives. A roughly $60 million DAO liquidity program pushed Unichain TVL from about $9 million to $267 million within 48 hours of its April 2025 launch, and by 2026 the chain handled close to half of all Uniswap V4 volume. Around 20 percent of its network revenue goes to Uniswap Labs.

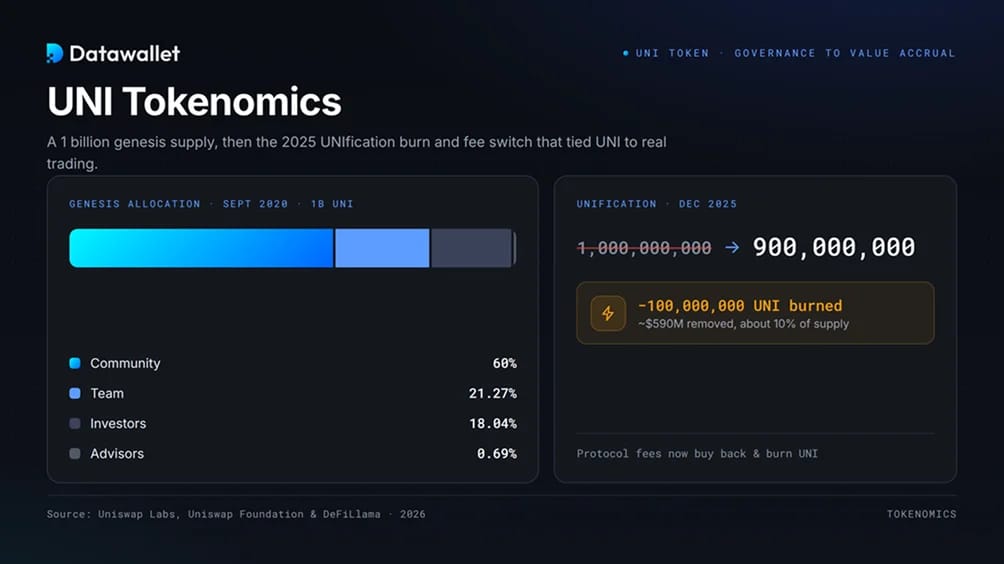

UNI Tokenomics

UNI is Uniswap's governance token, and its economics shifted more in late 2025 than in the prior five years. The original design and the new fee-driven model split into two chapters.

Token Distribution

UNI launched in September 2020 with a genesis supply of 1 billion tokens. The official allocation sent 60 percent to the community, 21.266 percent to the team and future employees, 18.044 percent to investors, and 0.69 percent to advisors, with the last three vesting over four years.

The launch is best remembered for its airdrop: anyone who used Uniswap before September 1, 2020 could claim 400 UNI, worth roughly $1,400 then and far more at later peaks. After the four-year vesting ended in 2024, a perpetual 2 percent annual inflation rate began to fund ongoing participation.

The UNIfication Fee Switch and Burn

For years, every trading fee went to liquidity providers and none to UNI holders, leaving the token with governance rights but no claim on revenue. The UNIfication proposal, introduced in November 2025, changed that.

Governance approved it on December 25, 2025 with 125,342,017 UNI for and 742 against, and execution followed on December 28 after a two-day timelock. The treasury burned 100 million UNI, about 10 percent of supply, worth more than $590 million at the time per CoinDesk. Total supply fell from 1 billion to 900 million.

It also switched on protocol fees. On V2, the LP share dropped from 0.30 to 0.25 percent, with 0.05 percent now going to the protocol. On curated V3 pools, the protocol takes 25 percent of LP fees on the lowest tiers and 16.7 percent on the highest. These fees fund continuous UNI buyback and burn, and DeFiLlama shows the mechanism reaching Optimism, Arbitrum, Base, Celo, Zora, and X Layer from March 8, 2026.

Token Utility

After UNIfication, UNI carries three roles. It is the governance token for proposals and treasury votes, it can be staked in the Unichain Validation Network, and it now accrues value through protocol-funded burns that shrink supply as trading grows.

By design, fees buy back and burn UNI rather than pay holders directly. The team framed this as benefiting holders while limiting the regulatory exposure that direct revenue sharing can attract.

Uniswap Ecosystem and Institutional Adoption

Uniswap's reach now extends well beyond retail swaps. The clearest signal came in February 2026, when BlackRock made shares of its tokenized US Treasury fund, BUIDL, tradable through UniswapX with Securitize.

It marked the world's largest asset manager's first step into DeFi. Whitelisted, pre-qualified investors can swap BUIDL against stablecoins around the clock, with Securitize handling compliance. BlackRock also disclosed a strategic investment and bought UNI, sending the token up about 25 percent.

The wider trend is tokenized real-world assets meeting on-chain liquidity. Running a regulated Treasury product through Uniswap pointed to a model where tokenized instruments use DEX rails for settlement and price discovery, not just closed institutional venues.

Uniswap Labs has also broadened its products with a self-custody mobile wallet, the acquisition of AMM and routing team Guidestar, and continued multichain deployment. The result is a protocol serving both a retail swapper on a phone and an institution moving regulated assets.

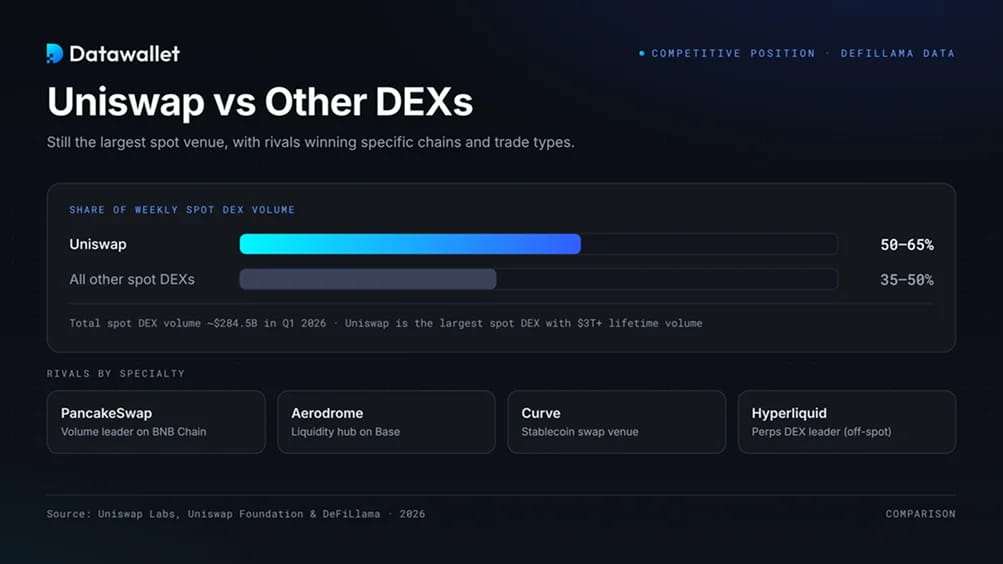

How Does Uniswap Compare to Other DEXs?

Uniswap is still the largest spot DEX by most measures, though competition has tightened. Per DeFiLlama and CoinGecko data through 2026, it ranks as a top venue across Ethereum, Base, Arbitrum, Optimism, and Polygon.

Trackers put its combined share of weekly DEX volume in a wide band, often 50 to 65 percent depending on conditions and memecoin spikes on rival chains. Total spot DEX volume hit about $284.5 billion in Q1 2026, down from Q4 as memecoin trading cooled.

Rivals split by specialty. PancakeSwap leads on BNB Chain and set monthly records in 2025, Aerodrome anchors liquidity on Base, and Curve stays the venue of choice for stablecoin swaps. Newer names like Fluid have taken share in specific windows.

Perpetual futures sit in a separate category. Hyperliquid became the dominant on-chain perps venue in 2025 and 2026, an area Uniswap does not serve directly. For that side, see our guide to decentralized perpetuals exchanges.

Uniswap Founders and History

Uniswap was created by Hayden Adams, a Stony Brook mechanical engineer who taught himself Solidity after Siemens laid him off in 2017. He built the first version after reading Vitalik Buterin's post on on-chain automated market makers, and Uniswap V1 went live in November 2018.

The protocol then iterated fast. V2 arrived in May 2020 with direct ERC-20 to ERC-20 pairs and flash swaps, V3 brought concentrated liquidity in May 2021, and V4 introduced hooks and the singleton design in January 2025.

On funding, Uniswap Labs raised an $11 million Series A in 2020 from a16z, Paradigm, and Union Square Ventures, a larger round in 2022, and the 2026 strategic investment from BlackRock. That roster ties Uniswap to crypto's most active investors.

A major overhang lifted in February 2025, when the SEC closed its investigation into Uniswap Labs with no enforcement action, after a Wells notice the year before. That removed a key regulatory risk and cleared the path for UNIfication.

Risks of Using Uniswap

Uniswap is battle-tested infrastructure, but using it still carries real trade-offs around execution, smart contracts, token economics, and the wider market. Investors should separate the protocol's strength from UNI as a speculative asset.

Key risks to consider include:

- Impermanent Loss: Providers can end up worse off than simply holding the two tokens when prices diverge, especially in volatile pairs. Concentrated liquidity in V3 and V4 amplifies this once price leaves a chosen range.

- MEV and Sandwich Attacks: Because trades sit in the public mempool, bots can front-run and back-run swaps. Retail trades on Ethereum mainnet get sandwiched routinely unless protected by UniswapX or private order routing.

- Smart Contract Risk: Uniswap runs on smart contracts, and V4 hooks let third parties add custom logic. A malicious or buggy hook, a faulty pool, or a bad token approval can risk funds even when the core protocol works.

- Scam and Fake Tokens: Anyone can create a pool for any token, so fraudulent and honeypot assets appear constantly. Buying an unverified token can mean total loss, and users must confirm contract addresses themselves.

- Fee Switch Trade-Offs: UNIfication redirects part of LP fees to the protocol, trimming what providers earn. If that pushes liquidity to rivals, it could pressure the volume now backing the UNI burn.

- Token Volatility: UNI now depends partly on trading activity through the burn, but it still trades with high volatility and broad crypto sentiment, moving sharply regardless of fundamentals.

- Competitive Pressure: PancakeSwap, Aerodrome, Curve, and chain-native DEXs compete hard for liquidity and volume, while perps venues like Hyperliquid capture activity Uniswap does not serve.

- Regulatory Uncertainty: The SEC closed its case, but rules on DeFi, tokenized assets, and value-accruing tokens stay unsettled across jurisdictions and could reshape how Uniswap and UNI operate.

- Layer 2 Dependence: Much activity now sits on Layer 2 networks and Unichain, which carry their own sequencer, bridging, and early-stage decentralization risks separate from Ethereum mainnet.

Final Thoughts

Uniswap has grown from a single-product DEX into a multichain protocol with its own Layer 2, an intent-based trading system, and institutional partners. Its core AMM design still underpins much of decentralized trading.

The 2026 story is value alignment. With the fee switch live and UNI burns tied to real volume, the token finally has a claim on protocol activity, and BlackRock's involvement shows regulated capital will use those rails.

Plenty still has to prove out. Lower LP rewards, hard competition, MEV exposure, and unsettled regulation remain open questions, so Uniswap reads as mature infrastructure carrying real execution and market risk, not a one-way bet.

.webp)