What is DYDX? Tokenomics, Fees & V4 Explained

Summary: dYdX is a decentralized Layer 1 blockchain optimized for perpetual derivatives trading, offering 182+ markets with up to 100× leverage. Built on Cosmos SDK with proof-of-stake, it delivers scalability, low latency, and governance-driven updates.

Despite rising competition from protocols like Hyperliquid, new features like MegaVault liquidity and community governance keep it a major player in DeFi and onchain perpetuals.

dYdX Overview

dYdX, founded by Antonio Juliano, is a Layer 1 blockchain designed for perpetual derivatives trading, supporting 182+ markets with $300M in daily volumes.

Available Assets

BTC, ETH, SOL & 180 more

Fees

0.050% Taker and 0.020% Maker Fee

Architecture

Cosmos-Based Layer 1 Blockchain

What is dYdX?

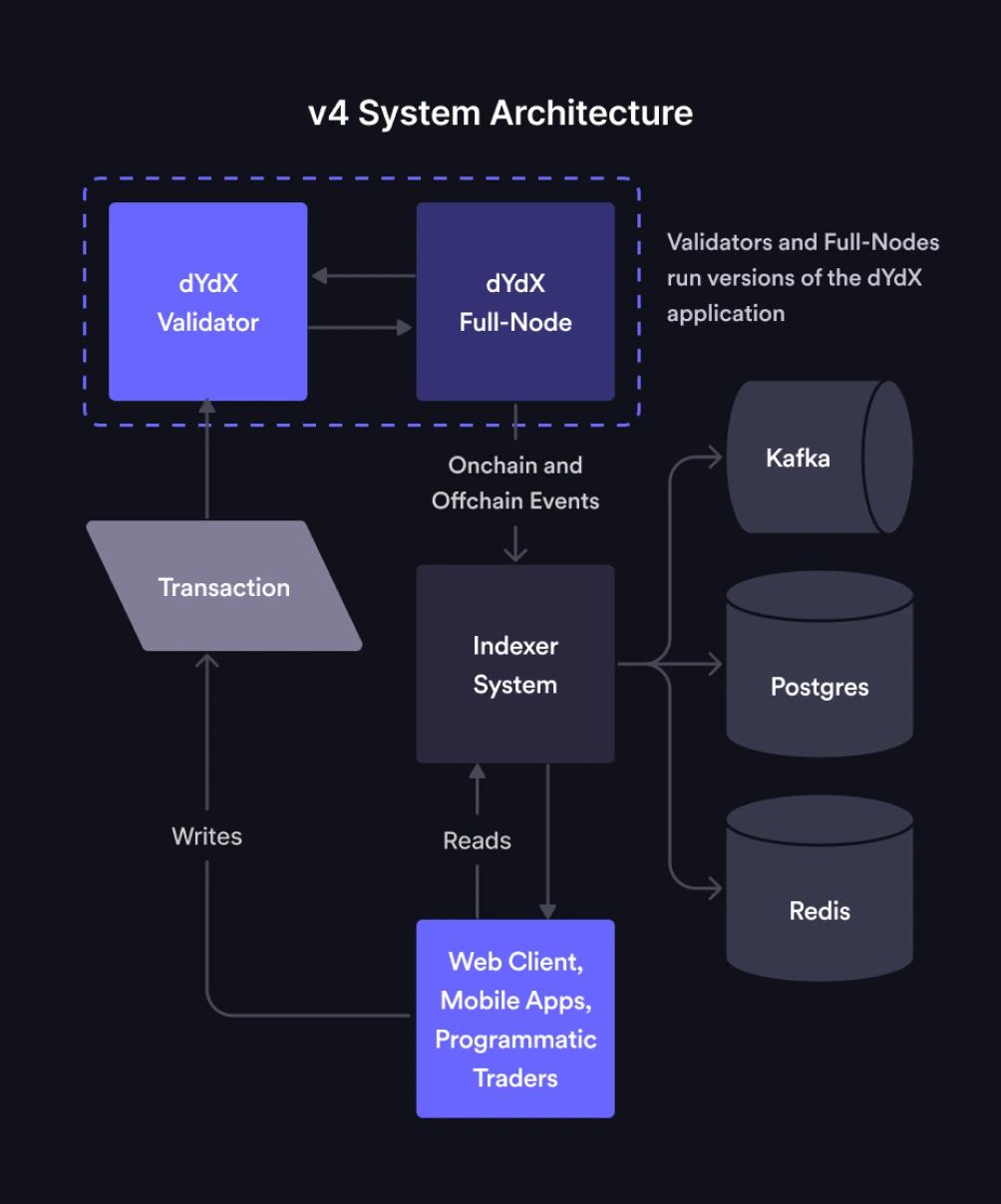

dYdX is a decentralized blockchain designed to support perpetual derivatives trading. Built on the Cosmos SDK and CometBFT consensus, it operates as a standalone Layer 1 blockchain with a decentralized order-book and matching engine. This architecture ensures high scalability, low latency, and complete transparency for traders.

The protocol employs proof-of-stake (PoS), where validators finalize blocks, and stakers secure the network. Rewards, paid in USDC and the native governance token, are drawn from trading and gas fees. Efficient data access is enabled through open-source indexers optimized for real-time use.

dYdX supports configurable margining, deterministic trading rewards, and governance-driven updates, providing a performant, trustless infrastructure for derivatives markets.

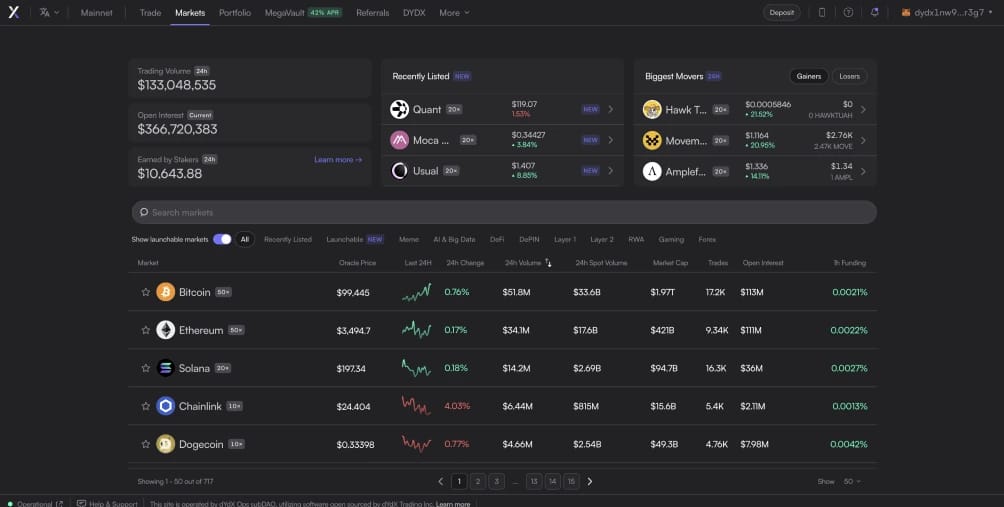

dYdX Supported Markets

dYdX hosts over 182 markets, enabling trading of cryptocurrency derivatives contracts with up to 100× leverage. Popular pairs such as BTC-USD, ETH-USD, SOL-USD, and DOGE-USD drive significant activity, contributing to an average daily trading volume of $300 million.

In addition to major pairs, dYdX regularly lists new tokens based on demand, including assets like TAO, GOAT, TIA, ZRO, and even Fartcoin. This approach ensures traders can access established markets and emerging opportunities across various sectors.

dYdX Trading Fees

dYdX uses a straightforward fee structure with maker rebates and volume-based discounts to incentivize trading. Fees differ for makers and takers, with reduced costs for high-volume traders across all markets.

- Maker Fees: -1.1 bps (rebate), rewarding liquidity providers.

- Taker Fees: Start at 3 bps, scaling lower with higher 30-day trading volumes.

- Volume Discounts: Apply progressively based on combined 30-day trading volume across sub-accounts.

- Flat Structure: Fees are uniform across all markets for simplicity.

- Governance Control: Fees can be adjusted by the dYdX governance community as needed.

dYdX V4 Explained

In April 2024, dYdX migrated from Ethereum-based smart contracts (V3) to its own Layer 1 blockchain using the Cosmos SDK (V4). This shift allowed dYdX to control its full tech stack, optimizing performance specifically for derivatives trading without reliance on external settlement layers like StarkEx.

V4 also introduced a decentralized off-chain order book maintained by validators for low-latency matching, paired with on-chain settlement. This replaced V3’s Layer 2 architecture, delivering greater efficiency. Proof-of-stake (PoS) consensus was also implemented, with validators finalizing blocks and earning rewards from trading and gas fees.

Governance expanded in V4, giving the community direct control over upgrades, fees, and rewards, replacing the slower DAO model in V3.

dYdX Staking and Rewards

dYdX’s staking and rewards system, governed by the community, secures the network and incentivizes participation through rewards tied to trading and gas fees. Validators, stakers, and traders benefit from mechanisms designed to align activity with protocol growth.

Staking Rewards

Validators and delegators earn staking rewards funded by trading and gas fees. Rewards are calculated and distributed every block but require manual claiming by participants.

- Reward Formula: (Fee Pool * (Delegator's Stake / Total Stake)) * (1 - Community Tax) * (1 - Validator Commission) according to the rewards documentation.

- Sources: Trading fees (USDC) and gas fees (USDC and NATIVE_TOKEN).

- Manual Claims: Rewards accumulate in the distribution module until claimed by stakers.

Trading Rewards

Traders receive automatic rewards for each trade, proportional to the fees they generate. These rewards are capped to align with the protocol’s treasury and governance decisions.

- Reward Formula: Rewards are proportional to a trader’s fees relative to all fees in the block.

- Emission Limits: Rewards per block are capped to control inflation.

- Automatic Distribution: Rewards are distributed directly to traders’ accounts after each block.

dYdX Tokenomics

The $DYDX token, launched in 2021 by the dYdX Foundation, is central to the protocol’s governance, rewards, and staking systems. Its structure is designed to incentivize use, support development, and decentralize decision-making. Key aspects of the design include:

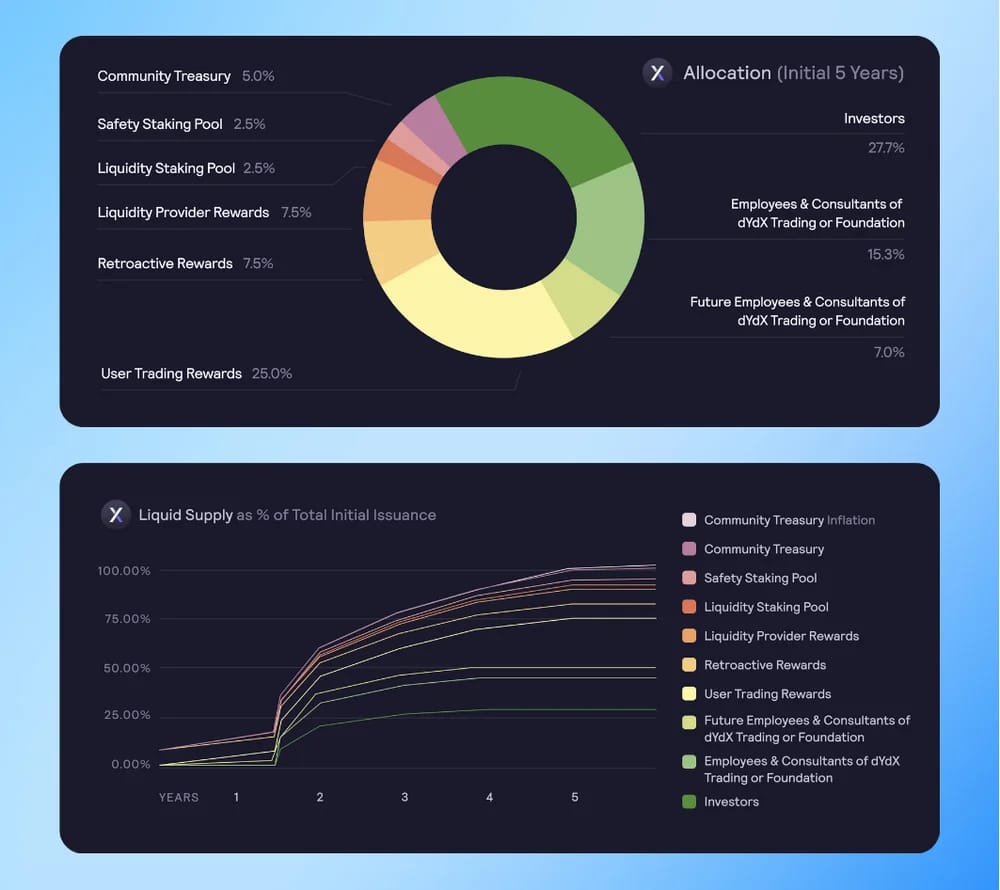

- Total Supply: 1 billion $DYDX tokens, distributed over five years from August 2021 to August 2026.

- Community Allocation: 50% (500 million $DYDX) is allocated for trading rewards (14.5%), retroactive mining rewards for past users (5%), liquidity provider rewards (5.2%), the Community and Rewards Treasuries (24.2%), USDC liquidity staking (0.6%), and safety staking (0.5%).

- Investor and Employee Allocation: The remaining 50% supports platform development through distributions to investors and team members.

- Inflation Policy: Starting in 2026, the protocol may introduce an inflation rate of up to 2% annually for ongoing development, subject to governance approval.

- Governance Control: $DYDX holders manage all major protocol decisions, including market additions, parameter adjustments, and token functionality.

- Validator Staking: With V4, $DYDX holders can stake to secure the network and participate in consensus.

- Utility for Discounts and Staking: The token continues to provide fee discounts and now supports validator staking, further decentralizing the network.

What is dYdX Unlimited?

dYdX Unlimited introduces instant market creation with liquidity powered by MegaVault. Users can launch leveraged markets for any asset, including cryptocurrencies and prediction markets, with up to 20x leverage.

MegaVault acts as a global liquidity pool, automating market making and offering depositors a share of profits with up to 40% APY. This upgrade simplifies decentralized trading, making it faster and more accessible.

Who Founded dYdX?

dYdX was founded in 2017 by Antonio Juliano, a Princeton-educated software engineer with prior experience at Coinbase and Uber. Under Juliano’s leadership, dYdX became one of the most recognized decentralized derivatives exchanges, achieving $1 trillion in trading volume.

In May 2024, Juliano announced his resignation as CEO after seven years of building the platform. However, he returned later that year, taking "founder mode" to reshape dYdX amidst rising competition from platforms like Hyperliquid, which has taken the majority of market share in perps volumes.

Bottom Line

dYdX has established itself as a key player in decentralized derivatives trading, with innovations like its Layer 1 blockchain, MegaVault liquidity system, and community-driven governance.

However, with competitors like Hyperliquid now trading $3 billion daily, 10x dYdX’s volume, the platform faces significant pressure to adapt and scale.

As dYdX continues to evolve, its ability to innovate and recapture market share will determine its position in the fast-moving DeFi landscape.