What are Liquid Staking Derivatives?

A liquid staking derivative is a token a protocol mints when you deposit assets into its staking service. It represents your claim on the pooled stake plus accruing rewards, and you can hold, sell, lend, or use it as collateral while the underlying tokens stay locked in the consensus layer.

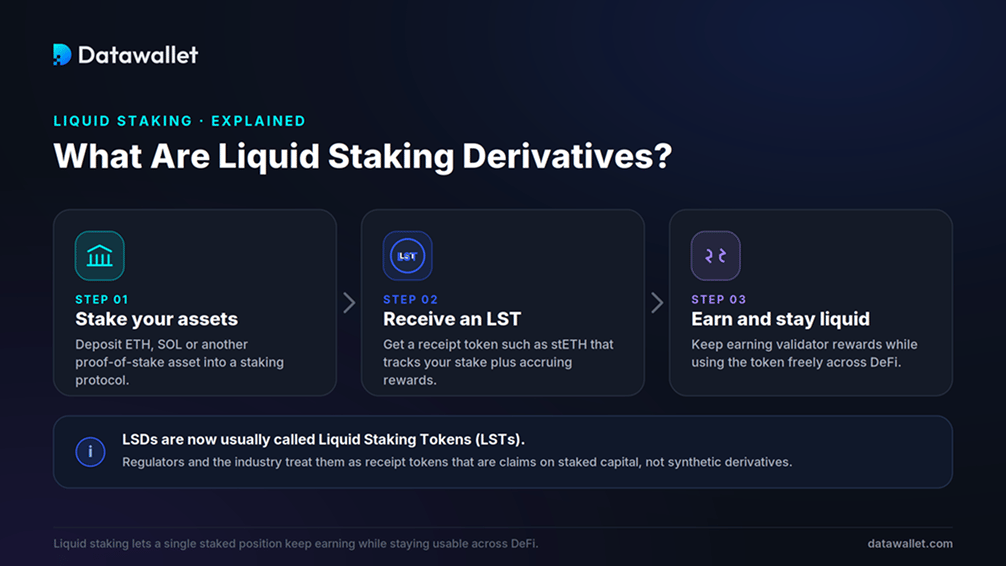

The "derivative" label is a holdover. Industry bodies and US regulators now prefer "liquid staking token" or "staking receipt token," since these assets are direct claims on staked capital rather than synthetic instruments that track a price. We use LSD and LST interchangeably here, with LST being the more accurate term.

They exist because native staking forces a tradeoff. Running an Ethereum validator requires 32 ETH locked in the consensus layer, where it sits idle beyond a base yield. Liquid staking removes that lockup with a liquid receipt, so the same capital secures the network and works elsewhere at once.

The model took off after Ethereum moved to proof-of-stake at the Merge in September 2022, and accelerated once the Shapella upgrade enabled staking withdrawals in April 2023. With withdrawals live, LSTs could be redeemed for the underlying asset, which anchored their value.

How Do Liquid Staking Derivatives Work?

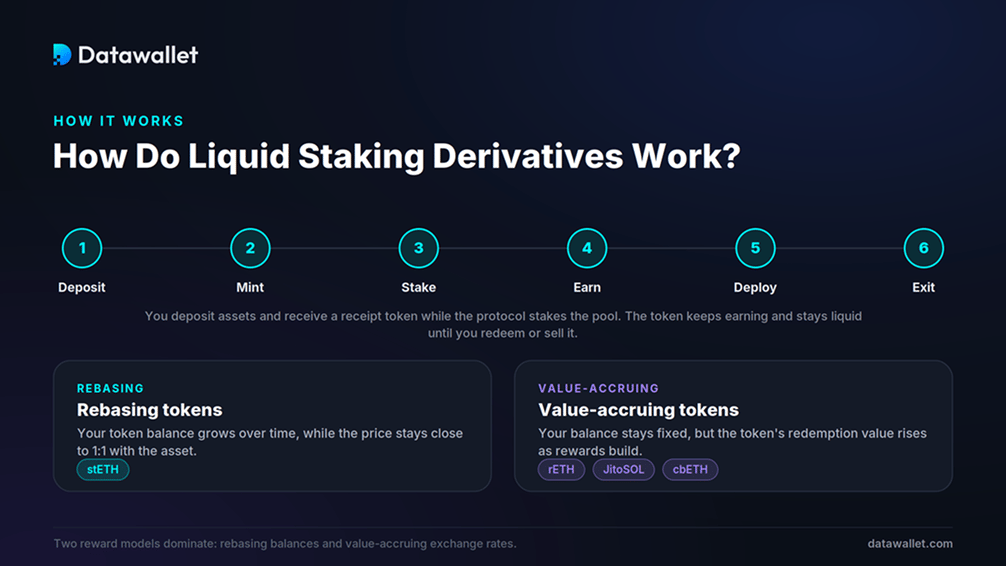

A liquid staking protocol sits between you and the validators. It pools deposits, delegates to node operators, and issues a token that tracks your position. The mechanics vary by protocol, but the lifecycle is consistent.

1. Deposit, Pooling, and Minting

When you deposit ETH, SOL, or another supported asset, the protocol pools it and mints a matching amount of its staking token to your wallet. The deposit is then staked across a validator set, so you skip the minimum balance and the work of running a node.

The core lifecycle works like this:

- Deposit: Send an asset like ETH or SOL into the protocol's smart contract through its app or a connected wallet.

- Mint: The protocol issues a receipt token (stETH, rETH, JitoSOL) recording your share of the pool and any rewards owed.

- Stake: Pooled funds are delegated to node operators that validate transactions and earn consensus rewards.

- Earn: Your token reflects accruing rewards automatically, with no claiming and no validator to maintain.

- Deploy: Move that token into lending markets, liquidity pools, or other strategies while the deposit stays staked.

- Exit: Redeem through the protocol's withdrawal queue, or sell on the secondary market for an instant exit.

2. How Staking Rewards Accrue

How an LST reflects rewards matters for accounting, taxes, and DeFi integrations. Two designs dominate.

- Rebasing tokens: Your balance grows daily to reflect rewards while holding a roughly 1:1 value with the underlying asset. Lido's stETH works this way, and most holders wrap it into non-rebasing wstETH for DeFi protocols that expect a fixed balance.

- Value-accruing tokens: Your balance stays fixed, but the token's redemption value rises as rewards build. Rocket Pool's rETH, Coinbase's cbETH, Frax's sfrxETH, and Jito's JitoSOL use this design, so one token slowly redeems for more than one unit of the base asset.

Protocols take a cut of rewards as a fee. Lido charges 10%, split between node operators and its DAO treasury, while Rocket Pool charges more in exchange for a more decentralized operator set.

3. Redemption, Withdrawals, and the Peg

An LST holds its value through redeemability and arbitrage. Because you can redeem the token for the underlying asset through the withdrawal queue, traders buy it whenever it trades below fair value and redeem for a profit, pulling the price back toward peg.

Timing is the catch. Exit queues are not instant, and Ethereum processes only so many validator withdrawals at once, so redemptions can take days during heavy outflow. Anyone needing immediate liquidity sells on a decentralized exchange, where deep pools usually keep prices tight but can widen under stress.

Top Liquid Staking Protocols

Liquid staking is the largest single category in DeFi. A handful of protocols hold most of the value, split across Ethereum and Solana.

- Lido (stETH): Ethereum's leader, holding close to half the sector with more than $20 billion staked. stETH is the most widely integrated LST, accepted as collateral across major lending and liquidity venues. Our Lido explainer covers the protocol in depth.

- Rocket Pool (rETH): The decentralization-first Ethereum option, built on a permissionless node operator network. It trades some liquidity depth for stronger censorship resistance.

- Binance Staked ETH (WBETH): One of the largest ETH staking tokens by value, issued through Binance and used across its ecosystem and supported DeFi venues.

- Jito (JitoSOL): Solana's leading LST, with billions in SOL staked. Jito captures maximal extractable value from transaction ordering and returns it to stakers, lifting its yield above standard Solana staking. See our Jito and JitoSOL guide.

- Marinade and Sanctum (Solana): Marinade's mSOL was an early Solana standard, while Sanctum powers a wide range of Solana LSTs, widening validator and token choice.

- ether.fi (eETH and weETH): The largest liquid restaking protocol, pairing base staking with EigenLayer restaking in one token. See our ether.fi guide.

Other established options include Coinbase's cbETH, Mantle's mETH, Frax's sfrxETH, StakeWise, and Liquid Collective's LsETH. For a current ranking, see our best liquid staking platforms.

Top Use Cases for Liquid Staking Derivatives

An LST's value is that one position does several jobs at once. Holders combine validator rewards with DeFi activity to raise the return on the same capital.

- Collateral: Tokens like wstETH are accepted on lending protocols, letting holders borrow against a staked position without unstaking.

- Lending: Supplying LSTs to money markets earns interest on top of the staking yield, layering two income streams.

- Liquidity provision: LST and underlying-asset pairs on decentralized exchanges earn trading fees, since the two assets track closely and limit impermanent loss.

- Restaking: LSTs can be restaked through EigenLayer to secure extra services and earn a second reward layer.

- Leverage looping: Some users borrow against an LST, buy more, and repeat to amplify exposure, a high-risk tactic covered in our looping strategy guide.

- Treasury management: Funds and treasuries hold LSTs to keep yield on idle assets while staying able to move quickly.

Liquid Staking vs Restaking

Liquid staking and restaking sit at different layers. Liquid staking unlocks the liquidity of one staked position. Restaking reuses that staked capital to secure extra protocols, adding both yield and risk.

In a restaking model, you commit staked ETH or an LST to a network like EigenLayer, where it backs Actively Validated Services such as oracles, bridges, and data availability layers. Each service sets its own slashing conditions and pays its own rewards, so your collateral answers to more than one set of rules.

Most users access this through liquid restaking tokens (LRTs). You deposit ETH or an LST into a protocol like ether.fi, Renzo, or Kelp and receive a token (eETH, ezETH, rsETH) that stays usable in DeFi. EigenLayer dominates this market by a wide margin.

The tradeoff is direct. Restaking can lift a typical 3% to 4% Ethereum yield by another one to two points from service rewards, but it stacks smart contract risk and exposes the same capital to multiple slashing conditions. Yield-loop strategies promising far higher returns rely on borrowing and recursion, which can unwind fast in a sharp move.

Liquid Staking Trends and Statistics

A few figures show how central staking has become to both Ethereum and DeFi, and where liquid staking sits in 2026.

- Sector size: Liquid staking is DeFi's largest category, with DefiLlama tracking value above $40 billion in mid-2026 after a peak near $86 billion in August 2025. The total moves with crypto prices.

- Ethereum participation: Around 30% of all ETH, roughly 36 million coins, is now staked, with native yields near 3%, per our Ethereum staking statistics.

- Lido dominance: Lido holds close to half of all liquid staking value and roughly a quarter of staked ETH, a concentration that keeps the decentralization debate alive.

- Restaking growth: EigenLayer secures well over $10 billion in restaked ETH and controls most of the restaking market, the fastest-growing slice of the sector.

- Solana yields: Solana LSTs like JitoSOL often pay 6% to 8%, above Ethereum equivalents, helped by MEV rewards. See our Solana staking statistics.

- Institutional inflows: Staking-enabled funds drove roughly a third of Ethereum ETF inflows in 2026, pushing validator entry queues to multi-year highs.

Pros and Cons of Liquid Staking Derivatives

Liquid staking derivatives improve capital efficiency and lower the barrier to staking, but they add risks that native staking avoids. The table weighs the main tradeoffs.

Are Liquid Staking Derivatives Safe?

Liquid staking is one of DeFi's more battle-tested areas, and the largest protocols have years of audits and bug bounties behind them. That track record reduces risk without removing it, since an LST stacks several distinct exposures worth evaluating separately.

The clearest warning came in June 2022, when stETH fell to about 0.94 ETH and briefly lower. Withdrawals were not yet live, so the token could not be redeemed for ETH. As the Terra collapse spread and lenders like Celsius and Three Arrows Capital dumped stETH into thin liquidity, the price slid below peg, as Nansen documented. It recovered once Shapella enabled redemptions in 2023.

Risks of Using Liquid Staking Derivatives

Before treating an LST as a safe, fully liquid version of the underlying asset, holders should weigh the main risk categories.

- Smart Contract Risk: LST and restaking contracts can contain bugs, and audits reduce but do not remove exploit risk. Our smart contract auditing overview explains how this is assessed.

- Slashing Risk: Validators that go offline or break consensus rules face penalties that cut the value backing the token.

- Depeg Risk: An LST can drift from the underlying during heavy selling, hurting forced sellers and triggering liquidation cascades for leveraged holders.

- Liquidity and Exit Risk: Withdrawal queues are not instant, and Ethereum limits daily validator exits, so secondary-market prices can widen sharply in a rush for the exits.

- Centralization Risk: Lido alone holds roughly a quarter of staked ETH, and concentration at that scale raises questions about validator influence and governance.

- Restaking and Looping Risk: Restaking exposes the same collateral to multiple slashing conditions, while looped positions can be liquidated quickly when markets turn.

The Future of Liquid Staking

The biggest recent shift is regulatory. In August 2025, the SEC's Division of Corporation Finance stated that liquid staking does not involve the offer or sale of securities. The SEC and CFTC then codified that view in a joint interpretation on March 17, 2026, confirming that liquid staking is not a securities transaction and that staking receipt tokens are not securities. That removed a barrier that had kept many US institutions on the sidelines.

Products followed the rules. The first US Ethereum staking ETF launched in late 2025, Grayscale's ETHE began passing staking rewards to shareholders in January 2026, and BlackRock listed its staked Ethereum fund in March 2026. Solana staking ETFs from Bitwise and VanEck arrived around the same time. You can track flows on our Ethereum ETF tracker.

Infrastructure matured alongside. Lido's V3 upgrade introduced stVaults, a modular framework that lets institutions and builders run custom staking setups while tapping stETH liquidity. The Pectra upgrade raised the validator balance cap to 2,048 ETH through EIP-7251 and streamlined withdrawals, easing operations for large stakers.

Final Thoughts

Liquid staking derivatives solved proof-of-stake's original problem: the choice between earning yield and keeping capital usable. By issuing a tradable receipt for a staked position, they turned idle collateral into active capital and now underpin a large share of DeFi.

The category has also grown more layered. Restaking, leverage looping, and multichain LSTs can raise returns, but each adds risk a simple staked position avoids. The 2022 stETH episode shows that liquidity and the peg hold in calm markets and can break under stress.

For most users, the real questions are protocol security, liquidity depth, and how much complexity they want. With regulation clearer and institutional products live, liquid staking looks set to stay a core part of the on-chain economy, as long as holders treat each layer of yield as its own decision.