Can I Buy Bitcoin with Sparkasse Bank?

Not directly in the Sparkasse app today. Sparkassen has said it plans to add in app crypto trading through DekaBank by summer 2026.

If you want BTC now, I treat Sparkasse as the funding rail. Send EUR from your Sparkasse Girokonto to a regulated exchange in Germany, then buy Bitcoin there. For speed and fewer payment issues, I stick to SEPA Überweisung and, when it is available, select Echtzeit Überweisung (Instant Payments) in Online Banking or the Sparkasse app.

I only use Sparkasse Visa or Mastercard deposits as a backup because cards tend to add fees and more declines than a bank transfer. Once your euros arrive, buy on an exchange authorised under the EU’s MiCA regime and aligned with BaFin-supervised crypto services in Germany.

How to Buy Crypto with Sparkasse Bank

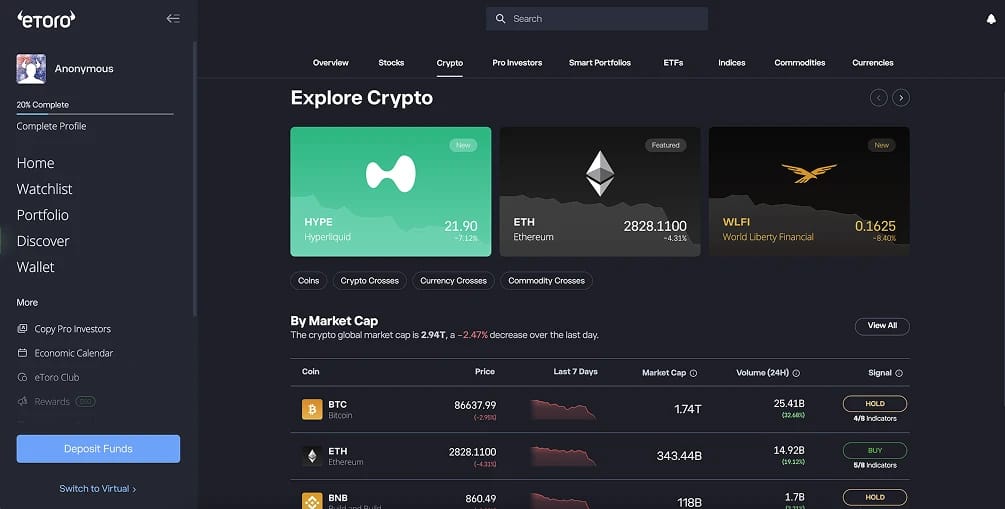

Sparkasse customers can buy crypto by sending euros to a regulated platform, and in our tests eToro is the simplest route for most German users. You trade inside eToro through eToro (Europe) Ltd, which holds a MiCA permit from CySEC that covers regulated crypto services across the EEA.

I recommend eToro because it keeps everything in one account (crypto plus stocks and ETFs) and pricing is clean: 1% to buy and 1% to sell crypto. The tradeoff is cost, so I use it for longer-term positions, not frequent in-and-out trades.

Step-by-step guide to buying crypto with Sparkasse on eToro:

- Open an eToro account: I register, then complete the identity and crypto access checks for Germany.

- Deposit euros from Sparkasse (SEPA transfer): In the Sparkasse app, I use Überweisung, paste the eToro EUR IBAN from the deposit screen, and copy the reference exactly.

- Choose your cryptocurrency: I search Bitcoin or Ethereum, open the asset page, and check the order ticket before I commit.

- Execute the trade: I enter the amount, place the order, and eToro executes the buy. Your crypto is then held under the Germany custody setup (the part that matters after you fund from a bank transfer).

Fees and Deposit Limits for Sparkasse Bank Customers

I check costs before funding eToro from Sparkasse for two reasons: FX conversion can inflate the bill, and daily transfer limits can block a deposit.

- Bank Transfers: SEPA Überweisung from Sparkasse is usually the lowest-cost rail, but pricing depends on your local Sparkasse and account plan. Echtzeitüberweisung (SEPA Instant) can be free or charged, again plan dependent.

- Card Deposits: I avoid card deposits when possible because conversion fees can apply if the deposit settles outside EUR, so I keep funding and balances in EUR.

- Withdrawals: eToro charges a flat $5 USD withdrawal fee for withdrawals from a USD investment account to an external bank account. I batch withdrawals so that fee does not hit small amounts.

- Limits: Sparkasse online transfer limits vary, and failed transfers often come down to hitting the daily cap. In Sparkasse Online Banking, adjust it under Einstellungen > Konten, Karten, Finanzprodukte > Girokonto > Online-Überweisungslimit pro Tag, then confirm with pushTAN. On eToro, unverified accounts are limited to $2,250 total deposits, so I verify early if I plan to fund size.

- Trading: eToro charges 1% to buy and 1% to sell crypto. I treat that as a longer-hold setup, not frequent trading.

Routing Sparkasse deposits through SEPA in EUR keeps costs cleaner than card funding, where conversion and processing fees stack fast.

Sparkasse Bank Cryptocurrency Policy

Sparkasse still does not sell Bitcoin or other coins directly in the Sparkasse app today, but it has already signposted that customers should be able to trade crypto in app from 2026, using DekaBank products inside the Sparkassen group.

In practice, I treat Sparkasse as a funding bank, not a crypto broker. SEPA transfers to established EU platforms usually go through, but Sparkasse risk checks can pause first-time recipients, unusual amounts, or transfers that look like they are heading to lightly supervised venues. That scrutiny aligns with how German AML expectations apply to crypto services.

What I recommend: treat Sparkasse as the rail, then use an exchange with a clear EU authorisation track under MiCA and services supervised in Germany. If a transfer gets flagged, it is almost always because the destination looks offshore or poorly supervised, so I stick to venues with a real EU footprint and documented compliance.

Best Alternative Exchanges for Sparkasse Customers

If you want options beyond eToro, use exchanges that support SEPA EUR transfers and operate under German or EU licensing.

What is Sparkasse?

Sparkasse is Germany’s network of local savings banks, grouped under the Savings Banks Finance Group (Sparkassen-Finanzgruppe) and coordinated by the German Savings Banks Association (DSGV). On an aggregated basis, the group reported around EUR 2.5 trillion in total assets.

Day to day banking runs through your local Sparkasse Girokonto, using Online Banking and the App Sparkasse. Most payments and account changes are approved with S-pushTAN (or chipTAN, depending on your setup).

.webp)

Final Thoughts

If I am buying Bitcoin with Sparkasse, I keep it simple: fund in EUR using SEPA Überweisung, confirm my daily transfer limit before I send, and buy on a MiCA licensed platform once the deposit lands.

I use eToro when I want an easy multi asset account and I am fine paying 1% in and 1% out, and I switch to a lower fee exchange when I plan to trade more actively.

The practical checklist is always the same: match the beneficiary details exactly, avoid card deposits unless you are stuck, verify early so limits do not block you, and do one small test transfer before moving size.