Safest Stablecoins for 2026: USDC, USDT, USDS & USDe Ranked

Summary: The safest stablecoin in 2026 is Circle's USD Coin (USDC), now supervised federally under the GENIUS Act and licensed as an e-money token under MiCA, with monthly attestations and 1:1 redemption.

Sky's USDS has passed Ethena's USDe to become the largest stablecoin run by a decentralized protocol and the third-largest overall, showing that overcollateralized, governance-run designs scale without offshore reserves or derivatives.

Picking a safe stablecoin means reading three things at once: who supervises the issuer, what backs the token, and how the peg held when liquidity dried up.

Safest Stablecoin: Circle (USDC)

USDC keeps the top spot in 2026 by pairing the sector's most transparent reserve disclosure with the only licence covering both the United States and the European Union.

Reserves

$77B in cash and short-dated US Treasuries, managed by BlackRock

Networks

Native on 20+ chains, led by Ethereum, Solana, and Base

Market Share

~25% of the stablecoin market, second largest

What Makes a Stablecoin Safe?

A stablecoin is a promise that one token will always be worth one dollar. Safety is how credible and enforceable that promise stays when you try to redeem it under pressure. Three forces decide it, and every call in this guide traces back to them.

Backing comes first. A token is only as sound as the assets behind it and your ability to confirm they exist. Cash and short-dated US Treasuries with monthly attestations sit at the safe end; loans, gold, crypto, and derivatives add yield and add ways for the dollar to slip.

Accountability comes second. Until 2025 a stablecoin was a private promise you either trusted or did not. The GENIUS Act in the US and MiCA in the EU put named supervisors and enforceable reserve, redemption, and disclosure rules behind the largest issuers. Who is legally on the hook now counts as much as what sits in the vault.

Behaviour under stress comes third. A peg that held through bank failures, exchange blowups, and funding-rate crashes has proven something no whitepaper can. Track record is evidence; marketing is not.

That lens also explains the market's shape. Total stablecoin supply sits above $300 billion per DefiLlama, in the $305 to $320 billion range through 2026, and more than 230 million wallets now hold one. For supply, dominance, and chain data, see our stablecoin statistics page.

Why Stablecoins Fail

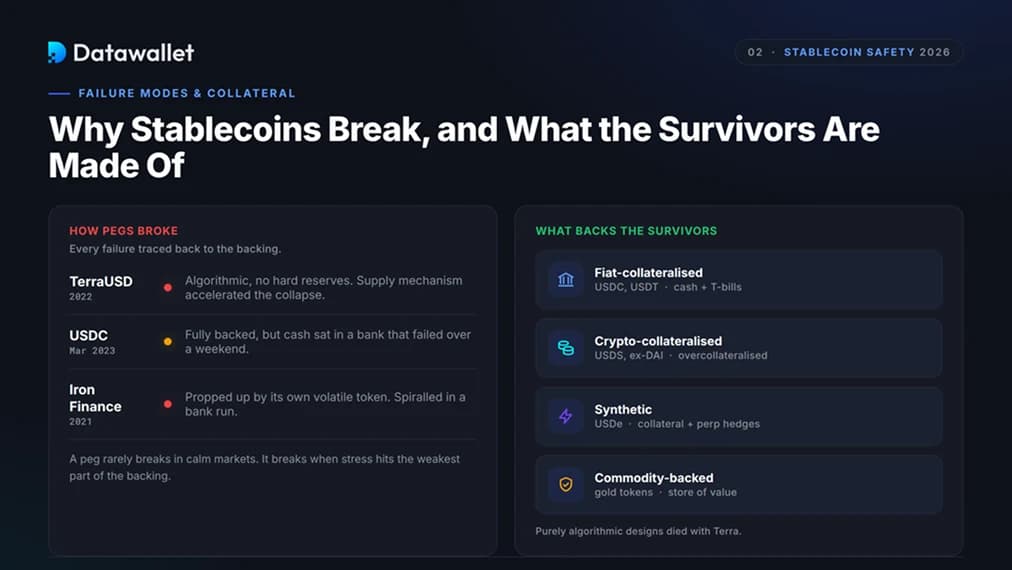

The fastest way to judge safety is to study the failures, because each one traces straight back to what backed the token. The pattern is consistent: a peg rarely breaks in calm markets, it breaks when stress hits the weakest part of the backing.

TerraUSD in 2022 held no hard reserves, so when confidence cracked, the supply mechanism meant to defend the dollar accelerated the collapse instead. USDC in March 2023 was fully backed, but part of its cash sat in a bank that failed over a weekend, and the token traded under a dollar until those deposits were confirmed safe. Iron Finance was propped up by its own volatile governance token and spiralled in a bank run. Three different fault lines, all in the backing.

The tokens that lasted moved toward harder collateral, and their models now sort cleanly by how they can fail. Purely algorithmic designs died with Terra and no longer feature.

- Fiat-collateralised (USDC, USDT): cash and short-dated government debt, redeemable 1:1. The most contained failure mode, a bank or Treasury problem, which is why this model anchors almost the entire market.

- Crypto-collateralised (USDS, the former DAI): minted against crypto deposits worth more than the coins issued, with the surplus absorbing volatility.

- Synthetic (USDe): collateral paired with short derivatives positions, holding dollar value without holding dollars. Its risk lives in funding rates, not reserves.

- Commodity-backed: tracking physical reserves like bullion. These gold-backed cryptocurrencies act more like a store of value than a spendable dollar.

Knowing the model tells you the live risks to watch. Anything backed beyond cash and Treasuries inherits the credit and custody risk of those assets. A fiat token is only as safe over a weekend as the banks holding its cash. Synthetic and leveraged-yield positions can unwind fast when funding flips or liquidity thins.

Cross-chain versions depend on crypto bridges, the single biggest source of stolen funds, and even contracts cleared by reputable auditors hide edge cases that surface only in production. A solvent token can also be delisted in a jurisdiction, as USDT was across the EU.

The 5 Safest Stablecoins in 2026

Working from those three forces, we screened the largest tokens on DefiLlama and CoinMarketCap and ranked the five that lead their categories, weighting accountability and verifiable backing most. They cover the regulated dollar, the offshore dollar, the decentralised dollar, the synthetic dollar, and the regulated euro.

1. USD Coin (USDC)

USDC holds roughly $77 billion in circulation and about a quarter of all stablecoin supply, and its safety case rests on disclosure no rival matches. Reserves sit in cash at large banks and short-dated US Treasuries inside the Circle Reserve Fund, an SEC-registered government money market fund managed by BlackRock and custodied at BNY Mellon, with monthly Deloitte attestations and a mix near 80% Treasuries, 20% cash.

The bigger shift is legal. Circle, public on the NYSE since June 2025, now falls under GENIUS Act federal supervision and in late 2025 won conditional OCC approval to run its reserves through a national trust bank. In Europe it operates as a MiCA e-money token through its ACPR-licensed French entity. No other major holds that combination, which is why institutions default to USDC for payroll, treasury, and settlement.

The trade-offs are real. Circle earns almost all its revenue from interest on reserves, so falling Treasury yields would squeeze the issuer even with the peg intact, and regulation is splitting USDC into separate US and EU programs. Its one depeg came in March 2023, when $3.3 billion of cash was briefly stranded in the failed Silicon Valley Bank; the peg recovered within three days once the deposits were backstopped.

Key advantages

- Only major stablecoin supervised under both the GENIUS Act and MiCA

- Reserves held in a BlackRock-run government money fund, attested monthly by Deloitte

- Conditional OCC trust-bank approval brings reserve management further in-house

2. Tether (USDT)

USDT is still the largest stablecoin by a wide margin, near $189 billion outstanding and about 58% of supply. Its edge is liquidity: the default trading pair on most exchanges, the dominant dollar for emerging-market remittances, and the most-used settlement asset on Tron. Per Tether's transparency reporting and quarterly BDO Italia attestations, reserves run roughly 80% US Treasuries, about $141 billion in bills that rank Tether among the world's largest holders, with smaller allocations to secured loans, gold, and Bitcoin. The company cleared more than $10 billion in net profit in 2025 and another $1 billion in Q1 2026.

The safety question is structural, not whether the dollars exist. Tether has run on point-in-time attestations rather than a full audit for its entire history, though it engaged KPMG for its first complete audit, which began in early 2026. Its offshore base also leaves it outside the GENIUS Act, and it has been delisted from regulated EU venues under MiCA.

Tether's answer is USAT, a separate US-regulated token issued through OCC-chartered Anchorage Digital Bank with Deloitte-attested reserves. It grew more than 500% in April 2026 but still sits near $140 million, so the flagship carries the liquidity while the compliant sibling carries the licence.

Key advantages

- Deepest liquidity and the widest exchange and chain coverage of any stablecoin

- Reserves now around 80% short-dated Treasuries, with a first full audit underway via KPMG

- A separate GENIUS-compliant USAT extends Tether into the regulated US market

3. Sky Dollar (USDS)

USDS is the headline change in this year's ranking. Issued by Sky Protocol, the rebranded successor to MakerDAO, it has grown to around $9 billion in supply, the largest stablecoin run by a decentralized protocol and the third-largest overall. DAI still converts to USDS 1:1, and the peg holds through overcollateralised vaults, a Peg Stability Module that swaps USDC at a dollar, and arbitrage against on-chain liquidity.

The conservatism behind the yield is what makes it credible. Backing spans tokenised US Treasuries, crypto vaults, and protocol-owned liquidity, allocated by the Sky Agent Network of independent managers who compete to deploy reserves. The sUSDS savings wrapper has passed $6 billion, the largest yield-bearing stablecoin balance in the market, and its Spark sub-DAO extends USDS into lending and cross-chain savings. Sky cleared roughly $124 million in gross revenue and a $46 million surplus in Q1 2026.

The risks are the usual DeFi ones: smart-contract exposure across the vaults, governance concentration through the SKY token, and counterparty risk on the real-world assets behind the yield. Our full breakdown sits in the USDS explainer.

Key advantages

- Largest non-custodial dollar, with reserves and governance fully on-chain

- Overcollateralised crypto plus real-world-asset backing on battle-tested Maker-era contracts

- sUSDS and the Spark sub-DAO turn idle USDS into transparent, governance-set yield

4. Ethena USD (USDe)

USDe is the most interesting and most cautionary entry. It is a synthetic dollar that holds its peg by pairing crypto collateral, including staked ETH, BTC, and SOL, with offsetting short perpetual positions, so the combined book stays close to dollar-neutral whatever the price does. That design let it scale faster than any stablecoin in history, peaking near $14 billion in 2025 before settling around $4.5 billion.

The round trip is the lesson. Yield, paid through the staked sUSDe token, depends on perpetual funding staying positive; when funding compressed, Ethena rotated backing toward Treasury bills and its own USDtb token, which holds BlackRock's tokenised BUIDL fund. That steadied the peg but cut the yield that drew capital in, and much of the supply had been looped through leverage on lending markets, amplifying both gains and unwinds.

USDe sits outside the GENIUS Act's payment-stablecoin definition, so it cannot be sold as one to US persons without restructuring, and it leans on centralised exchanges to hold its hedges. Ethena is pushing upmarket with iUSDe, an institutional version wrapped for compliance, yet its backing still rests on the same traditional rails it set out to replace. The mechanics are covered in our Ethena guide.

Key advantages

- Scales without bank reserves, the most capital-efficient dollar in the market

- Backing now blends perp hedges with BUIDL-backed USDtb for steadier collateral

- iUSDe and deep exchange integrations are opening an institutional channel

5. Euro Coin (EURC)

EURC is the clearest winner from MiCA enforcement. Issued by Circle's ACPR-licensed French entity and backed 1:1 by euro cash and short-duration EU government debt with monthly attestations, it has grown to roughly $430 million and holds 40% to 50% of the euro stablecoin market. That lead came less from product design than from regulation clearing the field: as non-compliant euro tokens were delisted from EU exchanges, liquidity pooled into the few licensed options, and EURC held its peg while rivals slipped.

For euro trading, on-chain FX, and EUR-to-USDC settlement through Circle Mint, EURC is the most credible regulated choice, running natively on Ethereum, Solana, Base, Avalanche, and Stellar. Circle has also pushed it into physical retail through an integration with Ingenico's 40 million payment terminals.

The catch is scale: the whole euro stablecoin segment is a rounding error next to the dollar market, so liquidity outside the largest venues can be thin.

Key advantages

- Largest MiCA-compliant euro stablecoin, passported across all 27 EU member states

- Same Circle reserve and attestation discipline as USDC, denominated in euros

- Native on five chains with growing point-of-sale and FX settlement use

Do Safe Stablecoins Pay Yield?

There is a reason the safest dollar tokens pay you nothing for holding them, and one clause explains it. The GENIUS Act bars licensed issuers from paying yield directly to holders of a payment stablecoin, so the yield did not vanish. It moved one layer out, into wrapper tokens and savings modules built on top of the base coin.

That is why you earn on the wrapped versions, not USDC or USDS themselves. The wrappers split into three risk profiles worth keeping straight:

- Savings wrappers: sUSDS pays a governance-set rate funded by the protocol's collateral, lately in the high-3% range and tracking the Federal Reserve with a lag. Smoother, but adjustable by vote.

- Basis-trade wrappers: sUSDe pays whatever perpetual funding yields, historically higher but volatile, and capable of briefly turning negative.

- Treasury wrappers: Pass through short-dated government yield minus a fee, the lowest-volatility option, at the cost of KYC and trust in a centralised issuer.

So a headline APY tells you almost nothing without the structure behind it. A governance-set 4% and a 9% leveraged-loop window during an incentive period are not the same product, and treating them alike is how holders get hurt. We track live rates and the risk behind each in our guide to the best stablecoin interest rates. The yield itself almost always traces back to tokenised real-world assets, now the engine powering the safest end of the market.

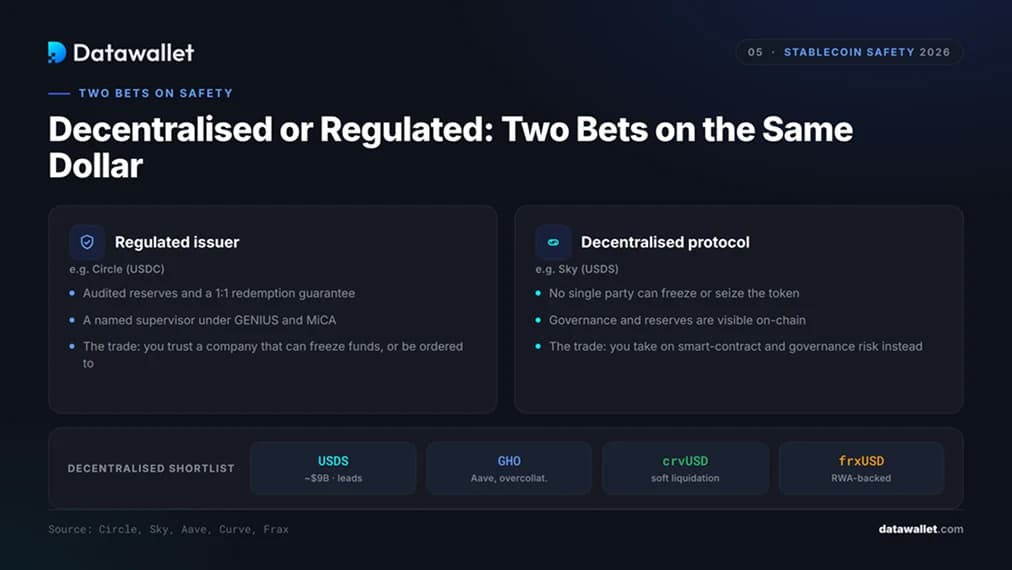

Decentralized vs Regulated Stablecoins

A safe stablecoin can come from two opposite places, and the real choice is which risk you would rather hold. A regulated issuer like Circle gives you audited reserves, a redemption guarantee, and a supervisor to answer to, in exchange for trusting a company that can freeze funds or be ordered to. A decentralized protocol removes that single point of control and hands you smart-contract and governance risk instead.

On the decentralized side, only a short list clears the bar in 2026. USDS leads on scale, capitalisation, and integration. Aave's GHO is next, minted against overcollateralised deposits inside one of DeFi's most tested lending markets. Curve's crvUSD uses soft liquidation, selling collateral gradually as prices fall rather than in abrupt blocks, which has held through several drawdowns. Frax's frxUSD has moved to fuller collateralisation with tokenised Treasury backing.

What unites the survivors is harder collateral and clearer reserves, while the tokens that leaned on reflexive or thinly backed designs are gone. Neither path wins outright: a regulated coin shields you from code and crypto volatility, a decentralized one shields you from a single issuer or regulator. Most holders end up wanting some of each for different jobs.

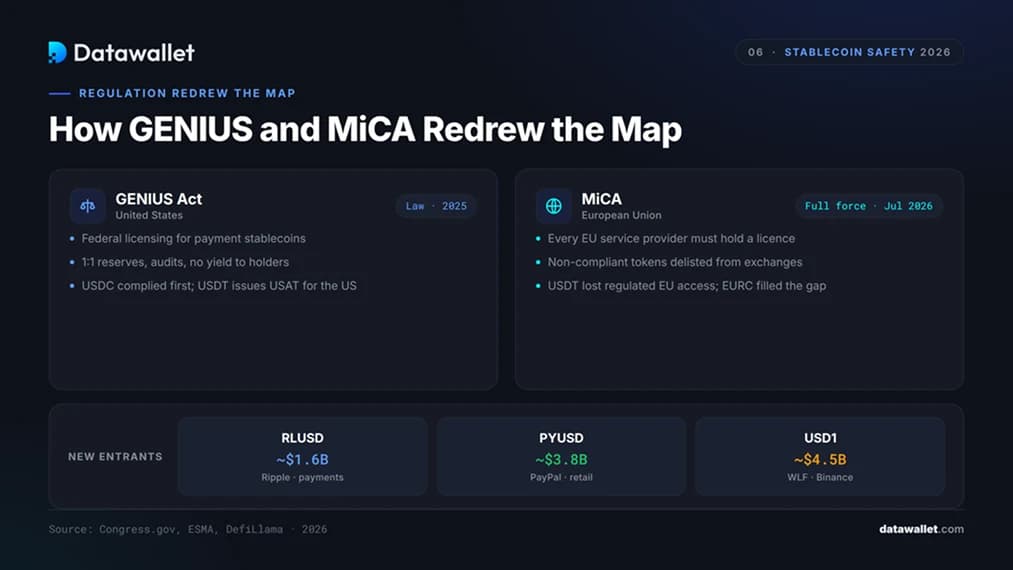

Stablecoin Regulation in 2026: GENIUS and MiCA

Two laws now decide which stablecoins operate where, reshaping the field more than any product launch. MiCA reached full enforcement on 1 July 2026, forcing EU exchanges to delist unlicensed tokens. The GENIUS Act set up US federal licensing, with rules finalised in mid-2026, while the CLARITY Act still works out how the SEC and CFTC divide the rest.

The result is a clean split between compliant and offshore money. Circle sailed through, since USDC and EURC were built to these standards. Tether spun up the separate USAT for the US while its flagship lost regulated EU access, opening room for new entrants:

- Ripple's RLUSD has passed $1.6 billion in enterprise payments and settlement, with a Mastercard tie-in and a Singapore central-bank pilot.

- PayPal's PYUSD, issued by Paxos, sits near $3.8 billion on PayPal and Venmo.

- World Liberty Financial's USD1 reached roughly $4.5 billion via Binance and BitGo custody, though its political ownership draws heavy scrutiny.

Bank and sovereign issuers are arriving too, from a European bank consortium's euro token to Japan's yen-backed JPYC. A parallel fight is breaking out over who keeps the yield reserves generate: Hyperliquid tried to launch its own stablecoin to recapture that income and ended up handing Coinbase its USDC treasury instead. Expect that economic question, alongside the regulatory one, to shape who gains share next.

The Bottom Line

For money you cannot afford to see wobble, USDC is the safest stablecoin in 2026. It carries the clearest supervision, the most verifiable reserves, and a redemption guarantee that has been tested and held. GENIUS and MiCA turned what used to be trust in a company into enforceable obligation, and Circle was built for exactly that.

The more telling shift sits a layer down. USDS scaling into the top three shows the decentralized model matured rather than faded, while USDe's slide from its peak is a reminder that synthetic yield is cyclical and leverage cuts both ways. The market has consolidated around conservative collateral, real-world-asset yield, and named supervisors, and the tokens that ignored those shifts are gone.

For most holders, safety comes from a deliberate match of token to purpose rather than a single coin: a regulated dollar for core balances, a yield wrapper sized for its risk, and a clear view of what backs anything you hold. In a market this size, that discipline beats chasing the highest advertised rate.

Frequently asked questions

.webp)