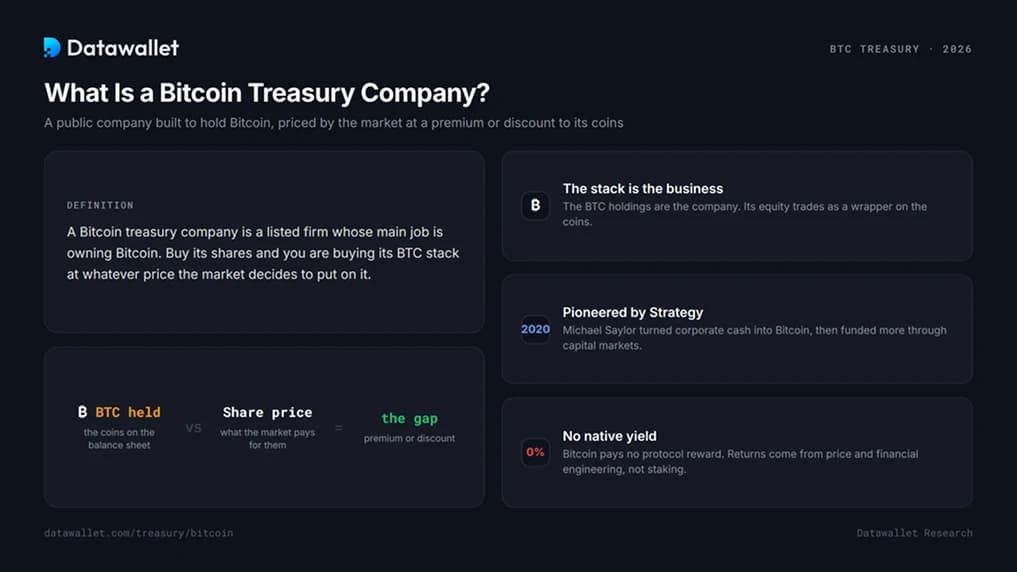

What Is a Bitcoin Treasury Company?

A Bitcoin treasury company is a listed firm whose main job is owning Bitcoin. You buy its shares and you are, in effect, buying its BTC stack at whatever price the stock market decides to put on it.

That last part is the whole game. The stock almost never trades at exactly the value of the Bitcoin behind it. When it trades higher, the company can raise money and buy more coins than the dilution costs existing holders. When it trades lower, that machinery seizes up. Everything below is an explanation of why the gap exists, who has exploited it best, and what happens when it closes.

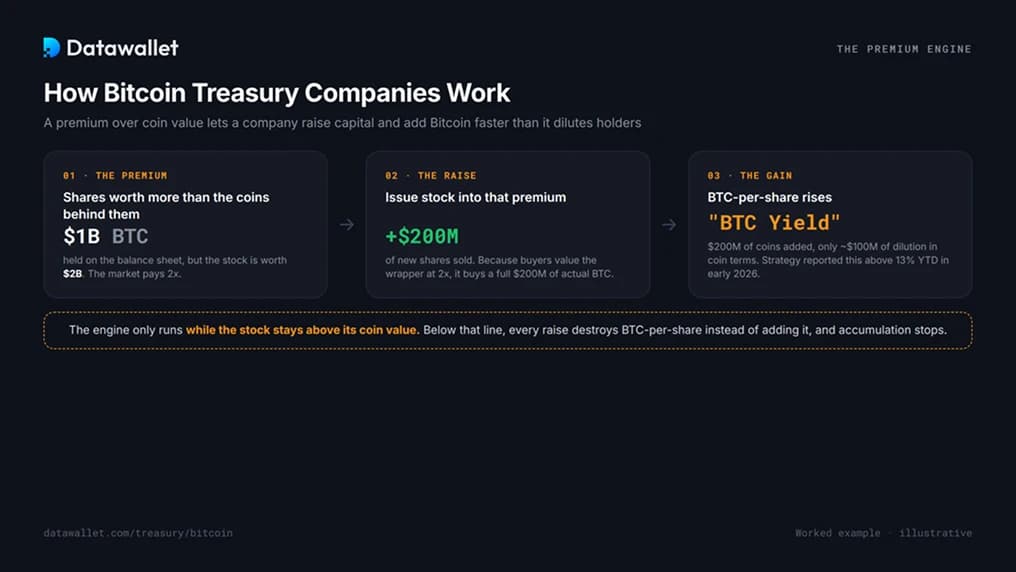

How Bitcoin Treasury Companies Work

Picture a company holding $1 billion of Bitcoin whose shares are collectively worth $2 billion. The market is paying two dollars for every dollar of coins. That gap is not a glitch; it is the engine.

The company sells, say, $200 million of new stock. Because buyers value the wrapper at twice its Bitcoin backing, that $200 million buys $200 million of actual BTC while only diluting existing shareholders by the equivalent of $100 million in coin terms. Bitcoin-per-share goes up. Strategy named this effect "BTC Yield" and reported it running above 13% year-to-date in early 2026, a figure that measures coin accumulation per share rather than any interest paid.

Two things keep the engine running, and both can fail. The shares have to stay above the value of the underlying Bitcoin, or new raises start destroying coin-per-share instead of adding it. And buyers have to keep showing up for the paper, since a treasury that cannot issue cannot accumulate. A 2024 accounting change that let firms carry Bitcoin at market value, rather than writing it down and never up, removed the last reason a CFO had to say no.

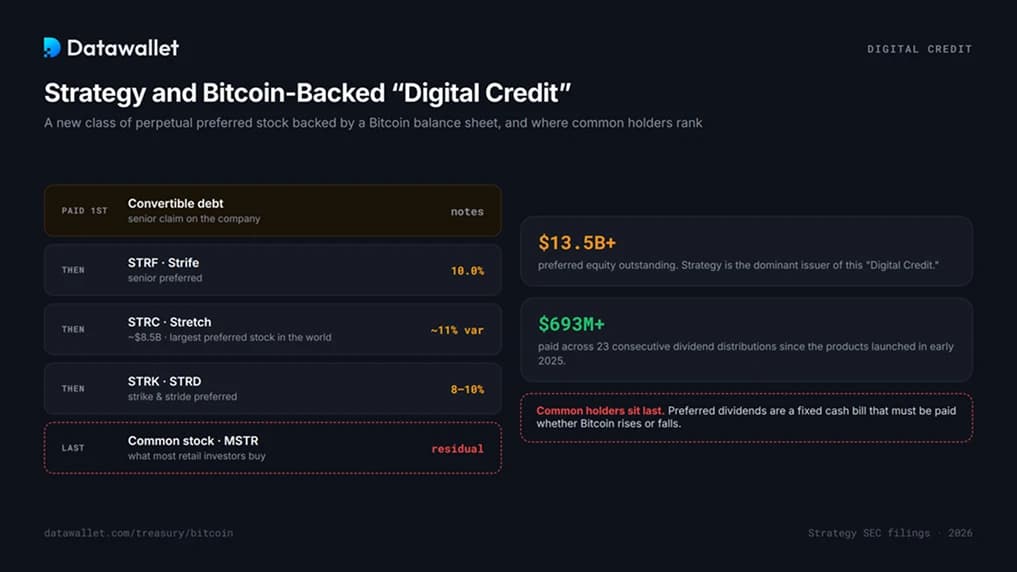

Strategy and Bitcoin-Backed "Digital Credit"

Most coverage calls Strategy a leveraged Bitcoin bet. That undersells what it actually built. Beyond common stock and convertible notes, the company spent 2025 and 2026 issuing a family of perpetual preferred shares, traded under tickers like STRC, STRK, STRF and STRD, that it markets as "Digital Credit": income instruments backed by a Bitcoin balance sheet rather than by cash flows.

The scale is hard to overstate. Strategy describes itself as the dominant issuer of this new instrument, with over $13.5 billion of preferred equity outstanding, and its flagship STRC reached roughly $8.5 billion in market value within nine months of launch, which the company claims makes it the largest preferred stock in the world. STRC pays a variable dividend, recently above 11% annualized, and is engineered to trade near a stable $100 by adjusting that rate monthly. The pitch to investors is bitcoin's upside funding, equity-like returns with credit-like volatility.

For the buyer of common MSTR stock, this changes the risk picture. The preferred holders sit ahead of you. Their dividends, which Strategy has paid across more than 23 consecutive distributions totaling several hundred million dollars, are a fixed cash obligation that must be met whether Bitcoin rises or falls. In good years that leverage magnifies coin accumulation. In bad ones it is a bill that arrives regardless.

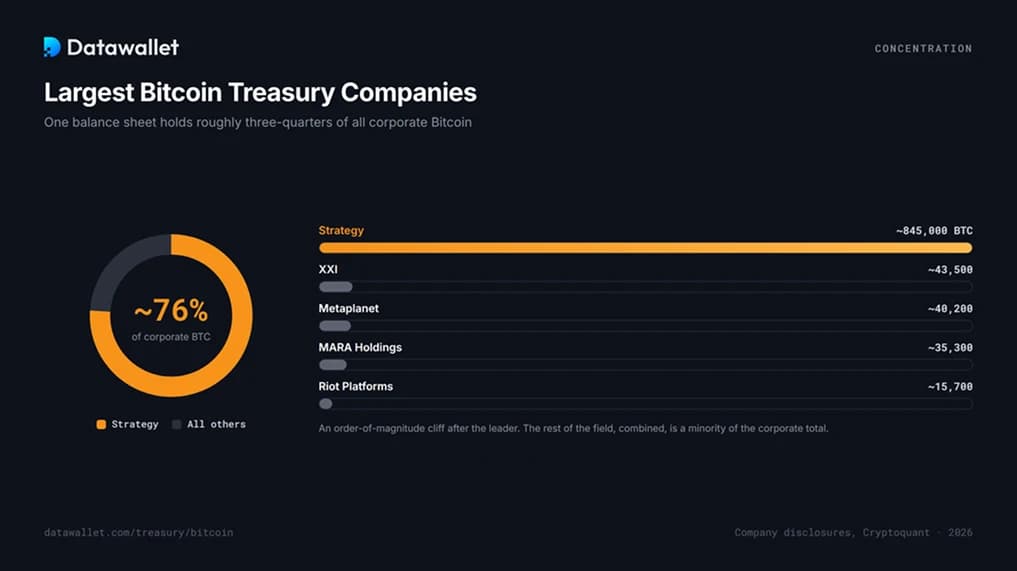

Largest Bitcoin Treasury Companies

The shape of the ranking matters more than the order. Strategy sits at the top with roughly 845,000 BTC, and by early 2026 it held about three-quarters of all Bitcoin owned by public treasury companies. Over a recent 30-day stretch it bought around 45,000 BTC while every other public treasury combined added close to a thousand, with non-Strategy buying down roughly 99% from its 2025 peak. The category collapsed inward toward one balance sheet.

The names below it each hold tens of thousands of coins, an order of magnitude behind and collectively a minority of the corporate total. What separates them is strategy, not scale:

- Twenty One (XXI) is fusing custody, payments, and mining into one vertically integrated entity rather than a pure holding vehicle.

- Metaplanet has chased an aggressive accumulation target as Japan's answer to the Strategy playbook.

- MARA and Riot hold their stacks partly as a byproduct of mining, not as the core thesis.

When people debate the Bitcoin treasury trade, they are mostly debating one company's capital structure. Datawallet's Ethereum treasury tracker shows a different shape, where staking income rather than financial engineering separates the leaders.

What mNAV Means for Treasury Stocks

The number that captures all of this is mNAV, a company's market value divided by the worth of its Bitcoin, with the careful version adding debt and preferred stock into the numerator. It reads as a simple multiple:

- Above 1.0 is a premium. At an mNAV of 2.0, the market pays two dollars for every dollar of coins. Every capital raise is accretive, and the flywheel turns.

- At 1.0, the stock is worth exactly its coins. The premium that justified owning the stock over plain Bitcoin has thinned to nothing.

- Below 1.0 is a discount. The shares are worth less than the Bitcoin they represent. Raising money would hand new investors cheap claims on existing coins, so disciplined managers stop issuing.

That threshold is where treasury companies live or die, and it is not theoretical. Even Strategy slipped to a fractional discount in November 2025 for the first time in nearly two years, and Metaplanet watched its multiple fall from roughly eight times coin value toward parity even as Bitcoin itself climbed.

The per-company mNAV column in the table above is the single fastest health check on any name in the sector.

Bitcoin Treasury Stock vs Spot Bitcoin ETF

Since 2024 there has been a simpler way to own Bitcoin in a brokerage account, and it competes directly with every treasury stock. A spot Bitcoin ETF holds coins in custody and tracks the price almost exactly, charging a fee in the region of 0.12% to 0.25%. No premium, no debt, no dividend obligations, and shares you can redeem against the underlying.

A treasury stock offers something the ETF deliberately does not: leverage and a premium. Strategy has massively outrun the largest ETF since both became available, precisely because corporate borrowing amplifies Bitcoin's gains. The catch is symmetry. In the early-2026 selloff Bitcoin dropped around 36% and Strategy fell closer to 45%, because a shrinking premium subtracted equity value on top of the coin decline. The honest way to hold both ideas: an ETF is Bitcoin, a treasury stock is a geared trade on Bitcoin with a sentiment premium bolted on. One is an allocation, the other is a position.

Risks of Bitcoin Treasury Companies

The failure modes here are corporate-finance failures, not crypto ones, which is what makes them easy to underestimate:

- The premium is sentiment, and sentiment leaves. Unlike an ETF share, a treasury share cannot be redeemed for coins, so nothing anchors the premium. When it goes, no arbitrage drags it back.

- Borrowed money comes due. Convertible notes must convert into stock or be repaid. A share price stuck below the conversion level at maturity turns a financing tool into a cash demand.

- Preferred dividends do not pause for bear markets. The Digital Credit stack carries fixed payouts owed in cash whatever Bitcoin does, a standing drain that bites hardest exactly when the coins are worth least.

- A discount can feed on itself. A falling share price weakens confidence, the discount widens, and a leveraged firm may end up selling the very Bitcoin it was built to hoard.

- "Never sell" has an expiry date. Several smaller treasuries have already liquidated coins to clear debt, and at least one large miner formally dropped its no-sale pledge. Conviction is a policy, not a guarantee.

This page is information, not investment advice. Anyone who simply wants Bitcoin exposure can hold the coin or a spot ETF and skip the corporate layer entirely.

How to Verify Corporate Bitcoin Holdings

Treasury disclosures deserve verification rather than trust, and Bitcoin makes that unusually easy. Start with the company's own filings and press releases, which state coin counts and capital structure. When a firm publishes its wallet addresses, you can read the balance straight off the chain on an explorer such as mempool.space, with no middleman between you and the ledger. A third-party proof-of-reserves attestation, where available, ties the filed numbers to the on-chain ones. Treat agreement across all three as the real confirmation, and a company that discloses none of them as a question worth asking.

Frequently Asked Questions

Which company owns the most corporate Bitcoin?

Strategy, formerly MicroStrategy, by an enormous margin: roughly 845,000 BTC, near 4% of all the Bitcoin that will ever exist, and by early 2026 about three-quarters of every coin held across public treasury companies. The live table at the top of this page ranks the rest.

If Bitcoin pays no yield, how do these companies profit?

Two ways, neither involving interest on the coins. They aim to grow Bitcoin-per-share by issuing stock at a premium and buying more BTC, and shareholders ride Bitcoin's price through a geared wrapper. Strategy adds a third line by issuing bitcoin-backed preferred stock to outside income investors.

What is "Digital Credit"?

Strategy's term for the perpetual preferred shares it issues, such as STRC, which pay a dividend and are backed by its Bitcoin balance sheet rather than by operating cash flow. It has become the largest issuer of these instruments, marketing them as income products with equity-like upside and lower volatility.

Why does the share price swing more than Bitcoin itself?

Leverage and the premium. Borrowed capital amplifies Bitcoin's moves in both directions, and the mNAV premium adds a second, sentiment-driven layer of volatility that an ordinary coin holder never experiences. Treasury stocks routinely fall further than Bitcoin in selloffs and rise further in rallies.

Is a treasury stock just a Bitcoin ETF with extra steps?

No, and the difference matters. An ETF tracks Bitcoin closely for a small fee and is redeemable for coins. A treasury stock layers on corporate debt, dividend obligations and a premium that can vanish, making it a leveraged trade rather than clean exposure.

How do I confirm a company actually holds the Bitcoin it claims?

Cross-check three things: the figures in its public filings, the on-chain balance at any wallet address it discloses (readable on a block explorer), and any independent proof-of-reserves report. When all three agree, the holding is real; when a company offers none, treat the claim with caution.