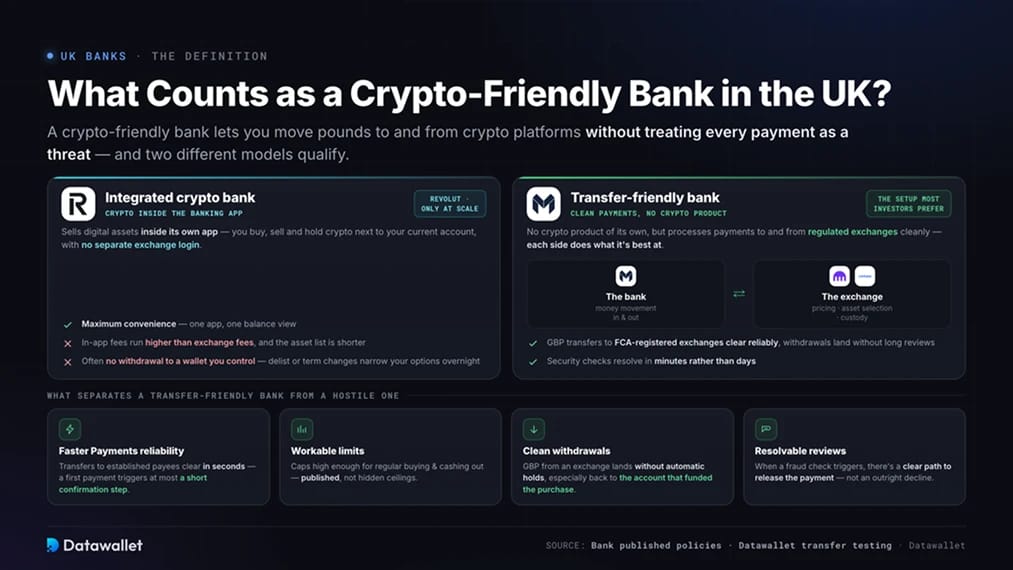

What Counts as a Crypto-Friendly Bank in the UK?

A crypto-friendly bank lets you move pounds to and from crypto platforms without treating every payment as a threat. In practice that means GBP transfers to FCA-registered exchanges clear reliably, withdrawals back to your account arrive without long reviews, and any security checks can be resolved in minutes rather than days.

Two different models qualify.

Integrated crypto banks

An integrated crypto bank sells digital assets inside its own app. You buy, sell and hold crypto next to your current account, with no separate exchange login. Revolut is the only UK bank operating this way at scale.

The convenience carries costs. In-app trading fees run higher than exchange fees, the asset list is shorter, and you often cannot withdraw coins to a wallet you control. If the bank delists an asset or changes its terms, your options narrow overnight.

Transfer-friendly banks

A transfer-friendly bank offers no crypto product of its own but processes payments to and from regulated exchanges cleanly. You keep the bank for money movement and use an exchange for pricing, asset selection and custody, the setup most active investors prefer.

What separates a transfer-friendly bank from a hostile one:

- Faster Payments reliability: Transfers to established exchange payees clear in seconds, and a first payment to a new payee triggers at most a short confirmation step.

- Workable limits: Any caps on crypto payments are high enough for regular buying and cashing out, and the bank publishes them rather than applying hidden ceilings.

- Clean withdrawals: GBP arriving from an exchange lands without automatic holds, especially when it returns to the account that funded the purchase.

- Resolvable reviews: When a fraud check does trigger, the bank offers a clear path to release the payment instead of an outright decline.

Top Crypto-Friendly Banks in the UK

The table below summarises where every major UK bank stands. Restriction levels reflect published policies and our own transfer testing against FCA-registered exchanges.

1. Revolut

Revolut leads this ranking as the one UK bank that treats crypto as a product rather than a risk to be contained. You can trade more than 200 cryptocurrencies inside the main app, and active traders get Revolut X, a separate exchange interface with deeper order books and lower fees.

Its regulatory position also changed this year. In March, the PRA lifted the restrictions on its licence and Revolut Bank UK Ltd launched as a fully authorised bank, giving eligible deposits protection from the Financial Services Compensation Scheme of up to £120,000 per person. Crypto balances sit in a separate Revolut entity and carry no FSCS cover, so only your pounds are protected.

The weaknesses are cost and custody. In-app trading fees start at 1.49% unless you pay for a plan, and most coins cannot be withdrawn to a private wallet. We cover the full fee schedule in our Revolut crypto fees guide. For larger positions, use Revolut for GBP transfers and buy on a full exchange instead.

2. Monzo

Monzo is the cleanest transfer-friendly option among UK digital banks. It publishes its policy openly, names supported exchanges such as Coinbase in its help pages, and processes Faster Payments to registered platforms in seconds.

The constraint is its cryptocurrency allowance, a fixed £5,000 across any rolling 30-day period introduced in April last year. Monzo will not raise it, even on paid plans, and payments to Binance are declined outright following an FCA consumer warning. For anyone investing under £5,000 a month, neither restriction will register.

3. Lloyds Bank

Lloyds stands out among the high-street banks because it publishes no transfer caps on crypto payments. Faster Payments to FCA-registered exchanges generally clear, and in our testing an established payee behaves like any other transfer.

The bank has blocked credit card purchases of crypto since 2018, and payments to Binance are stopped across the Lloyds Banking Group brands. Treat Lloyds as a bank-transfer account, send a small first payment to establish each new exchange payee, and scale from there.

4. Co-operative Bank

Co-operative Bank, now part of Coventry Building Society, takes the quietest approach on this list. It publishes no crypto policy at all, which cuts both ways. There are no stated caps to plan around, but there is also no documented commitment you can point to if a payment is held.

We sent a £1,000 Faster Payments transfer to an FCA-registered exchange from a Co-op account and the deposit was credited immediately. The sensible pattern is a small test payment to any new exchange, then routine transfers once the payee has a clean history.

5. Nationwide

Nationwide sits in the middle of the market. Its published policy allows up to £5,000 a day in Faster Payments transfers to buy crypto, and sets no monthly ceiling. That daily cap supports regular purchases and staged cash-outs, though anyone moving larger sums in one go will need a second bank.

Nationwide is currently restricting debit card payments to crypto platforms, credit card purchases are banned, and the FlexOne youth account cannot buy crypto at all. Since absorbing Virgin Money, Nationwide has been aligning the two brands, so expect Virgin Money accounts to follow the same rules.

UK Banks That Block or Cap Crypto Payments

The rest of the market runs from restrictive to closed. UK banks tightened rather than relaxed their controls over the past year, even as the country's first full crypto rulebook moved through Parliament. A UK Cryptoasset Business Council survey found that 80% of exchanges saw more customers hit bank transfer blocks last year, with around 40% of crypto transactions blocked or delayed.

Banks with total blocks

These four banks decline payments they identify as crypto-related, regardless of the destination exchange's regulatory status.

- Chase UK: Declines all outgoing payments to crypto providers by card and bank transfer, though it still accepts funds arriving back from exchanges.

- Starling Bank: Enforces a platform-wide block on sending money to crypto exchanges by card or transfer.

- Metro Bank: Does not process outbound payments to known crypto exchanges.

- TSB: Restricts all cryptocurrency payments and has done since 2021.

None of these is workable as a primary account for crypto. If you bank with one of them, open a second account before you fund any exchange.

Banks with hard caps

These banks process crypto payments but enforce ceilings that make frequent or larger transactions unreliable.

- Barclays: Blocked all card purchases from June last year, then introduced Faster Payments limits of £2,500 per transaction and £10,000 per calendar month from December. The monthly cap counts payments from every account you hold, joint and business accounts included.

- HSBC: Caps crypto payments at £2,500 per transaction and £10,000 in any rolling 30-day period, applied identically to bank transfers and debit cards. Credit card purchases are refused.

- NatWest: Limits crypto transfers to £1,000 a day and £5,000 in any 30-day period, including attempted and rejected payments, measured per person across all accounts.

- RBS: Applies the same NatWest Group controls. Crypto payments are monitored continuously and capped at £5,000 in any rolling 30-day period.

- Santander: Limits exchange payments to £1,000 per transfer and £3,000 in any rolling 30-day period, and has a record of declining first-time payments to new exchange payees.

- First Direct: Caps single payments at £2,500 with a £10,000 ceiling across any 30-day period.

Across nearly every high-street name, payments to Binance are blocked separately and more aggressively than payments to other exchanges, a legacy of the FCA's 2021 warning about Binance Markets Limited. If your bank allows crypto transfers at all, an FCA-registered exchange such as Kraken or Coinbase will clear far more reliably.

Why Do UK Banks Block Crypto Transactions?

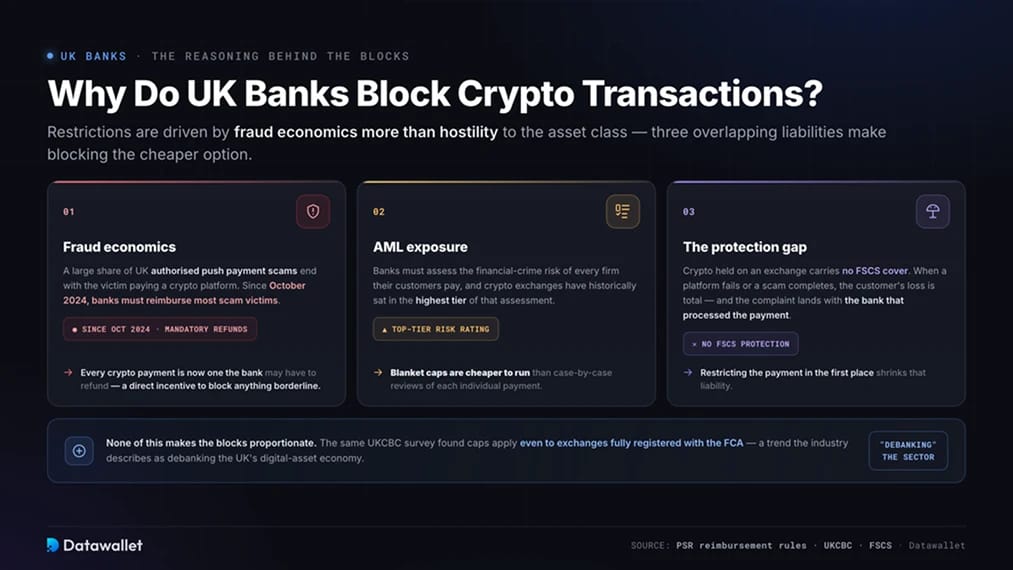

Bank restrictions are driven by fraud economics more than by hostility to the asset class. A large share of UK authorised push payment scams end with the victim sending money to a crypto platform, and since October 2024 banks have been required to reimburse most scam victims. Every crypto payment a bank waves through is now a payment it may have to refund, which gives fraud teams a financial incentive to block anything borderline.

Anti-money laundering exposure adds a second layer. Banks must assess the financial crime risk of the firms their customers pay, and crypto exchanges have historically sat in the highest tier of that assessment. Blanket caps are cheaper to run than case-by-case reviews.

The third driver is the protection gap. Crypto held on an exchange carries no FSCS cover, so when a platform fails or a scam completes, the customer's loss is total and the complaint lands with the bank that processed the payment. Restricting the payments in the first place shrinks that liability.

None of this makes the blocks proportionate. The same UKCBC survey found the blocks apply even to exchanges fully registered with the FCA, and the industry has described the trend as debanking the UK's digital asset economy. But it explains why the tightening continued through a period when regulation was arriving.

How the New UK Crypto Rules Change the Picture

The UK's regulatory landscape shifted more in the past twelve months than in the previous decade, and bank policy will eventually have to respond. Parliament passed the Financial Services and Markets Act 2000 (Cryptoassets) Regulations in February, bringing exchanges, custodians, dealers and staking providers inside the FCA's full regulatory perimeter for the first time.

The timeline is now fixed. The FCA published its final core rules for the regime on 30 June, covering stablecoin backing, custody, market abuse and minimum capital rules. Firms can apply for authorisation from 30 September, firms that apply by 28 February 2027 can keep operating while their application is assessed, and from 25 October 2027 any platform without FCA authorisation must stop serving UK customers.

Three other developments matter for anyone weighing up banks:

- Regulated exposure without transfers: The FCA reopened retail access to crypto exchange traded notes in October, so you can now hold Bitcoin or Ethereum exposure through a stockbroker on a recognised UK exchange. Your bank cannot block a brokerage purchase the way it blocks an exchange transfer, though ETNs carry issuer risk and no FSCS cover.

- Stablecoin rules: The Bank of England published its final framework for systemic sterling stablecoins in June, clearing the way for regulated digital pounds issued at scale. Banks that block exchange payments today are building for tokenised money tomorrow.

- Tax reporting: Under the Crypto-Asset Reporting Framework, exchanges serving UK users now report customer transaction data to HMRC, which cross-references it against tax returns. Keep records of every deposit and withdrawal, because your bank statements and your exchange history are both visible to the tax authority.

The honest read is that bank caps are unlikely to loosen before authorised exchanges start operating under the full regime. Once platforms carry FCA authorisation, Consumer Duty obligations and capital requirements, the fraud-risk justification for blanket blocks becomes harder for banks to defend. Until then, plan around the caps rather than waiting for them to lift.

How to Set Up Reliable GBP Transfers

A few habits remove most of the friction UK users report:

- Send a test payment first: A £10 transfer to a new exchange payee establishes the destination in your bank's risk model before real money moves.

- Reuse the same payee details: Fraud systems score payment patterns, so identical payee names and references make each subsequent transfer look routine.

- Cash out to the funding account: Withdrawing GBP to the same account you deposited from avoids the new-payee checks that delay withdrawals to unfamiliar accounts.

- Keep a second bank account: Fraud checks trigger without warning, so a backup account at a different bank means a held payment never locks you out of a market move.

- Prefer Faster Payments over cards: Card payments pass through merchant category filters that banks use to decline crypto purchases, while account-to-account transfers face fewer automated blocks and no card processing fees.

What is the Safest UK Crypto Exchange?

Coinbase is our pick for British users because its FCA approvals, safeguarded GBP handling and public-company auditing go further than the rest of the market.

- UK regulatory standing: Coinbase serves UK customers through CB Payments Ltd, authorised by the FCA as an electronic money institution and registered for cryptoasset activities (register number #900635).

- Safeguarded GBP balances: Pounds held on Coinbase sit as safeguarded e-money, kept separate from the company's own funds, so customers rank ahead of general creditors if the firm ever failed.

- Public-company transparency: Coinbase Global is listed on Nasdaq and files externally audited financial statements, so its customer asset holdings are checked by independent auditors rather than self-reported.

- Audited security controls: Coinbase completes SOC 1 and SOC 2 reports and keeps around 98% of customer digital assets in offline cold storage, away from internet-exposed systems.

- GBP support built for UK banks: Free Faster Payments deposits and withdrawals move account to account, the payment type UK banks decline least when they tighten rules on crypto merchants.

No exchange removes risk entirely, and nothing held on any platform carries FSCS protection. But for a UK user pairing a bank account with one exchange, Coinbase offers stronger sterling protections and clearer external auditing than any rival we have tested. Our full Coinbase review covers fees, products and platform depth.

Final Thoughts

The crypto-friendly banking question in the UK has a clearer answer than it did a year ago. Revolut now pairs a full banking licence with in-app trading, Monzo offers the cleanest transfer experience under a fixed allowance, and Lloyds, Co-op and Nationwide remain workable for bank-transfer investing. The rest of the high street ranges from capped to closed.

Structure matters more than bank choice, though. Run one reliable main account plus a backup, fund exchanges by Faster Payments rather than cards, test each new payee with a small transfer, and cash out to the account you funded from.

The regulatory ground is also shifting under the banks. With FCA authorisation opening to exchanges in September and the full regime arriving in October 2027, the justification for blanket blocks will weaken. Until it does, pick a bank from the top of this list and build your setup around the published caps.