Compare Top Stablecoin Interest Rates Platforms

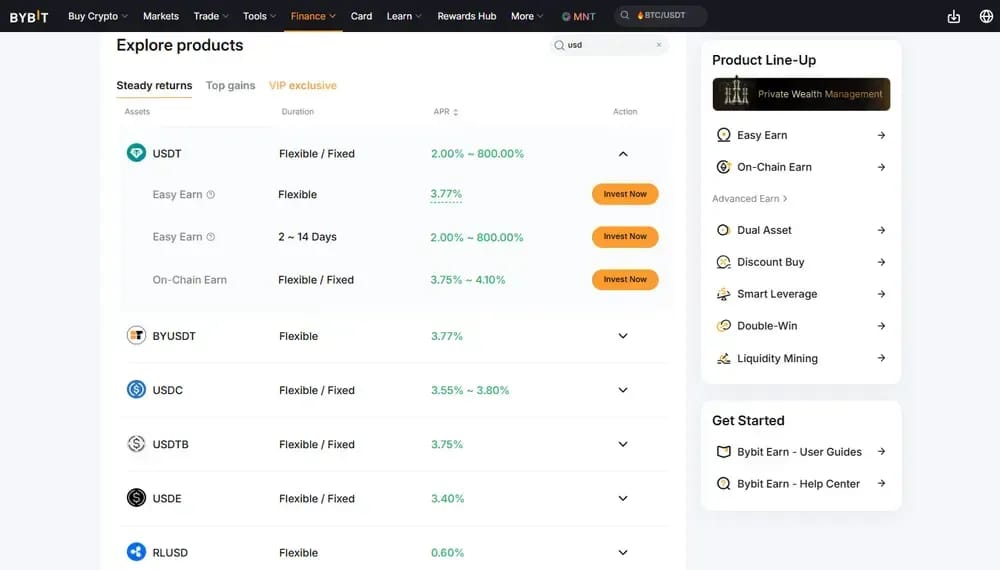

1. Bybit

Bybit is our top overall pick because it combines strong stablecoin APRs, simple redemption, and centralized-exchange convenience without forcing users into complex DeFi routing. The standout stablecoin offers are USDT Flexible at 3.77% APR and USDC Flexible at 3.80% APR, with limited-time USDT promotions reaching much higher tiers.

The platform works best for users who want idle USDT or USDC earning from the same exchange account they already use for spot, futures, and fiat ramps. Easy Earn is positioned as a beginner-friendly product, and flexible plans can be redeemed anytime, making it practical for active portfolio cash management.

Bybit also scores well on reserve transparency. Its Proof of Reserves framework lets users compare wallet assets against user liabilities, while the March 2026 PoR report covered Proof of Liabilities, Proof of Ownership, reserve calculation, and assessment procedures. That makes it our best blend of yield, usability, and visible backing.

Pros

- Strong USDT and USDC flexible stablecoin APRs.

- Simple experience for non-DeFi yield seekers.

- Proof of Reserves improves custody transparency.

- Flexible products suit active cash management.

Cons

- Promotional APRs are capped and temporary.

- Custodial platform risk remains unavoidable.

- Regional availability can restrict certain offers.

2. Aave

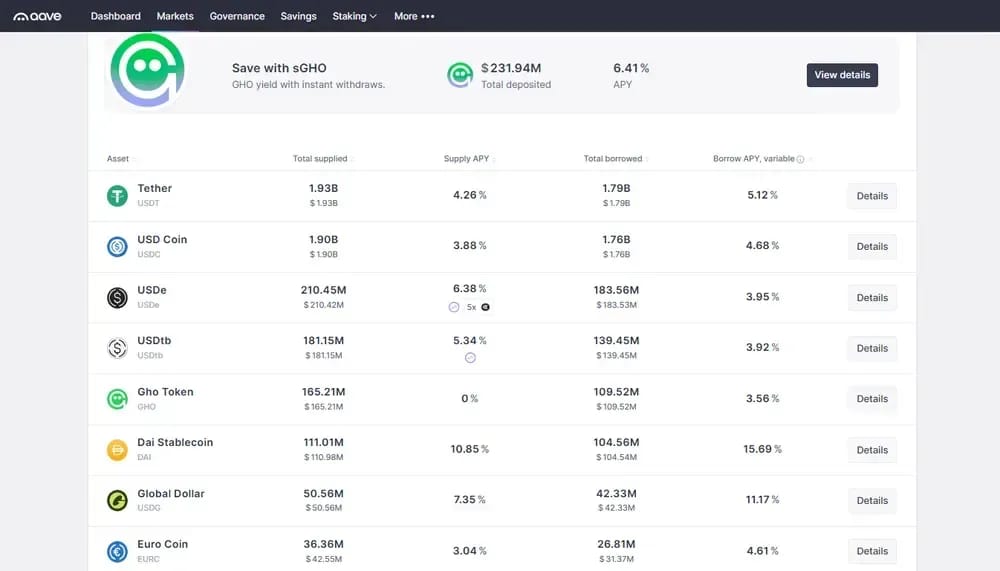

Aave remains the top ranked DeFi choice for stablecoin lenders who want transparent, non-custodial money-market exposure. USDC on Aave V3 Ethereum showed 3.70% APY with a 30-day average of 4.41% and about $145 million TVL on DeFiLlama, making it a benchmark onchain lending venue.

The recent rsETH/Kelp-related stress is important to mention, not ignore. On April 18, 2026, Aave’s Protocol Guardian froze rsETH and wrsETH reserves across multiple V3 deployments, set LTV to zero, and later froze selected WETH markets to contain contagion into other reserves, including stablecoins.

Despite that incident, Aave still earns its ranking because its response was upfront, governance-driven, and visible onchain. It is open-source, non-custodial, deployed across permissionless blockchains, and built around variable lending rates rather than opaque exchange campaigns, which suits users comfortable managing smart-contract and liquidity risk.

Pros

- Leading non-custodial stablecoin lending market.

- Transparent rates, liquidity, and utilization data.

- Governance response is visible and auditable.

- Strong fit for experienced DeFi users.

Cons

- Smart-contract and oracle risk still apply.

- Liquidity stress can delay withdrawals.

- APYs fluctuate with borrower demand.

3. Binance

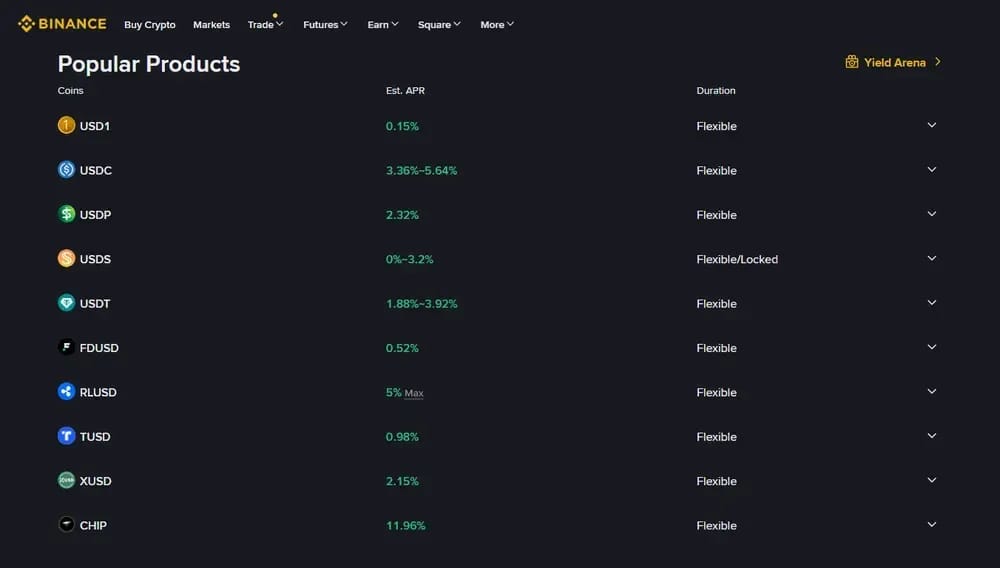

Binance is the strongest centralized-exchange alternative for users who want stablecoin yield inside a massive global platform. Simple Earn supports flexible and locked products, with flexible subscriptions earning every minute and locked products distributing daily rewards. For 2026, Binance has run stablecoin campaigns with headline APRs up to 8% and 30%.

The main appeal is product depth. Binance Simple Earn is principal-protected in token amount, supports flexible redemptions, and calculates Flexible Product rewards through Real-Time APR plus possible Bonus Tiered APR. That setup is useful for users who want stablecoin yield without touching wallets, bridges, or DeFi approvals.

Binance also has an established Proof of Reserves page stating that user account balances are fully backed 1:1, plus additional reserves. We would rank it behind Bybit for this list because many high APRs are campaign-based, but it remains a top CeFi choice for liquidity, accessibility, and product range.

Pros

- Broadest centralized earn product ecosystem.

- Flexible rewards accrue directly every minute.

- Large exchange liquidity and fiat access.

- Proof of Reserves supports custody transparency.

Cons

- Best APRs often depend on campaigns.

- Regional restrictions can affect availability.

- Users retain centralized custody exposure.

4. Ethena

Ethena is another great pick for users who specifically want crypto-native stablecoin yield rather than standard USDC or USDT lending. Its USDe synthetic dollar is built around delta-hedged crypto assets and liquid stables, while sUSDe is the yield-accruing savings asset for users who stake USDe.

The current yield is competitive but no longer the extreme number associated with earlier Ethena cycles. DeFiLlama shows sUSDe with 5.37% APY, a 30-day average of 4.06%, and roughly $2.14 billion TVL, while Ethena’s protocol page shows a similar average APY around 5.34%.

We like Ethena for sophisticated users who understand basis trades, funding-rate compression, and exchange counterparty exposure. Yield comes from sources such as funding and basis spreads, rewards on liquid stable backing assets, and staked ETH rewards, so returns can change sharply when market structure turns less favorable.

Pros

- Strong sUSDe APY versus many stablecoin markets.

- Large TVL and broad DeFi integrations.

- Yield accrues through the sUSDe token.

- Distinct crypto-native dollar yield model.

Cons

- More complex than fiat-backed stablecoins.

- Funding-rate dependence can compress returns.

- Counterparty and hedging risks require diligence.

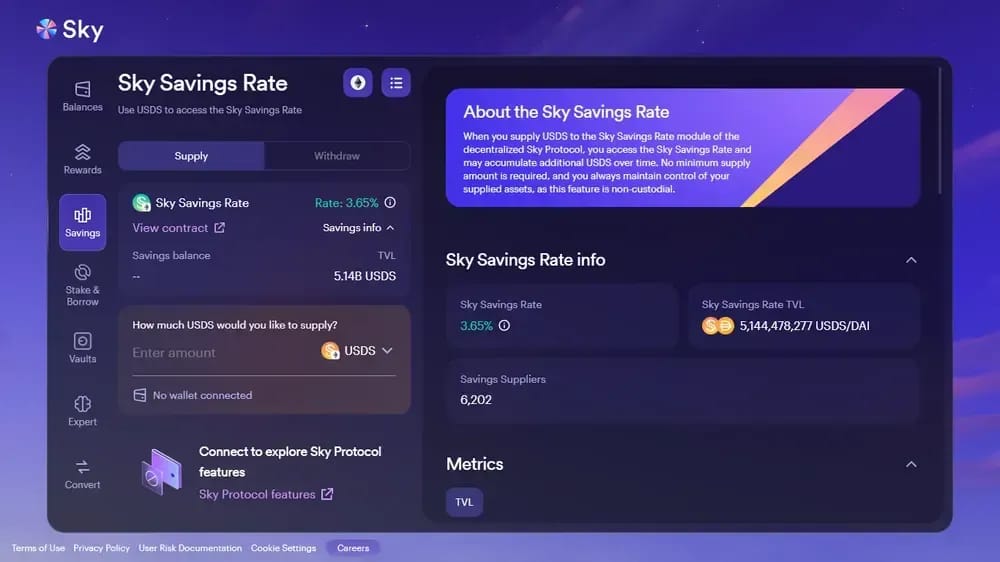

5. Sky Money

Sky is a great decentralized protocol for users who want a clean, protocol-native savings experience around USDS rather than a third-party exchange account. Its flagship sUSDS product currently shows a 3.75% APY, with a reported total sUSDS supply of 6.23 billion and instant-liquidity positioning.

The broader Sky.money interface also includes stablecoin vault strategies. Current displayed options include USDT Savings at 5.19% APY, USDS Risk Capital at 4.00%, and USDS Flagship at 4.76%, though those vault returns are strategy-driven and variable rather than simply governance-set savings rates.

Sky works best for users who value predictability, non-custodial access, and Maker/Sky ecosystem depth. The 1:1 USDC-to-USDS conversion with zero fees or slippage adds convenience, but U.S. availability restrictions and governance-set rate changes need to be checked before moving serious capital.

Pros

- Simple sUSDS savings-rate structure.

- Large sUSDS supply signals deep adoption.

- USDC-to-USDS conversion is friction-light.

- Multiple vault choices for stablecoin users.

Cons

- Current sUSDS APY trails top alternatives.

- Some products unavailable in the United States.

- Governance can change rates over time.

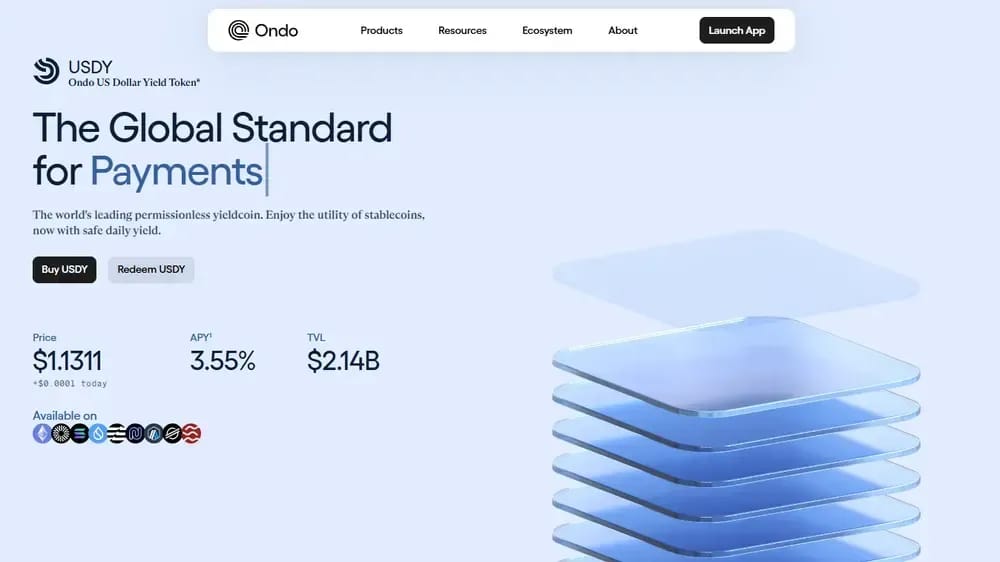

6. Ondo

Ondo is excellent for users who want stablecoin-like yield backed by tokenized real-world assets rather than DeFi borrowing demand. USDY is Ondo’s core yield-bearing dollar asset, and its APY is set monthly in accordance with USDY governing documents.

DeFiLlama currently shows USDY on Mantle at 3.55% APY with a 30-day average of 3.55% and about $29.43 million TVL. Other chain deployments, including Stellar and Solana, show similar 3.55% current APY snapshots, making Ondo more consistent than opportunistic.

We see Ondo as a conservative RWA allocation rather than a maximum-yield play. USDY’s circulating supply and market capitalization are substantial on DeFiLlama, but users should understand transfer restrictions, jurisdictional limits, and the difference between a yield-bearing token price and a traditional redeemable stablecoin balance.

Pros

- Tokenized Treasury exposure with stable yield.

- Monthly APY setting adds rate clarity.

- Multi-chain USDY availability improves access.

- Strong fit for RWA-focused portfolios.

Cons

- Lower APY than higher-risk DeFi options.

- Transfer and jurisdiction limits may apply.

- Not identical to standard USDC or USDT.

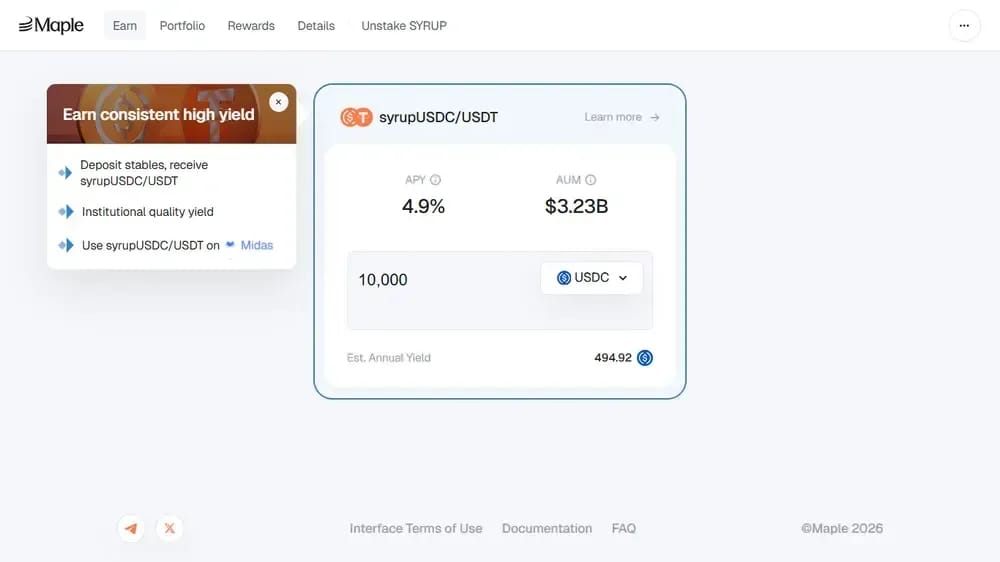

7. Maple

Maple is our top pick for users who want stablecoin yield sourced from institutional onchain credit rather than retail exchange promotions. Its syrupUSDC product gives USDC depositors exposure to overcollateralized institutional lending, and Maple presents syrupUSDC/USDT as liquid yielding dollar assets with weighted APY around 4.8%.

DeFiLlama’s Maple syrupUSDC pool shows 4.95% APY, a 30-day average of 4.53%, and about $2.67 billion TVL, placing it among the largest stablecoin yield venues in this list. That scale is meaningful for users comparing yield depth, not just headline percentages.

The tradeoff is credit risk. Maple’s documentation describes yield as primarily generated from fixed-rate, overcollateralized loans to institutional borrowers, supported by liquidity provision and futures basis strategies. We like it for yield-focused users who understand borrower, collateral, and managed-strategy risk.

Pros

- Attractive syrupUSDC yield with large TVL.

- Institutional lending model diversifies yield sources.

- Overcollateralized loans support risk controls.

- Useful alternative to utilization-based DeFi lending.

Cons

- Credit risk differs from pure DeFi lending.

- Strategy complexity requires deeper due diligence.

- Liquidity assumptions can change under stress.

Where Do Stablecoin Yields Come From?

tablecoin yield usually comes from someone else paying to use your capital. On Aave, borrowers pay interest to access liquidity, and supplier APYs adjust with utilization. When borrowing demand rises, supply rates can rise too; when liquidity is abundant, yields usually compress.

Centralized exchanges like Bybit and Binance package yield into Earn products, but the source can vary by product. Some returns come from lending demand, structured campaigns, market-making programs, or exchange-level promotions, which is why headline APRs can change quickly or include capped bonus tiers.

Ethena is different because USDe and sUSDe are tied to a synthetic dollar model. Its yield is linked to crypto-native sources such as derivatives funding, basis spreads, and rewards on backing assets, so returns depend heavily on market structure rather than simple borrower demand.

Sky, Ondo, and Maple sit in another category. Sky’s sUSDS yield comes through the Sky Savings Rate, Ondo’s USDY targets tokenized Treasury-style yield, and Maple’s syrupUSDC/USDT comes from overcollateralized institutional loans. Rembemer, if you don’t know where the yield comes from, you are the yield.

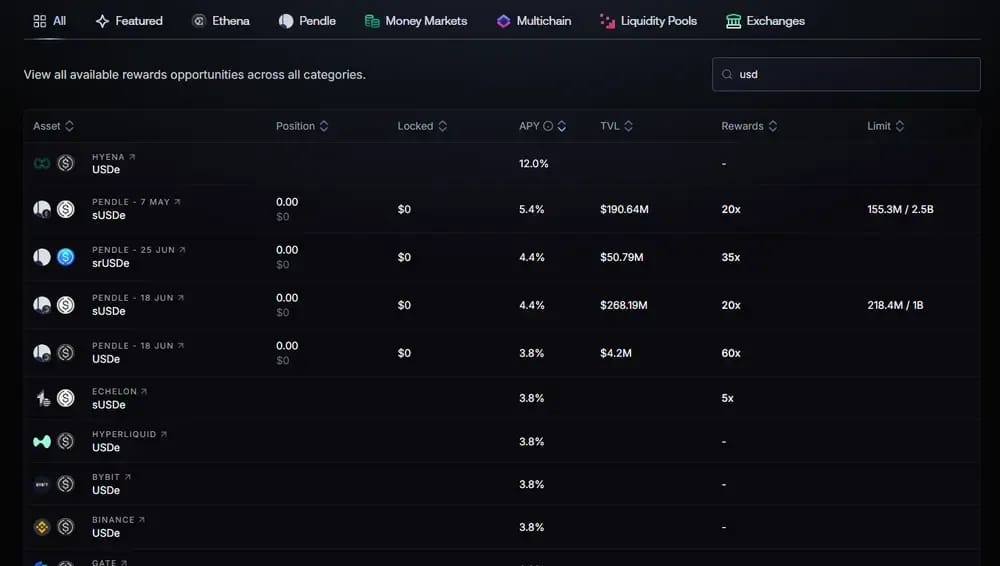

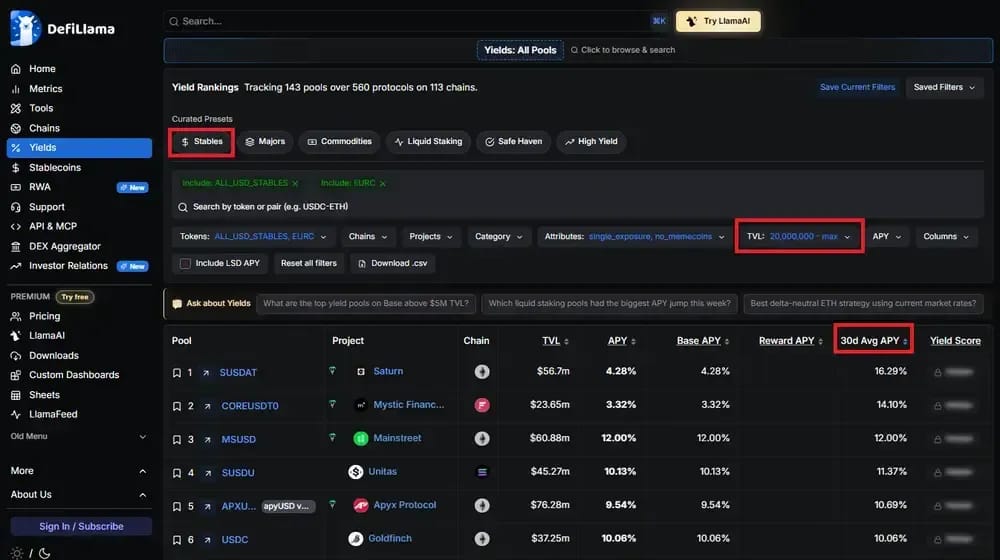

How to Find Stablecoin Pools With High APY

DefiLlama’s Yields dashboard is best for finding short-term, exotic stablecoin strategies, not passive savings replacements. Treat it as a discovery tool, then verify everything manually.

Use this workflow to filter cleaner opportunities:

- Open Yields: Go to DefiLlama’s Yields page, which tracks APY and yield data across DeFi pools, then select the stablecoin preset from the curated filters.

- Filter Tokens: Use the token filter for major stablecoins, including USDC, USDT, USDS, DAI, USDe, or EURC, depending on the risk profile you want to research.

- Set TVL: Raise the minimum TVL filter to $20 million. This removes tiny pools where APY spikes can disappear quickly or exits become difficult.

- Sort Average: Sort by 30d Avg APY, not only current APY. This helps separate sustained yield from temporary incentive bursts or one-day liquidity distortions.

- Check Category: Review the project, chain, category, and pool structure. Lending markets, Pendle pools, vaults, and incentive farms all produce yield differently.

- Inspect Source: Click into each pool and identify the APY source. Prioritize transparent lending, fees, rewards, or strategy yield over unexplained returns.

- Compare Liquidity: Check current TVL against recent APY. A pool with high yield but shallow liquidity may be useful only for smaller, short-duration positions.

- Exit Fast: Use these screens for tactical opportunities. Exotic stablecoin yields can reprice quickly once incentives end, caps fill, or new deposits dilute returns.

Are Stablecoin Interest Rates Taxed?

Yes. Stablecoin interest, lending rewards, and yield payments are usually taxable when earned, but the exact treatment depends on your country, product structure, and whether the return is income or capital.

1. USA

In the United States, the Internal Revenue Service treats digital asset income as taxable, and its guidance explicitly includes stablecoins and rewards from staking or earn programs. Stablecoin yield is generally reported as income when received, based on its fair market value in U.S. dollars.

Selling, swapping, or redeeming stablecoins can also create a reportable transaction, even when the gain is small. The IRS says taxpayers must answer the digital asset question on federal returns and report earned income, so users should track deposits, reward dates, withdrawals, and conversions.

2. UK

In the United Kingdom, HM Revenue & Customs has specific Cryptoassets Manual guidance for DeFi lending and staking. HMRC does not apply one universal rule; it looks at the structure, whether ownership changes, and whether the return is income-like or capital in nature.

If the return has the nature of income, it may fall within Income Tax rules. If the return is capital in nature, HMRC says it may sit outside Income Tax and instead fall within Capital Gains Tax, making recordkeeping especially important for DeFi users.

3. Europe

Across Europe, taxation still depends on each country’s national rules, so Germany, France, Spain, Italy, and the Netherlands can treat crypto yield differently. The European Commission does not set one EU-wide crypto income tax rate for stablecoin interest or DeFi rewards.

What is changing is reporting transparency. The European Commission says DAC8 creates automatic exchange of information on crypto-assets between EU countries, requiring crypto-asset service providers to report relevant user activity to tax authorities across the bloc.

4. Australia

In Australia, the Australian Taxation Office treats crypto rewards from staking and similar arrangements as ordinary income when received. Stablecoin yield is usually valued in Australian dollars at receipt, then added to assessable income, even if the tokens remain on-platform.

A later disposal can also trigger capital gains tax, so the same stablecoin reward may need two records: income value when earned and cost base for future sale, swap, or redemption. The ATO also expects taxpayers to keep detailed crypto transaction records.

5. Rest of the World

Outside the USA, UK, Europe, and Australia, stablecoin yield taxation depends heavily on local law. The safest assumption is that rewards may be taxable, reportable, or both.

Use these checks before relying on any platform:

- Tax Authority: Start with your national tax agency, not exchange blogs, because official guidance decides whether rewards are income, capital gains, or business revenue.

- Income Timing: Check whether tax applies when rewards accrue, when they are paid, or only when withdrawn to your wallet or bank account.

- Disposals: Confirm whether swapping USDT to USDC, redeeming USDY, or exiting sUSDe counts as a taxable disposal in your country.

- Valuation: Record the local-currency value at each reward date, because many tax authorities require fair-market-value reporting when crypto income is received.

- Reporting Rules: Watch the OECD Crypto-Asset Reporting Framework, which supports automatic exchange of crypto transaction information between participating tax authorities.

- Exchange Data: Assume centralized exchanges may share user identity, balances, and transaction activity where local or international reporting rules require it.

- DeFi Records: Save wallet addresses, transaction hashes, pool names, APYs, deposits, withdrawals, and reward claims, especially for Aave, Ethena, Maple, or Pendle strategies.

- Local Advice: For large balances, use a crypto-aware accountant. Stablecoin yield can involve lending, derivatives, tokenized securities, or credit exposure, each taxed differently.

Is Stablecoin Yield Farming Safe?

Stablecoin yield farming can be useful, but it is not risk-free. The main risks are depegs, smart-contract exploits, liquidity crunches, and opaque yield sources.

Review these risks before depositing capital:

- Depegging: Stablecoins can break their peg under stress. USDC briefly depegged in 2023 after Circle disclosed $3.3 billion of SVB exposure.

- Complete Collapse: The TerraUSD collapse showed how algorithmic stablecoin yields can unwind violently when confidence breaks, liquidity exits, and the peg mechanism fails.

- Smart Contracts: DeFi yield depends on smart contracts. Euler Finance lost about $197 million in 2023, proving established lending protocols can still be exploited.

- Custody: CeFi yield platforms require trusting the exchange or issuer. Proof of reserves helps, but it does not remove withdrawal freezes, insolvency, or operational failure.

- Liquidity: High APY pools can become crowded or thin quickly. A strong quoted yield matters less if exits are delayed, capped, or slippage-heavy.

- Incentives: Some returns come from token rewards instead of real demand. Once incentives end, APY can collapse and reward tokens may sell off sharply.

- Strategies: Ethena-style synthetic yield, Pendle pools, and vault strategies can involve basis trades, maturities, or leverage loops. Higher yields usually add moving parts.

- Oracles: Lending protocols rely on accurate price feeds. Bad oracle data can trigger faulty liquidations, distorted collateral values, or unexpected losses during volatility.

- Bridges: Cross-chain stablecoin pools add bridge risk. A bridge exploit can damage wrapped assets even when the original stablecoin remains solvent.

- Complexity: The safest-looking yield is not always safest. If the platform cannot clearly explain who pays the return, assume the hidden risk is higher.

Final Thoughts

Stablecoin yield is most useful when the return source is clear, liquid, and repeatable. Bybit is the easiest starting point, while Aave remains the strongest DeFi benchmark.

Higher APYs usually introduce extra assumptions. Ethena, Ondo, and Maple can all be useful, but their yield sources differ materially from simple exchange earn products.

The safest approach is diversification, position sizing, and regular monitoring. Treat stablecoin yields as variable income products, not guaranteed savings accounts or risk-free cash equivalents.

Our Methodology

We reviewed 30 stablecoin yield platforms across centralized exchanges, DeFi protocols, synthetic dollar products, tokenized Treasury issuers, and institutional credit markets.

Here is how we evaluated each platform:

- Yield Data: We checked current APRs, 30-day averages, TVL, and pool data using platform pages and aggregators like DeFiLlama’s stablecoin yield dashboard.

- Stablecoins: We prioritized major assets including USDT, USDC, USDS, USDe, USDY, and syrupUSDC over obscure tokens with weaker liquidity or unclear redemption paths.

- Liquidity: We compared TVL, market depth, withdrawal terms, and exit flexibility, giving higher scores to products with larger pools and fewer redemption constraints.

- Yield Source: We separated lending demand, exchange earn products, tokenized Treasury yield, synthetic dollar strategies, and institutional credit, since each creates different risks.

- Risk Model: We reviewed custody, smart-contract exposure, collateral design, oracle dependence, issuer transparency, and whether users keep control of funds.

- Transparency: We favored platforms with clear dashboards, public documentation, reserve reporting, verifiable onchain data, or loan-level visibility where applicable.

- Usability: We tested how easily users can deposit, subscribe, redeem, monitor rewards, and understand the product without relying on hidden mechanics.

- Track Record: We considered platform maturity, incident history, integrations, audits, market share, and whether the yield has remained competitive beyond short-term promotional campaigns.