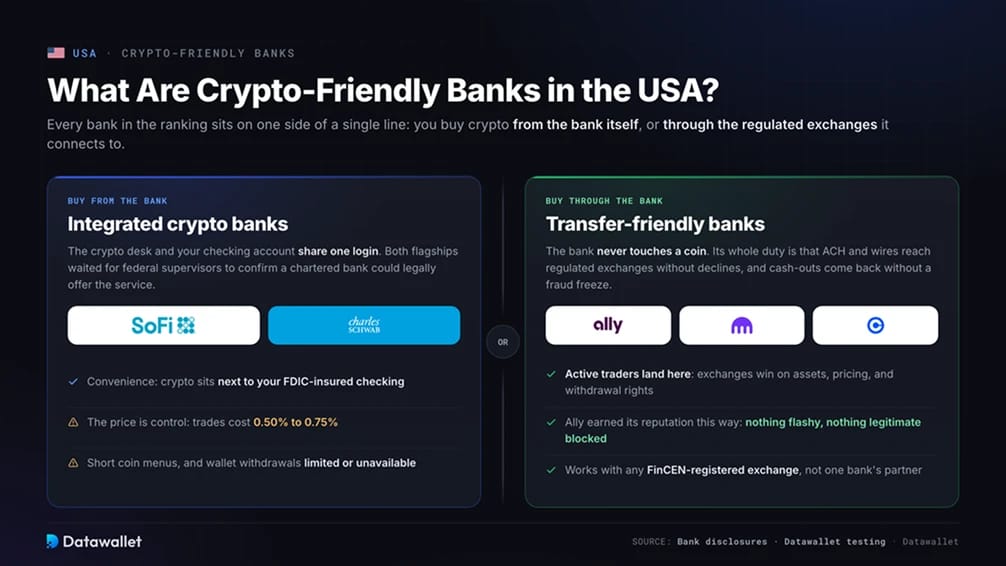

What Are Crypto-Friendly Banks in the USA?

Crypto-friendly carries a wider meaning in the USA than almost anywhere else, because American banks may now sell digital assets under their own charters. Every bank in our ranking sits on one side of a single line, whether you buy crypto from the bank itself or through one of the regulated crypto exchanges in the USA it connects to.

Integrated Crypto Banks

Buying from the bank means the crypto desk and your checking account share one login. SoFi and Schwab run the flagship programs, and both waited for federal supervisors to confirm that a chartered bank could legally offer the service, a question that stayed open until early 2025.

The price of that convenience is control. Trades cost 0.50% to 0.75% at the big names, coin menus stay short compared with any exchange, and withdrawing coins to a wallet you control is limited or unavailable.

Transfer-Friendly Banks

Buying through the bank means the bank never touches a coin. Its whole duty is that ACH transfers, the standard US system for moving money between bank accounts, and outgoing wires reach exchanges like Kraken and Coinbase without declines, and that your cash-outs come back without a fraud freeze.

Active traders mostly land here, since an exchange beats any bank program on asset count, pricing, and withdrawal rights. Ally earned its reputation among crypto users this way, doing nothing flashy and blocking nothing legitimate.

Top Crypto-Friendly Banks in the United States

We rank US banks on how they handle real crypto activity. That covers direct trading where it exists, plus the reliability of ACH and wire transfers to exchanges registered with the Financial Crimes Enforcement Network (FinCEN), the federal agency that supervises money services businesses.

Here is our comparison table of the most crypto-friendly banks in the USA:

1. SoFi

SoFi tops our ranking because it closed the gap between a bank account and an exchange account. SoFi Crypto launched in November 2025, making SoFi the first nationally chartered, FDIC-insured US bank to offer retail crypto trading, and it lets members fund purchases of Bitcoin, Ethereum, Solana, and dozens of other coins straight from checking or savings.

SoFi had offered crypto before, then shut the service in 2023 as a condition of securing its banking license. The relaunch under the Office of the Comptroller of the Currency (OCC), the federal regulator for national banks, signals how far supervisory attitudes have moved.

The trade-off is depth. A dedicated exchange still beats SoFi on coin selection, order types, and pricing for large trades, and crypto held at SoFi carries no FDIC protection because deposit insurance covers dollars only.

2. Chase

Chase earns second place through the most surprising reversal in US banking. In July 2025, JPMorganChase announced a strategic partnership with Coinbase covering Chase credit cards on Coinbase, direct bank-to-wallet account linking, and conversion of Ultimate Rewards points into USDC.

Card funding went live first, and the account linking and rewards features are scheduled to reach customers this year. For the roughly 80 million people who bank with Chase, that removes most of the friction that used to surround Coinbase deposits.

Credit card purchases of crypto can fall under cash advance terms, which add fees and immediate interest, so we would still fund with a checking account link or ACH. The partnership is also Coinbase-specific, and Chase has not extended the same treatment to other exchanges.

3. Charles Schwab

Schwab launched Schwab Crypto this May, giving retail clients direct spot trading in Bitcoin and Ethereum at 0.75% per trade. Charles Schwab Premier Bank acts as custodian, and Paxos handles execution.

For anyone who already keeps a brokerage or bank account at Schwab, the draw is seeing crypto next to stocks and funds in one view, backed by an institution holding trillions in client assets.

Only two coins are supported, clients cannot deposit or withdraw crypto yet, and residents of New York and Louisiana are excluded. Schwab says more assets and transfers will follow, without a firm date.

4. Revolut

Revolut remains the strongest fintech option for people who want crypto and everyday spending in one app. US customers get in-app trading across a wide coin list, and Revolut X adds an exchange-style interface with advanced order types and lower trading fees.

Banking services in the US are provided through Lead Bank, a member of the Federal Deposit Insurance Corporation (FDIC), so the dollar side of the account carries standard deposit insurance while the crypto side does not.

The main weakness is custody freedom. Only select coins can be withdrawn to an external wallet, so most holdings stay locked inside Revolut, and trading costs in the main app run higher than at major exchanges.

5. Ally Bank

Ally is the bank we point to when someone asks for a plain checking account that never fights their exchange transfers. Ally offers no crypto trading of its own. ACH and wire transfers to FinCEN-registered exchanges clear without the merchant blocks that plague many large banks.

The detail to plan around is the new-customer cap. External transfers are limited to $25,000 in total during the first 90 days of the account, so anyone planning a large first deposit to an exchange should open the account well before they need it.

Ally Invest also carries spot Bitcoin exchange-traded funds (ETFs) for anyone who wants price exposure inside a brokerage account instead of holding coins directly.

6. Cash App

Cash App goes deep on one asset instead of covering many. It supports Bitcoin purchases from $1, withdrawals to wallets you control, and instant payments over the Lightning Network, Bitcoin's fast payment layer. This February, it cut Bitcoin purchase fees to zero or near zero and raised withdrawal limits for eligible users.

Cash App is a financial platform rather than a chartered bank, with banking services supplied by partner institutions and its debit card issued by Sutton Bank, Member FDIC. Some Bitcoin features are unavailable to New York residents.

If you only care about Bitcoin, this is the most complete package on the list. If you want any other asset, you will need an exchange alongside it.

7. Fifth Third Bank

Fifth Third is the regional bank we watch most closely. It has stood up a dedicated crypto working group, taken digital asset strategy to board level, and told analysts it wants to provide reserve accounts and payment services to stablecoin and crypto infrastructure firms, having already worked with companies like Stripe and Fireblocks.

For a retail customer today, Fifth Third is a transfer-friendly choice rather than a crypto product. Standard bank transfers to major regulated exchanges work, and the bank's public research treats stablecoins as core payments infrastructure rather than a threat.

We rank it mid-table because intent is not yet product, and its crypto credentials remain a bet on direction until something ships.

8. Customers Bank

Customers Bank serves the industry side of crypto. Its Customers Bank Instant Token (CBIT) network lets exchanges, stablecoin issuers, and trading firms settle US dollar payments between each other around the clock, which made it one of the few banks crypto companies could rely on after 2023.

In August 2024 the Federal Reserve placed the bank under a written agreement over deficiencies in its digital asset risk management and anti-money laundering (AML) controls, the checks banks run to stop criminal funds. The bank has continued operating CBIT while addressing those findings.

For an individual funding a Coinbase account, Customers Bank is the wrong tool. For a crypto business that needs 24/7 dollar settlement, it is one of very few options.

Non Crypto-Friendly Banks in the USA

The blocklist got shorter this year, but it did not disappear. The remaining friction sits almost entirely on the credit card side, where issuers either decline crypto transactions outright or price them as cash advances.

- Capital One: Does not permit credit card purchases of crypto and has a long record of declining ACH transfers to exchanges under fraud rules. We treat it as the least reliable major bank for exchange funding.

- Bank of America: Its card agreements class crypto as a cash-like transaction, which triggers cash advance fees and immediate interest. Standard bank transfers to regulated exchanges usually work, but cards are a poor funding method here.

- Wells Fargo: Blocks credit card transactions at merchants that primarily sell crypto. Retail customers can still fund licensed exchanges by ACH or wire, and affluent clients get access to Bitcoin fund products through the advisory arm.

If a bank prices crypto like a cash advance or its processors warn about crypto merchants, keep your credit cards out of it and fund exchanges by bank transfer instead.

Why Do US Banks Block Some Crypto Payments?

Banks block crypto payments when their risk systems score the transaction as likely fraud, likely scam, or hard to reverse. A large share of payment scams end with the victim sending money to a crypto platform, and once the transfer settles, recovery is nearly impossible, so banks intervene before the money leaves.

AML obligations add another filter. Banks must monitor where customer funds go, and a payment to an unregistered offshore platform carries far more compliance risk than one to a FinCEN-registered exchange. That is why transfers to Kraken, Coinbase, or Gemini clear far more often than transfers to obscure venues.

Card networks add friction of their own. Crypto purchases carry their own merchant category code, which lets an issuer decline or reprice every transaction in the category with one rule. That single switch explains why a bank can block your debit card at an exchange while happily processing your ACH transfer to the same company.

What Changed for US Crypto Banking This Year?

A cluster of policy moves rebuilt the ground under this category, and they explain why banks that shunned crypto for a decade now compete in it.

- The GENIUS Act became law: Signed on July 18, 2025, the GENIUS Act created the first federal framework for payment stablecoins, requiring dollar-for-dollar reserves and licensed issuers. It gave banks a legal basis to hold stablecoin reserves, custody the assets, and issue tokenized deposits.

- The OCC cleared bank crypto activity: Interpretive Letters 1183 and 1184 confirmed that national banks may custody crypto, buy and sell it for customers, and use outside providers, and they scrapped the old rule that banks needed supervisory sign-off first. SoFi and Schwab both launched under this framework.

- A fair banking order targeted debanking: An August 2025 executive order directed regulators to stop using reputational risk as grounds for cutting off customers, a practice crypto firms argued was used to freeze the industry out of banking.

Wall Street responded fast. Beyond SoFi and Schwab, Morgan Stanley's E*Trade completed its rollout of spot Bitcoin, Ethereum, and Solana trading this July at 0.50% per trade, and Citi is preparing an institutional crypto custody service while several majors explore stablecoins.

The consumer gimmicks went the other way. Quontic, the first FDIC-insured bank to offer a Bitcoin rewards debit card, now markets a cash back version of that account instead. The market has moved past novelty perks toward direct trading and settlement infrastructure.

What is the Safest Crypto Exchange in the USA?

Coinbase is our pick for the safest exchange to pair with a US bank account. It is run by a public company listed on Nasdaq, so its finances and customer asset holdings appear in audited filings with the SEC, a level of disclosure no private US exchange matches.

Custody sits under banking-style supervision. Coinbase Custody Trust Company is a limited purpose trust company chartered by the New York State Department of Financial Services, which subjects it to capital, AML, and examination requirements, and the platform keeps roughly 98% of customer assets in offline cold storage.

It is also the exchange US banks integrate with most deeply. The Chase partnership wires the largest US bank directly into Coinbase, so deposits from major banks clear risk checks with fewer holds than payments to lightly regulated venues.

Final Thoughts

Our advice for most US users is a two-account setup. Hold a bank with a direct crypto product or a proven transfer record as your main account, keep a second transfer-friendly account as backup, and do your serious trading on a FinCEN-registered exchange.

Fund exchanges by ACH or wire rather than cards, send a small test transfer to any new platform, and cash out to the same account you deposited from so both sides can verify the money trail.

The direction of travel finally favors you. With national banks now selling crypto directly and regulators barred from leaning on banks to drop crypto customers, the era of guessing whether your deposit will bounce is ending.

.webp)