BitMine (BMNR) Explained: Tom Lee's $60K Ethereum Thesis

Summary: BitMine Immersion Technologies (NYSE: BMNR) is the world's largest corporate holder of Ethereum, with 4.8 million ETH (~$10.2 billion) as of April 2026.

Chairman Tom Lee sees ETH reaching $7,000-$9,000 in 2026, with a bull case of $60,000+ as Ethereum becomes the settlement layer for global finance.

This article breaks down BitMine's treasury, the technical pillars of Lee's Ethereum thesis, his price targets, and how BMNR's ETH stack compares to Strategy's Bitcoin position.

What is BitMine Immersion Technologies?

BitMine started as a US-based Bitcoin mining operation but pivoted in mid-2025 to become an Ethereum treasury company. The shift began when Tom Lee was appointed Chairman in June 2025, alongside a $250 million private placement to seed the new strategy.

BitMine's stated goal is the "Alchemy of 5%": accumulating 5% of all circulating ETH and turning it into a productive, staked balance sheet. The company has reached 3.98% of supply in just nine months, putting it nearly 80% of the way there.

BMNR uplisted to the NYSE from NYSE American on April 9, 2026, with backing from Peter Thiel's Founders Fund and Cathie Wood's ARK Invest. It is now the second-largest crypto treasury company globally, behind only Strategy.

BitMine's Ethereum Treasury Holdings

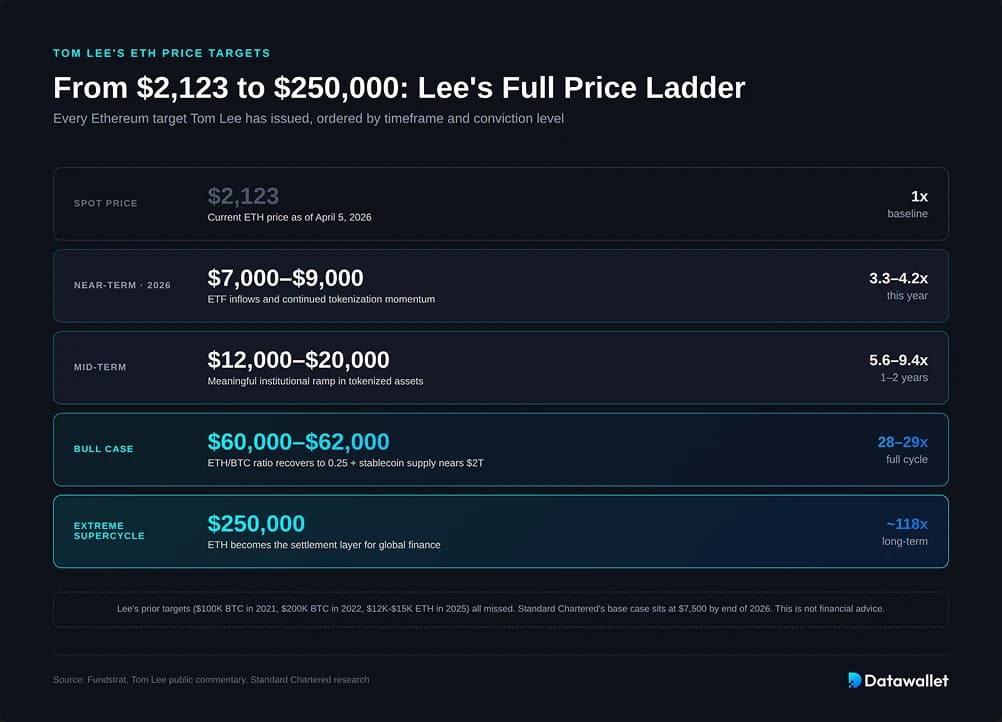

As of April 5, 2026, BitMine holds 4,803,334 ETH, around 3.98% of Ethereum's 120.7 million circulating supply. At $2,123 per ETH, the position is worth roughly $10.2 billion.

The full balance sheet:

- 4,803,334 ETH (~$10.2 billion at $2,123)

- 198 BTC (legacy holdings from the mining business)

- $864 million in cash

- $200 million stake in Beast Industries

- $92 million stake in Eightco Holdings (ORBS), giving BMNR indirect exposure to OpenAI

- Combined total: $11.4 billion

BitMine has been the most aggressive corporate buyer of ETH through the recent drawdown, accumulating 71,252 ETH in a single week in early April 2026. Lee has framed the buying as a bet that Ethereum is in "the final stages of the mini-crypto winter." For live tracking, see our Ethereum Treasury Tracker.

How BitMine Funds Its Ethereum Purchases

BitMine runs the same flywheel Michael Saylor pioneered with MSTR: issue equity at a premium to NAV, convert the proceeds into ETH, and grow ETH per share faster than dilution drags it down. The model breaks the moment the premium compresses, which is exactly the risk Kerrisdale Capital flagged in its October 2025 short report. The funding stack works in three steps:

- Seed capital (July 9, 2025): $250M private placement led by MOZAYYX, with Founders Fund, Pantera, FalconX, Kraken, Galaxy Digital, DCG, and Tom Lee personally.

- The main engine: A $24.5 billion ATM equity program through Cantor Fitzgerald and ThinkEquity, scaled from $2B to $24.5B in under a month. By late 2025, BMNR had issued 240M+ shares and raised $10B+ in gross proceeds, with ~$14B in unused capacity.

- Strategic block trades: ARK Invest acquired $182M of BMNR in a single July 2025 block, with 100% of net proceeds earmarked for ETH purchases.

MAVAN: BitMine's Staking Engine

What separates BitMine from a passive treasury is MAVAN (Made in America VAlidator Network), the institutional-grade staking platform launched in early April 2026.

Of the 4.8 million ETH BMNR holds, 3,334,637 are already staked through MAVAN, representing $7.1 billion at current prices. That stake currently generates approximately $196 million in annualized staking revenue, with Lee projecting up to $282 million at full deployment using a 2.78% seven-day yield.

MAVAN was originally built for BitMine's own treasury but is now expanding to serve external institutional investors and custodians. The platform makes BitMine the largest single staker of ETH on the network and turns the treasury into a yield-generating asset rather than a passive holding.

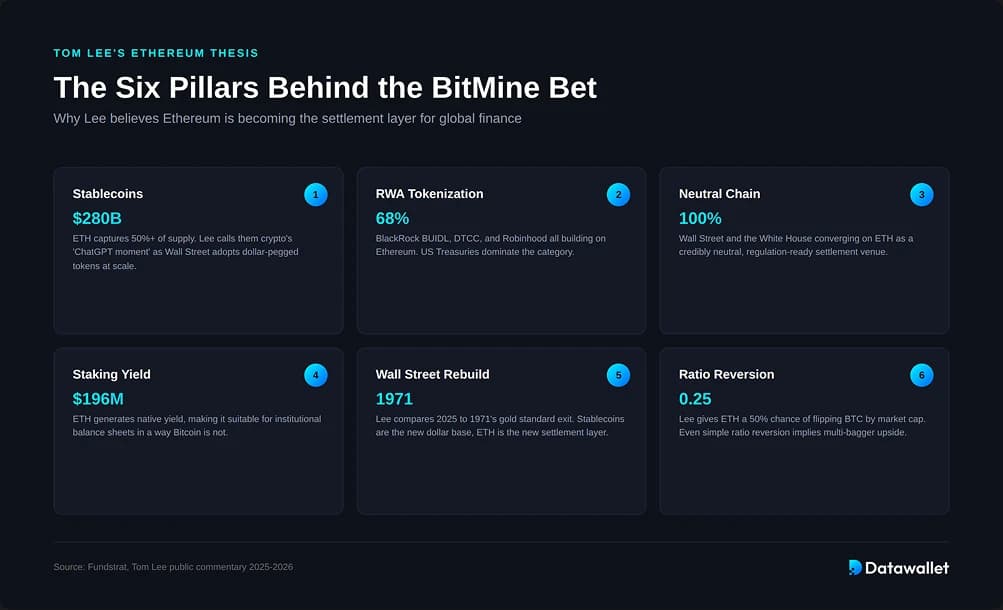

Tom Lee's Ethereum Thesis: The Six Pillars

Lee's case for Ethereum is more structured than the headline price targets suggest. It rests on six interlocking pillars, each backed by data points that have moved meaningfully over the past 18 months.

Pillar 1: Stablecoins as the "ChatGPT Moment"

Lee describes stablecoins as "the ChatGPT moment for crypto", the first product to achieve genuine viral consumer, business, and bank adoption. The stablecoin market sits at roughly $280 billion, with Ethereum capturing more than 50% of total supply through USDT and USDC.

The thesis goes further. Lee references US Treasury projections that the stablecoin market could reach $2 trillion within five years, and points to the GENIUS Act as the regulatory framework that finally pulls Wall Street in. If Ethereum holds its dominant share, that growth flows directly into network demand.

Pillar 2: Real-World Asset Tokenization

Lee's second pillar is the tokenization of traditional financial assets onto public blockchains. Ethereum currently hosts roughly 68% of all tokenized real-world asset value, with US Treasuries leading the category followed by commodities and tokenized credit.

The institutional names matter here. BlackRock's BUIDL fund, Robinhood's tokenized equity push, and the DTCC's planned tokenization of US Treasury infrastructure all run primarily on Ethereum. When the firms that run global settlement pick a chain, that chain accrues value disproportionately.

Pillar 3: Ethereum as Wall Street's "Neutral Chain"

The third pillar is institutional. At Korea Blockchain Week 2025, Lee argued that Wall Street and the White House are converging on Ethereum because it is perceived as a "truly neutral chain" without insider advantage. Institutions want infrastructure they can trust over decades, not chains controlled by foundations with concentrated tokenomics.

Neutrality also extends to uptime. Ethereum has not had a meaningful outage since The Merge, an operational threshold most alternative L1s have failed to clear.

Pillar 4: Staking Yield as Productive Collateral

Unlike Bitcoin, ETH generates native yield through staking. Lee treats this as the structural feature that makes Ethereum suitable for institutional balance sheets in a way Bitcoin is not. A treasury holding 4.8 million ETH and staking 3.3 million produces real cash flow, not just price exposure.

This is central to BitMine's own model. The company tracks "ETH per share" as a key metric, copying Strategy's "BTC Yield" framework but layering staking revenue on top. Productive treasuries can compound where passive ones cannot.

Pillar 5: The 1971 Moment

Lee's macro framing draws a parallel to 1971, when the US dollar went off the gold standard and Wall Street rebuilt itself around fiat. He argues 2025 is the equivalent inflection point, with Wall Street rebuilding around blockchain rails. Stablecoins are the new dollarized base layer, tokenization is the new financial engineering, and Ethereum is the new settlement venue.

The historical parallel drives why Lee thinks this cycle will not look like previous crypto bull runs. Demand will come from institutional flows tied to real activity, not retail speculation tied to sentiment.

Pillar 6: ETH/BTC Ratio Reversion

The final pillar is technical. Lee notes that the ETH/BTC ratio sits well below historical averages, and gives ETH roughly a 50% probability of eventually surpassing BTC in market cap. If the ratio simply reverts to 0.25, well below its 2017 and 2021 highs, that alone implies multi-bagger upside for ETH at any reasonable Bitcoin price.

Tom Lee's Ethereum Price Targets

Lee has issued progressively more aggressive ETH targets over the past 12 months. The full ladder:

- Near-term (2026): $7,000 to $9,000, anchored to ETF inflows and tokenization momentum

- Mid-term: $12,000 to $20,000, requiring meaningful institutional ramp in tokenized assets

- Bull case: $60,000 to $62,000, contingent on the ETH/BTC ratio recovering toward 0.25 and stablecoin supply approaching $2 trillion

- Extreme supercycle: Up to $250,000, implying roughly 100x from current levels

Lee has been clear the higher targets are long-term and depend on sequenced adoption milestones. He has also acknowledged his track record is mixed: prior calls of $100,000 Bitcoin in 2021 and $200,000 in 2022 missed by wide margins, and his 2025 ETH targets of $12,000-$15,000 did not hit.

For context, Standard Chartered's Geoff Kendrick projects $7,500 by end of 2026, scaling to $30,000 by 2029.

BMNR Ethereum Treasury vs MSTR Bitcoin Treasury

The natural comparison for BitMine is Strategy (NASDAQ: MSTR), the company Michael Saylor turned into the original corporate Bitcoin treasury. Both are public-market vehicles built around large, single-asset crypto positions. The mechanics are similar, but the underlying assets behave very differently.

Two things stand out. BitMine has accumulated 4% of ETH supply roughly six times faster than Strategy reached 4% of BTC supply, reflecting both ETH's deeper liquidity and BMNR's more aggressive capital markets activity. Strategy's stack is larger in dollar terms because Bitcoin's market cap is roughly four times Ethereum's, but BMNR is closing the gap on percentage ownership at much higher velocity.

The structural difference is staking. Strategy holds a non-yielding asset and relies entirely on price appreciation and capital markets premiums to generate shareholder value. BitMine holds a yielding asset and earns roughly $196 million a year before any price movement. That cash flow funds further accumulation, creating a flywheel Strategy cannot replicate with Bitcoin.

The trade-off is asset narrative. Bitcoin has a longer track record as a treasury reserve, a cleaner regulatory profile, and the "digital gold" thesis institutions already understand. Ethereum's pitch as productive infrastructure is newer, more dependent on adoption playing out, and exposed to competitive risk from alternative L1s. BMNR's path requires Lee's thesis to broadly play out. MSTR's path mostly requires Bitcoin to keep doing what it has done for 15 years.

Risks to the Thesis

The Ethereum thesis is not uncontested. Mechanism Capital's Andrew Kang has publicly challenged Lee's RWA assumptions, pointing out that despite a 100-1000x increase in tokenized asset value since 2020, Ethereum's transaction fees have remained relatively stagnant. Network upgrades like EIP-4844 and Fusaka have made activity cheaper faster than tokenization has scaled, meaning more usage has not translated into proportional fee revenue.

Other risks worth noting:

- Competition from alternative L1s like Solana, which has captured meaningful stablecoin and DeFi market share

- Regulatory exposure to staking, where the SEC's posture has shifted multiple times

- BMNR equity premium compression, with shares down significantly since September 2025 even as ETH holdings have grown

- Macro and rate sensitivity, since treasury strategies depend on capital markets access to issue equity at premiums to NAV

- ETH/BTC ratio failing to revert, which would cap upside well below Lee's projections

Lee himself has acknowledged the path will not be linear and frames the current period as "the final phase" of the downturn rather than a clean uptrend.

Bottom Line

BitMine has built the largest corporate Ethereum treasury in the world in less than a year, anchored by Tom Lee's conviction that ETH is becoming Wall Street's settlement layer. The 4.8 million ETH stack, the MAVAN staking engine generating ~$196M annually, and the NYSE uplisting all point to a company executing a deliberate institutional play.

Lee's six pillars (stablecoin dominance, RWA tokenization, neutrality, staking yield, the 1971 macro analogy, and ETH/BTC ratio reversion) underpin price targets ranging from $7,000-$9,000 in 2026 to $60,000+ in a full supercycle. Whether those numbers print depends on whether tokenization and stablecoin adoption deliver the institutional flows the thesis requires.

Compared to Strategy's Bitcoin treasury, BitMine offers a faster accumulation pace, productive yield, and a higher-beta bet on a younger thesis. Both vehicles will live or die by whether their underlying asset compounds the way their chairmen believe it will.

Frequently asked questions

.webp)