Best Decentralized Finance Projects (DeFi) for 2026

Decentralized finance has narrowed to a small group of protocols holding most of the capital and producing most of the real revenue. After the late-2025 high and the spring 2026 drawdown, the survivors share live products, paying users, and credible token economics.

The seven below cover the categories that matter most now: onchain perpetuals, lending, liquid staking, spot trading, synthetic dollars, and yield markets. We weighted real usage and revenue over token prices.

Our Top Picks: Best DeFi Projects 2026

- Hyperliquid - On-Chain Perps With Near-CEX Performance

- Aave - The Blue-Chip Lending Standard

- Lido - Liquid Staking That Powers The Rest Of DeFi

- Uniswap - The Default Venue For Token Swaps

- Ethena - A Yield-Bearing Synthetic Dollar

- Morpho - Modular Lending Built For Institutions

- Pendle - Fixed Income And Yield Trading Onchain

Best Platform to Trade DeFi Coins

Gate is one of the widest on-ramps for buying blue-chip and long-tail DeFi tokens before moving them into self-custody, pairing deep liquidity and low spot fees with direct onchain withdrawals.

Available Markets

3,800+ spot and derivatives markets

On-Ramp Methods

Card, SEPA and SWIFT transfers, Apple and Google Pay, and P2P.

Regulation & Licensing

Malta MFSA payment license (EU PSD2), plus Italy, Gibraltar, and Hong Kong.

The 7 Best DeFi Projects in 2026

To build this list we asked a harder question than which token is up: which protocols people keep using when incentives dry up. We compared total value locked, annualized fees and revenue, token value accrual, security history, and behavior under stress, using live dashboards and DefiLlama.

We also tested each product as a user would, funding accounts, depositing, swapping, and withdrawing to self-custody, and noted where access is geo-restricted. Track the wider market through Datawallet's Total Value Locked tool. The table compares all seven.

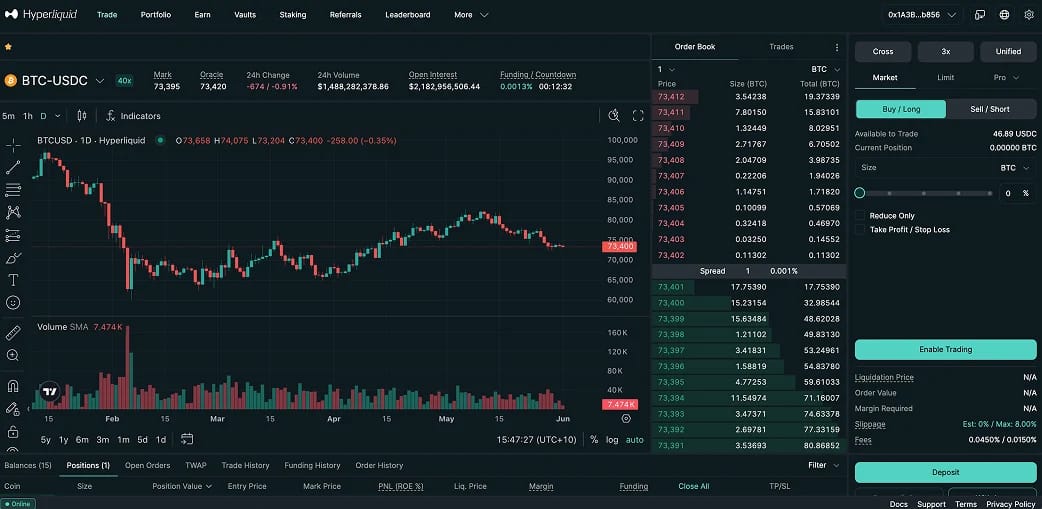

1. Hyperliquid (HYPE)

Hyperliquid is the standout DeFi project of this cycle, and it tops the list because it runs a fully onchain order book at centralized-exchange speed. It is the dominant decentralized perpetuals venue, with around 70% of onchain perp open interest and roughly $180 billion in monthly perp volume, and open interest near $9 billion, per Datawallet's Hyperliquid statistics page.

It is no longer just a crypto perps interface. HyperEVM added Ethereum-compatible smart contracts, and HIP-3 lets builders stake 500,000 HYPE to launch their own markets. Trade.xyz used that to bring tokenized oil, gold, the S&P 500 (licensed by S&P Dow Jones Indices) and a Nasdaq index onchain, lifting HIP-3 open interest near $2.5 billion, where only three of the top ten markets are now crypto. HIP-4 added prediction-style contracts in May 2026, and 97% of all fees buy back HYPE.

When I bridged USDC over, the balance credited almost instantly and the book behaved like a professional venue, not a typical DEX. The trade-offs are real: a validator set still in the mid-20s, liquidation risk on leverage, and a front end that blocks several regions, including the US. If perps are your focus, start with our guide to the best decentralized perpetuals exchanges.

Hyperliquid Highlights:

- Market share: Around 70% of onchain perpetual open interest.

- Volume: Roughly $180B in monthly perp volume.

- Token model: 97% of protocol fees buy back HYPE.

- Builder markets: HIP-3 needs 500,000 HYPE staked to launch a market.

- Real-world perps: Oil, gold, S&P 500 and Nasdaq via Trade.xyz.

- Access note: Front end blocks several regions, including the US.

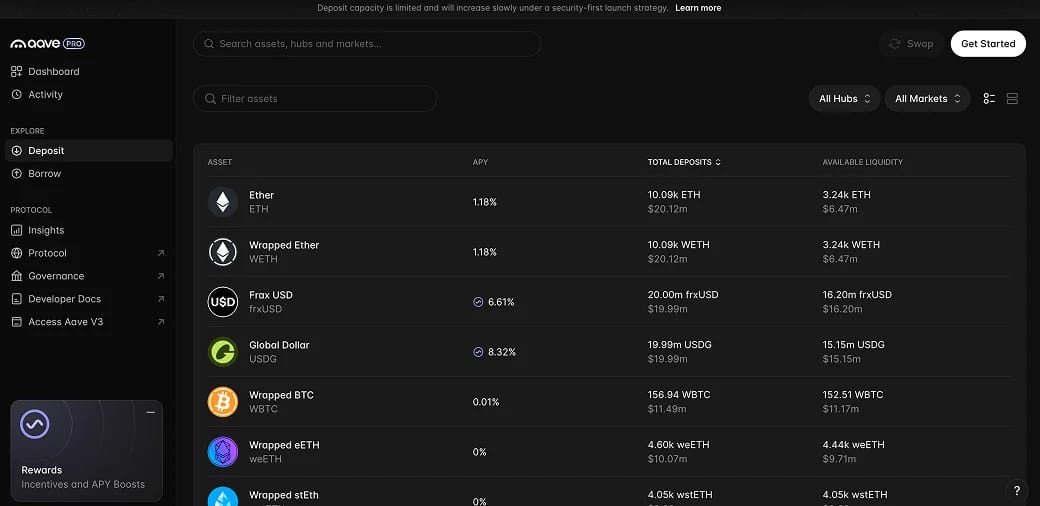

2. Aave (AAVE)

Aave is the reference point for onchain lending and the largest lender by deposits, with total value locked around $14 billion across 21 chains after a spring 2026 drawdown from a $30 billion peak. You supply assets to earn yield or post collateral to borrow, and its Safety Module plus long audit history make it the conservative default. Its overcollateralized stablecoin GHO, near $570 million in supply, and the Aave App savings product extend it past money markets.

The 2026 milestone was Aave V4, launched in March, a modular hub-and-spoke design that keeps liquidity unified while letting specialized markets manage their own risk. Governance also directed all Aave-product revenue to the treasury and set a $50 million-a-year buyback, shifting AAVE toward a value-accruing token.

Aave still carries scars. In April 2026, an exploit of Kelp DAO's rsETH minted roughly $290 million in fake collateral that hit Aave markets and left around $200 million in bad debt the DAO coordinated to absorb. I rate it highly because it handled the incident openly, but blue-chip lending always inherits the risk of the assets it lists.

Aave Highlights:

- Scale: ~$14B TVL across 21 chains, the largest lender.

- Architecture: V4 hub-and-spoke with unified liquidity.

- Stablecoin: GHO, near $570M supply, with an sGHO savings vault.

- Value accrual: All product revenue to treasury, $50M/yr buyback.

- Backstop: Safety Module designed to cover shortfall events.

- Risk note: April 2026 rsETH exploit left ~$200M bad debt.

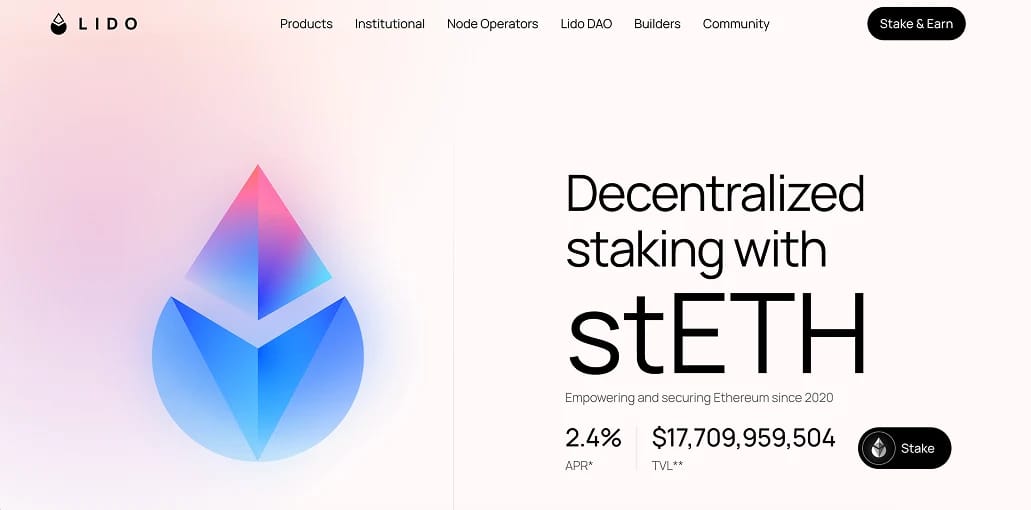

3. Lido (LDO / stETH)

Lido is the backbone of Ethereum liquid staking, with roughly $25 billion staked and about a quarter of all staked ETH. You stake ETH, receive stETH, and hold a liquid token that earns rewards while staying usable as collateral elsewhere, which makes stETH a core building block rather than a niche asset.

Lido V3 launched stVaults in January 2026, a modular framework letting institutions, rollups, and node operators run purpose-built staking while tapping stETH liquidity. Linea and Nansen were early adopters, and Lido targets one million ETH through stVaults by year end. Staking yield has compressed to roughly 2.6% from about 13% a year earlier, and a NEST buyback ties revenue back to LDO.

I have held stETH long enough to see it used as collateral across several protocols without ever unstaking, which is the point. Two caveats: Lido takes a 10% cut of rewards, and its scale, spread across some 600 node operators, still raises validator-concentration questions. Compare it in our guides to the best liquid staking platforms and best Ethereum staking platforms.

Lido Highlights:

- Scale: ~$25B staked, about 24% of all staked ETH.

- Liquid token: stETH, the most integrated DeFi collateral.

- Upgrade: V3 stVaults, targeting 1M ETH by year end.

- Yield: Around 2.6% staking APR in early 2026.

- Fee: 10% on staking rewards.

- Risk note: Validator concentration across ~600 operators.

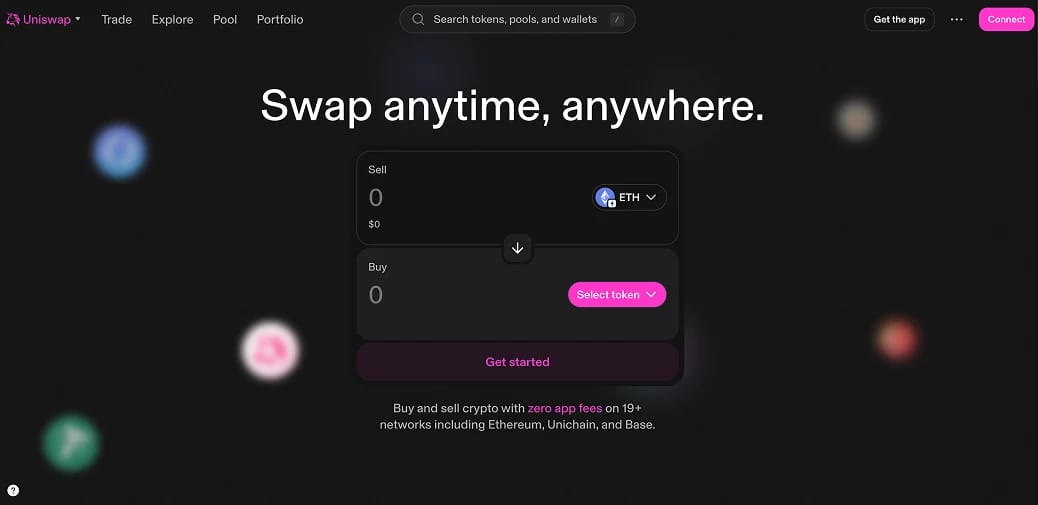

4. Uniswap (UNI)

Uniswap is still the default place to swap tokens onchain, holding the deepest blue-chip liquidity in crypto and clearing over $1 trillion a year, with about $231 billion in the first quarter of 2026 alone. Its automated market maker set the template the whole DEX category copied, and v4 added hooks, which let developers build custom logic like dynamic fees and onchain limit orders into pools.

The turning point came in December 2025 with the UNIfication vote. It switched on protocol fees, permanently burned 100 million UNI worth about $596 million, dropped front-end fees to zero, and feeds protocol and Unichain sequencer revenue into an automated burn. UNI's supply is now tied to how much the protocol gets used.

The first time I swapped through a v4 pool, what stood out was that the interface no longer skimmed a separate fee. The open questions are competitive: Unichain, near $12 billion in monthly volume, must keep winning Layer 2 share, and rival DEXs fight hard on incentives. As infrastructure, Uniswap remains the venue almost everything else builds on top of.

Uniswap Highlights:

- Volume: $1T+ a year, about $231B in Q1 2026.

- Programmability: v4 hooks for custom pool logic.

- Layer 2: Unichain, near $12B monthly, feeds UNI burns.

- Token model: 100M UNI (~$596M) burned, fee switch live.

- Liquidity: Deepest blue-chip markets in DeFi.

- Risk note: Liquidity competition and L2 adoption uncertainty.

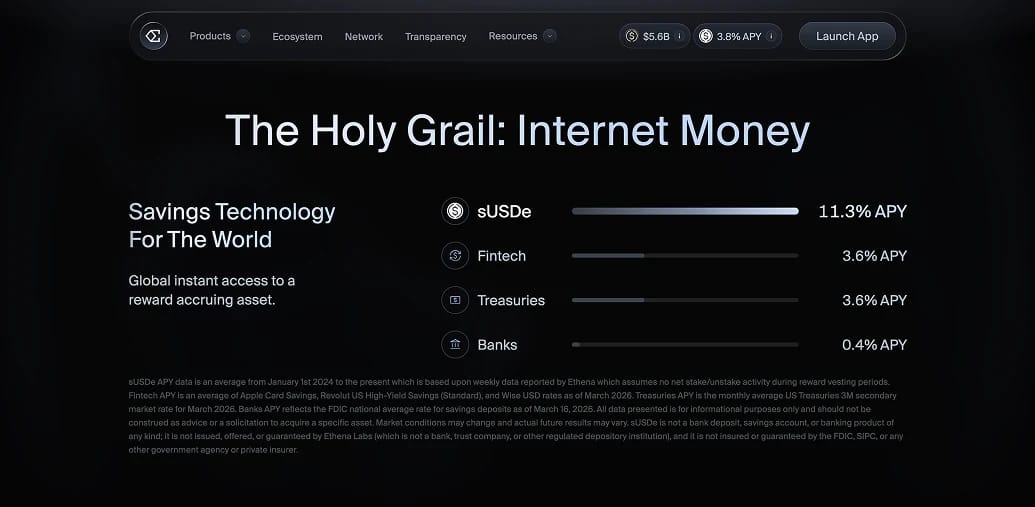

5. Ethena (ENA / USDe)

Ethena issues USDe, a synthetic dollar that holds its peg through a delta-neutral trade rather than a bank account. For every dollar of crypto held long, mostly staked ETH and spot BTC, it opens an equal short on perpetual futures, and the funding plus staking yield passes to holders of the staked version, sUSDe, which has paid a 90-day average near 12% and recently around 9%. That model carried USDe past a $14 billion peak before the October 2025 crash cut supply to roughly $6 billion.

The protocol has pushed into institutional plumbing, with custodians like Anchorage providing weekly proof of reserves, a treasury-backed variant called USDtb, and Converge, a settlement layer for tokenized real-world assets. The ENA token captures revenue through a fee switch to its staked form, sENA, behind a buyback near $890 million.

USDe offers the highest yield here, and that yield is the risk. It depends on perpetual funding staying positive, and the reserve fund cushioning negative-funding periods sits near $60 million, barely 1% of supply. Ethena has already absorbed about $8 billion in redemptions during the October crash, so treat sUSDe as a yield product to size carefully, not a set-and-forget stablecoin.

Ethena Highlights:

- Mechanism: Delta-neutral basis trade across spot and perps.

- Yield: sUSDe near 9% now, about 12% on a 90-day average.

- Scale: USDe near $6B after a $14B+ 2025 peak.

- Institutional push: USDtb, custodian proof of reserves, Converge.

- Value accrual: Fee switch to sENA, buyback near $890M.

- Risk note: Reserve fund near 1% of total supply.

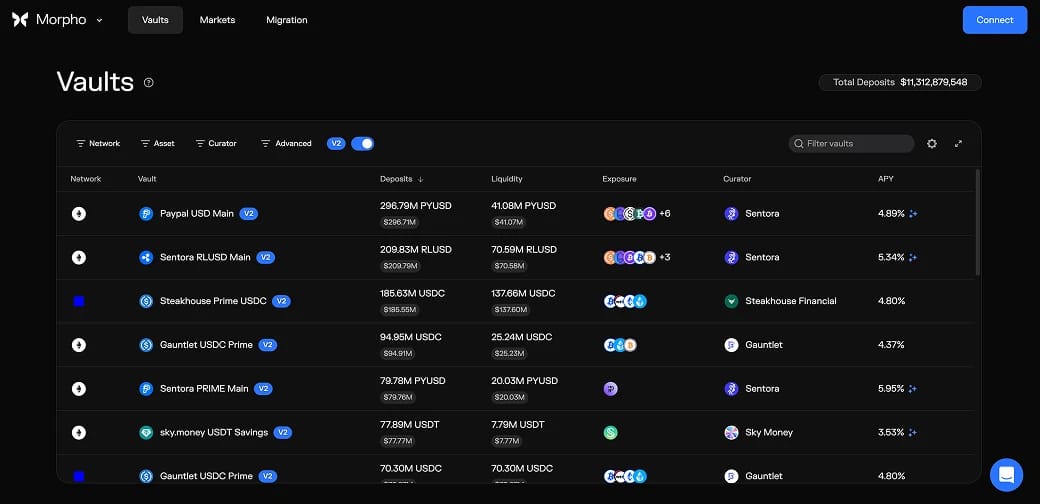

6. Morpho (MORPHO)

Morpho became the second-largest lending protocol, with total value locked near $11 billion in mid-2026 after deposits scaled from $5 billion to $13 billion through 2025, by rethinking what a lending market is. It splits the stack into Morpho Blue, an immutable 650-line primitive for isolated markets anyone can deploy, and Morpho Vaults, where professional curators allocate deposits across them. Instead of one shared pool run by a single DAO, you pick which curator and risk profile to trust.

That design is why institutions arrive through Morpho. It powers Coinbase's crypto-backed loans, now up to $100,000 against SOL as well as BTC and ETH, plus Kraken's DeFi Earn and Ethereum Foundation treasury deposits, while Apollo Global agreed to buy up to 9% of MORPHO, around 90 million tokens, over four years. Morpho V2 added market-driven rates, fixed-term loans, and real-world-asset support.

Depositing into a curated vault felt less like using an app and more like picking a fund manager, since the curator decides where money goes within set limits. The caveats: curator quality varies, loose parameters can still be exploited, and despite roughly $175 million in annualized fees, MORPHO has paid nothing to token holders so far. For lending depth, it now sits alongside Aave.

Morpho Highlights:

- Scale: ~$11B TVL, second only to Aave.

- Architecture: 650-line Morpho Blue plus Vaults curation layer.

- Distribution: Powers Coinbase loans, Kraken Earn, EF treasury.

- Institutional: Apollo buying up to 9% of MORPHO over four years.

- Fees: ~$175M annualized, none paid to holders yet.

- Risk note: Curator dependence and isolated-market exploits.

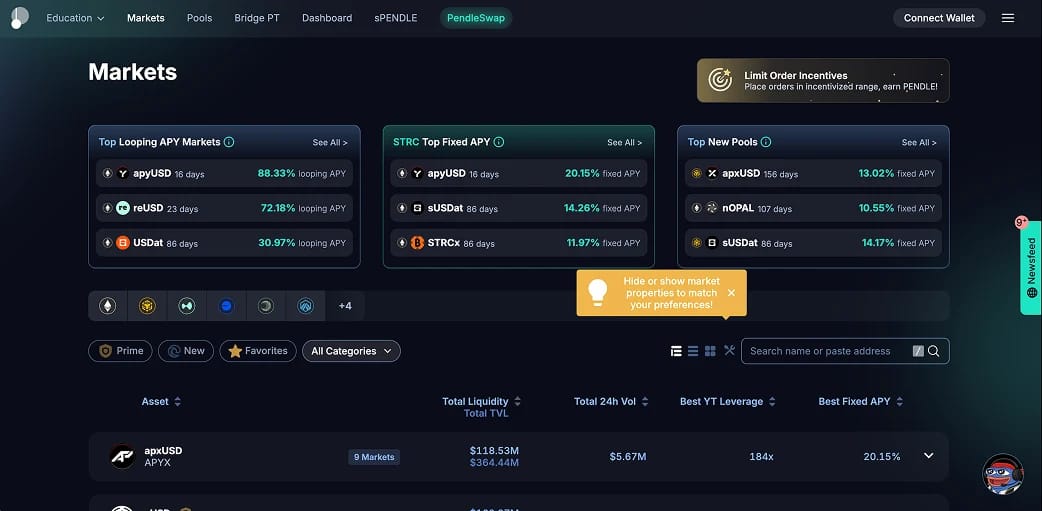

7. Pendle (PENDLE)

Rounding out the list, Pendle is the largest venue for trading yield itself, with total value locked around $5 billion after a roughly $13 billion peak in 2025. It splits a yield-bearing asset into a principal token (PT), which acts like a zero-coupon bond redeemable at maturity, and a yield token (YT), which captures the variable yield until then. One user locks in a fixed rate while another speculates on where rates head, all onchain.

Pendle grew with the staking and restaking waves and now spans more than eight chains, including Solana and TON. Its Boros platform extends into perpetual funding-rate trading, a market worth roughly $150 billion a day, and the sPENDLE upgrade sends about 80% of the protocol's near $40 million in annual revenue into buybacks.

Pendle gives DeFi something it lacked: a real fixed-income market. It is also the most demanding for newcomers, since PT and YT pricing, maturities, and post-expiry behavior take time to learn. PT positions are already accepted as collateral in Aave V4, a strong signal of how embedded the primitive has become.

Pendle Highlights:

- Scale: ~$5B TVL after a ~$13B 2025 peak.

- Mechanics: Splits assets into PT (fixed) and YT (variable).

- Expansion: Boros targets the ~$150B/day funding-rate market.

- Revenue: Near $40M a year, 80% sent to sPENDLE buybacks.

- Reach: Eight-plus chains, including Solana and TON.

- Risk note: Steep learning curve and maturity-date mechanics.

What Is DeFi (Decentralized Finance)?

DeFi refers to financial services that run on public blockchains through smart contracts instead of banks or brokers. Lending, trading, staking, and derivatives all execute as code, so anyone with a self-custody wallet can use them without permission, and balances stay under the user's own keys.

The price of that openness is responsibility. No support desk reverses a mistaken transfer, and no insurance fund stands behind most protocols. The same transparency that lets you verify a contract means a bug can be exploited by anyone who finds it, so security and track record matter more than advertised yield.

The category has consolidated since the last cycle. Total value locked has hovered near the hundred-billion-dollar mark in early 2026, with a handful of protocols holding most of it. Using any of them takes a wallet, some gas, and an on-ramp to acquire assets, where a regulated exchange still fits. See our guide to the best crypto wallets.

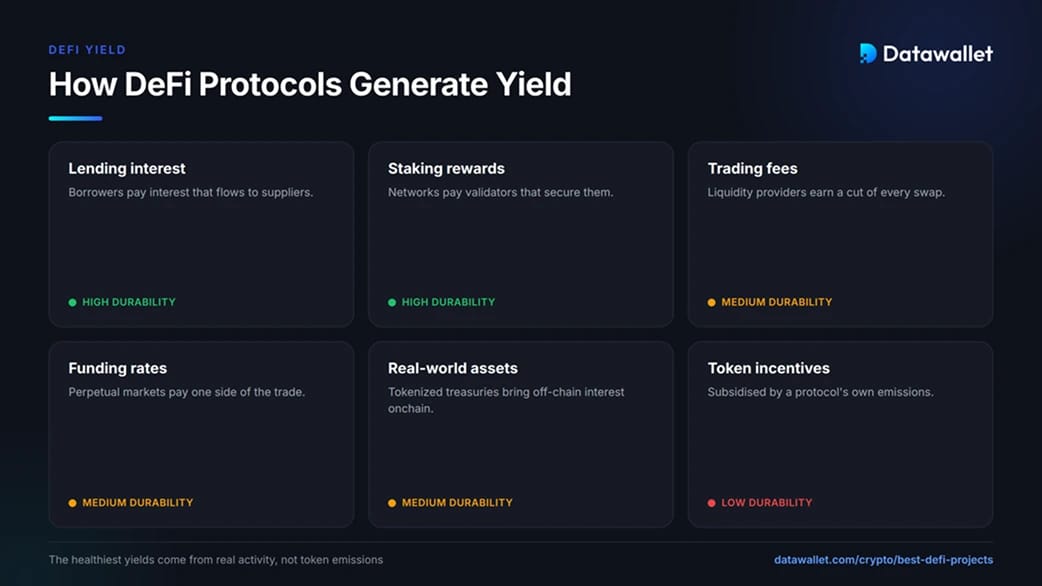

How Do DeFi Protocols Generate Yield?

Every DeFi yield comes from somewhere specific, and the source tells you how durable it is. The healthiest returns are paid by real activity, not token emissions, so the first question for any APY is who funds it.

The main sources of onchain yield:

- Lending interest: Borrowers pay to take loans, and that interest flows to suppliers on protocols like Aave and Morpho.

- Staking rewards: Networks pay validators to secure them, which liquid staking tokens like stETH pass through to holders.

- Trading fees: Liquidity providers on Uniswap earn a cut of every swap, offset by impermanent loss risk.

- Funding rates: Perpetual markets pay one side of the trade, the source behind Ethena's sUSDe and Pendle's Boros.

- Real-world assets: Tokenized treasuries and credit bring off-chain interest onchain, increasingly through curated vaults.

- Token incentives: Protocols sometimes subsidize yield with their own tokens, which inflates APYs temporarily and is the least sustainable source.

When a yield looks far higher than these sources justify, the gap is usually paid in token emissions or hidden risk. Treating an APY as a starting point for questions, not a promise, is the habit that separates careful users from the rest.

How to Start Using DeFi Safely

You do not need to understand every protocol to begin, but a deliberate setup prevents most beginner mistakes. Early on, learn the mechanics with amounts you can afford to lose entirely.

A sensible first run:

- Get a self-custody wallet. Install a reputable wallet, write the recovery phrase on paper, and never type it into a website. That phrase is your only backup.

- Acquire assets on an exchange. Use a regulated platform like Bybit to buy the token and gas you need, then withdraw to your own wallet.

- Start with a blue-chip protocol. Make a small first deposit on an established name like Aave or Lido before touching newer markets or leverage.

- Verify every address. Bookmark official sites, check contract addresses against the project's docs, and ignore links sent in direct messages.

- Size for total loss. Assume any single protocol could fail, and never commit more than you can write off while learning.

The biggest losses I have seen come from social engineering and fake front ends, not protocol bugs. Slowing down at the wallet and approval stage stops the most common attacks.

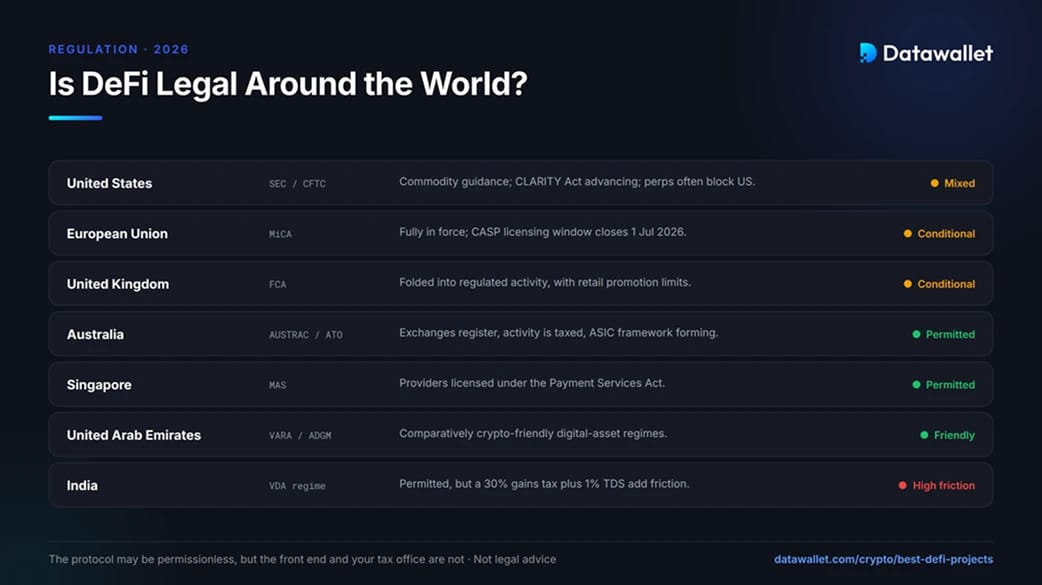

Is DeFi Legal Around the World?

DeFi is generally legal to use in most major markets, but the rules on how it is offered, marketed, and taxed differ sharply by country, and front ends increasingly restrict access by location. The notes below are a general overview, not legal advice, so confirm your position with a local professional.

How major regions are approaching DeFi in 2026:

- United States: A March 2026 SEC and CFTC memorandum moved several major assets toward commodity treatment, and the CLARITY Act advanced out of the Senate Banking Committee. Many perpetuals front ends, including Hyperliquid, still block US users.

- European Union: MiCA is fully in force, with the licensing transition window closing on 1 July 2026. Fully decentralized protocols sit outside its current scope, but front ends and teams marketing to EU users can fall inside it.

- United Kingdom: The FCA is folding crypto into regulated activity and limits how DeFi products are promoted to retail, shaping what UK users can legally be offered.

- Australia: Exchanges register with AUSTRAC, the ATO taxes most DeFi activity as it happens, and ASIC is building a platform framework, so local users carry clear record-keeping duties.

- Singapore: The MAS licenses providers under the Payment Services Act, and front ends serving residents may need authorization even when the protocol does not.

- United Arab Emirates: Dubai's VARA and ADGM run comparatively crypto-friendly regimes, which is why several DeFi teams base operations there.

- India: Use is permitted, but a 30% tax on virtual digital asset gains plus a 1% transaction levy create heavy friction for active users.

For a global user, the protocol may be permissionless while the interface and your tax authority are not. Checking both before you deposit saves trouble later.

Risks of Using DeFi Projects

DeFi rewards carry a different risk set than holding crypto on an exchange. Review these before committing capital to any protocol here.

- Smart-contract failure: A bug or exploit can drain a protocol even when the network works fine, so audits and time in market matter. See our overview of smart contract auditing companies.

- Listed-asset risk: Lending markets inherit the weaknesses of the tokens they accept, as Aave's spring 2026 bad-debt episode showed.

- Liquidation risk: Borrowing and leveraged perps can be liquidated fast in volatile conditions, locking in losses.

- Yield reflexivity: Strategies built on funding rates or looped leverage can unwind quickly when the market turns, breaking pegs.

- Custody mistakes: Self-custody means a lost seed phrase or a malicious approval is irreversible.

- Regulatory and access shifts: Front ends can geoblock your region or delist tokens with little notice.

- Token value accrual: A strong protocol does not guarantee a strong token, since some pass little revenue to holders.

Final Thoughts

The best DeFi projects in 2026 are the ones that kept working after incentives faded. Hyperliquid leads by turning onchain perps into a product that rivals centralized venues, and the rest cover the pillars users actually need: lending via Aave and Morpho, staking via Lido, swaps via Uniswap, dollar yield via Ethena, and a real rates market via Pendle.

None are risk-free, and the highest yields carry the highest fragility. Match the protocol to what you want to do, start small, keep assets in self-custody, and treat every advertised return as a question about where the money comes from.

.webp)