What is the GENIUS Act?

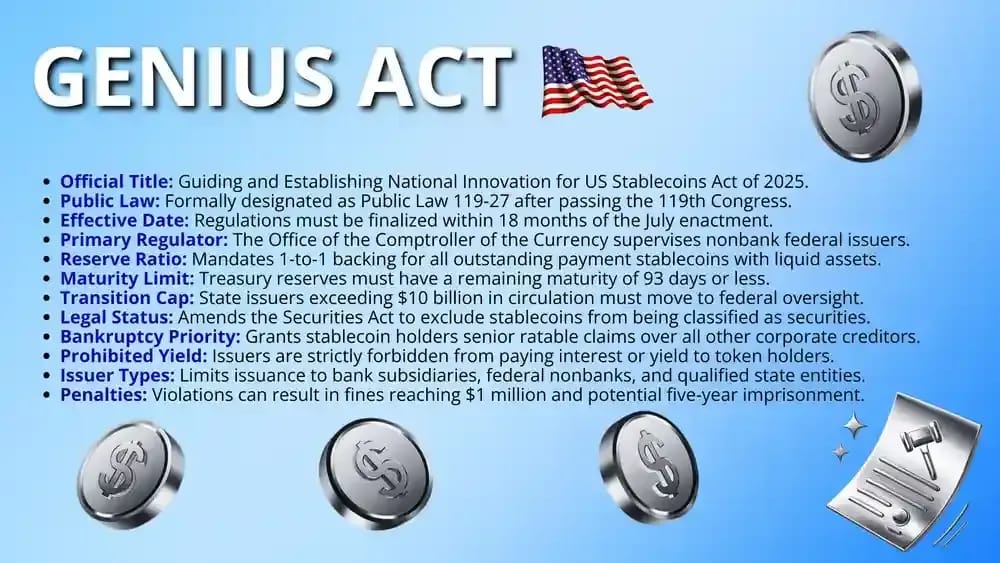

The Guiding and Establishing National Innovation for US Stablecoins Act, known as the GENIUS Act, creates a comprehensive federal framework for payment stablecoins. It establishes strict reserve requirements and clear oversight roles for the Federal Reserve and the Office of the Comptroller.

The law mandates that all issuers maintain 1-to-1 reserves in highly liquid assets like short-term Treasury bills. This structure aims to protect consumers from sudden de-pegging events while providing a legal path for nonbank entities to operate.

Crucially, the legislation clarifies that regulated payment stablecoins are not securities or commodities under existing federal law. This definitive classification provides the legal certainty needed for digital assets to integrate into the traditional United States financial system.

GENIUS Act Legislative Timeline

The GENIUS Act's timeline tracks the quick passage of the bill through the 119th Congress:

- Senate Introduction (05/01/2025): Senator Hagerty introduced the measure, which was immediately placed on the legislative calendar to begin formal floor consideration.

- Cloture Invoked (05/19/2025): The Senate successfully voted 66 to 32 to end debate on the motion to proceed with this critical legislation.

- Substitute Amendment (06/09/2025): A substitute amendment was proposed in the nature of a substitute to refine the regulatory scope of the act.

- Senate Passage (06/17/2025): The Senate passed the final version with an amendment by a bipartisan vote of 68 to 30 for the bill.

- House Approval (07/17/2025): Members of the House of Representatives passed the legislation by a substantial 308 to 122 vote during the morning session.

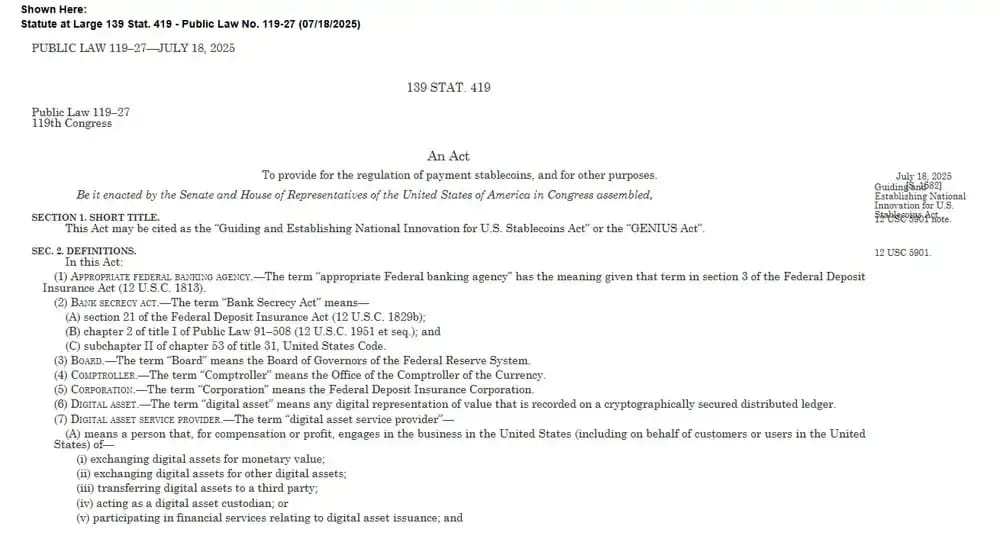

- Presidential Signature (07/18/2025): The President signed the bill into law, officially creating Public Law 119-27 and establishing the new national stablecoin standards.

Key Aspects of the GENIUS Act

The GENIUS Act introduces a dual-track regulatory system that balances state and federal oversight. By defining strict operational standards, the legislation ensures that only compliant entities can issue dollar-denominated stablecoins while protecting the stability of the broader financial ecosystem.

1. Permitted Issuers and the $10 Billion Threshold

The act restricts issuance to "permitted payment stablecoin issuers," which includes bank subsidiaries, nonbank entities approved by the Comptroller, and state-qualified issuers. This ensures that every stablecoin in circulation is tethered to a regulated and supervised financial institution.

A crucial $10 billion cap exists for state-regulated entities, such as those operating under New York’s BitLicense. Once an issuer’s circulation exceeds this $10 billion mark, they must transition to joint federal oversight to mitigate broader systemic risks.

2. Strict Reserve and Liquidity Mandates

Issuers must maintain a 1-to-1 reserve ratio using highly liquid assets to ensure every token can be redeemed for its face value. This prevents the "run on the bank" scenarios seen in previous market collapses.

- Eligible Assets: Reserves are limited to US coins, currency, or Treasury bills with a remaining maturity of 93 days or less.

- Monthly Certifications: CEOs must submit a monthly attestation of reserve accuracy, similar to the accountability standards found in the Sarbanes-Oxley Act.

- Prohibition on Rehypothecation: Issuers cannot pledge or reuse reserves for other investments, ensuring funds stay available for user redemptions at all times.

3. Definitive Legal Classification

This legislation provides historical clarity by amending the Securities Act of 1933 and the Commodity Exchange Act to exclude payment stablecoins from their jurisdiction. This specific exclusion allows tokens like USDC or PYUSD to function primarily as payment tools.

By removing the "security" label, the act ensures that issuers do not have to register every token launch with the SEC. This classification provides the legal certainty required for traditional banks to integrate digital assets into their existing payment infrastructures.

4. Consumer Protection and Bankruptcy Priority

In the event of an issuer’s insolvency, the act grants stablecoin holders senior priority over other creditors. This ensures that the reserves are used to pay back the token holders first before any other debts are settled.

- Priority Claims: Stablecoin holders have a "ratable" claim on the reserves, meaning they are paid out proportionally from the remaining 1-to-1 assets.

- Bankruptcy Speed: The act mandates that courts use their best efforts to begin distributing funds to holders within 14 days of the initial hearing.

- Asset Segregation: Required reserves are excluded from the debtor’s general estate, preventing them from being used to pay off the issuer's corporate legal fees.

How the GENIUS Act Defines Stablecoins

The GENIUS Act provides the first comprehensive statutory definition for "payment stablecoins" in United States history. By distinguishing these digital assets from traditional investment contracts, the law establishes a clear regulatory perimeter that prioritizes functional utility over speculative classification.

Stablecoins Classification: Before vs. After the GENIUS Act

To understand the update in the regulations, the following comparison highlights how the GENIUS framework replaces years of ambiguity with concrete legal categories for dollar-pegged assets:

Which Stablecoins Benefit From The GENIUS Act?

The GENIUS Act identifies specific digital assets that meet strict federal reserve criteria, creating a class of regulated and compliant payment tools.

These leading stablecoins currently align with the new standards:

- USDC (Circle): This asset aligns with federal reserve standards, ensuring its status as a primary settlement tool for major financial institutions.

- PYUSD (PayPal): Leveraged for retail payments, this token thrives under new consumer protection mandates, bolstering trust for everyday electronic commerce transactions.

- USA₮ (Tether): This specific federally regulated version allows the world's largest issuer to enter the American market while following strict guidelines.

- RLUSD (Ripple): Created for institutional liquidity, this stablecoin utilizes the clear legal definitions to facilitate cross-border payments through traditional banking.

- FIDD (Fidelity): The Fidelity Digital Dollar integrates with mainstream investment platforms, benefiting from the explicit exclusion of stablecoins from securities laws.

- USDP (Paxos): As a regulated trust company product, this asset maintains strict 1-to-1 backing, fulfilling the act's transparent monthly reporting requirements.

Conversely, popular assets like the original USDT and algorithmic tokens struggle because their diverse reserves do not meet the new mandates.

Pros and Cons of the GENIUS Act

The GENIUS Act balances institutional innovation with strict oversight. The following table highlights the primary advantages and potential drawbacks of this landmark legislation:

GENIUS Act Impact on Crypto Exchanges

The GENIUS Act requires domestic trading platforms to greatly alter the way they manage their asset listings and liquidity pools. Leading USA crypto exchanges like Coinbase and Kraken must now strictly vet every dollar-pegged token to ensure they are issued by permitted entities.

Platforms such as Gemini are already utilizing this legal clarity to market regulated assets, while non-compliant tokens face aggressive de-listing threats. This mandatory filtering creates a more secure environment for retail users by eliminating the risk of unbacked stablecoin collapses.

For offshore platforms like Binance and Bybit, the legislation restricts their ability to offer foreign stablecoins to US customers without a registration. These global entities must prove technological compliance with American lawful orders to maintain access to US users.

Decentralized protocols such as Uniswap and Aave occupy a unique position as the act provides specific exclusions for distributed ledger software. While the underlying code remains protected, profit-seeking interfaces must still navigate strict service provider definitions to avoid potential penalties.

What Does The GENIUS Act Mean For Investors?

The GENIUS Act ensures that retail investors are no longer exposed to the risks of unbacked or algorithmic stablecoin failures. By mandating audited 100% reserves, the law provides a reliable foundation for those using digital dollars for savings.

Average investors do not need to take immediate legal action, but they should verify that their preferred tokens are issued by permitted entities. Transferring funds into regulated assets like USDC or PYUSD ensures that their capital remains protected.

Final Thoughts

The GENIUS Act represents the initial half of a legislative bridge connecting traditional banking with the growing domestic digital asset market structure.

This landmark stablecoin framework effectively complements the CLARITY Act by removing overlapping jurisdictional friction and providing a clear path for broader institutional adoption.

Legislators have successfully established the essential guardrails required to maintain American financial leadership while ensuring the safety and stability of every dollar-pegged innovation.