Is Hyperliquid Available in the United States?

No. The interface blocks U.S. users at the door. Under its Terms of Use, "Restricted Persons" cover anyone residing, located, or incorporated in the United States, plus U.S. citizens wherever they are. Load the app from a U.S. IP address and you are told your jurisdiction is barred.

What sets Hyperliquid apart from centralized rivals is the mechanism. Binance and Bybit gate access with Know Your Customer (KYC) checks; Hyperliquid runs none. Its operator, Hyperliquid Corp., relies on geofencing plus your contractual promise that you are not a Restricted Person.

A key distinction: Hyperliquid Corp. runs the website-hosted interface, not the blockchain itself. The Layer 1 keeps settling trades no matter who can load the app, and that split sits at the center of every U.S. regulatory fight over it.

Our guide to Hyperliquid's supported and restricted countries lists every blocked jurisdiction.

%20(1).webp)

Why Does Hyperliquid Block US Users?

Risk avoidance. Serving leveraged perpetuals to American retail traders without registration would trigger several U.S. regulatory regimes at once, with steep penalties for getting it wrong. Hyperliquid took the path most offshore venues chose and walled the country off.

The pressures behind that call:

- Derivatives law: The Commodity Futures Trading Commission (CFTC) oversees U.S. crypto futures, and intermediaries facilitating them are generally expected to register with the CFTC and the National Futures Association. A perpetual is a derivative, putting Hyperliquid's core product in the agency's lane.

- Securities exposure: The Securities and Exchange Commission (SEC) can claim jurisdiction wherever a token or trade looks like a security, adding a second federal regulator and registration burden.

- Sanctions: Rules from the Office of Foreign Assets Control reach any platform that might serve blocked persons, which is why the terms separately exclude sanctioned and export-controlled territories.

- No consumer safeguards: A non-custodial, permissionless venue offers none of the segregated-funds rules or recourse U.S. regulators expect from retail platforms.

These concerns have teeth. The CFTC has previously charged operators of decentralized derivatives protocols for failing to register as designated contract markets or futures commission merchants, proving "decentralized" is no automatic shield. The geoblock keeps Hyperliquid out of that line of fire while the rules get rewritten.

The CFTC and Hyperliquid: A Shifting Regulatory Picture

The backdrop that justified the block is changing fast. In late May 2026 the CFTC cleared the first true perpetual futures contract on a registered U.S. exchange, KalshiEX's bitcoin product, and paired it with a policy statement setting a case-by-case review for future perpetuals.

CFTC Chairman Mike Selig cast the move as a clean break from the "regulation by enforcement" era that, in his account, pushed builders offshore. Bringing perpetuals onshore, he argued, lets regulators contain leverage and systemic risk in a supervised framework instead of exporting it. The same day, CFTC staff let Coinbase route U.S. customers to perpetuals on its offshore Deribit affiliate as foreign futures.

Three points matter for Hyperliquid specifically:

- Hyperliquid was not named. The approvals went to Kalshi, Kraken and Coinbase, each registered U.S. entities. Hyperliquid's interface stays restricted; the CFTC opened a category, not a door for this protocol.

- It is guidance, not a rule. Policy statements and no-action letters carry weight but lack the durability of a formal rule or a statute, so a future commission could reverse course.

- The category is the prize. Traders read the decision as a green light for perpetuals overall, the market Hyperliquid dominates, and the agency now has a template for contracts referencing other assets.

Hyperliquid's Washington Lobbying Push

Hyperliquid is not waiting on regulators. On February 18, 2026, the Hyper Foundation seeded the Hyperliquid Policy Center, a Washington advocacy nonprofit, with one million HYPE tokens worth around $29 million, per CoinDesk. It is led by crypto attorney Jake Chervinsky, former legal chief at the Blockchain Association, and works on rules for decentralized exchanges, perpetuals, and on-chain market infrastructure.

The argument is that DeFi derivatives belong inside the U.S. market through a tailored pathway, not shut out by default, and it leans on transparency. In a comment letter to the CFTC's perpetuals review, Hyperliquid argued that on-chain execution makes every order, fill, liquidation, and funding payment publicly verifiable, exposing more market activity than an opaque order book, not less. The Policy Center has since pressed the same case in meetings with the CFTC.

That puts Hyperliquid at a crowded table beside the DeFi Education Fund, the Solana Policy Institute, and the Blockchain Association. The bet is simple: help write the framework before it hardens, so the eventual U.S. path fits a non-custodial venue rather than one built for centralized intermediaries.

CME, ICE, and the Push to Regulate Hyperliquid

Not everyone in Washington wants Hyperliquid opened up. In mid-May 2026, Bloomberg reported that CME Group and Intercontinental Exchange, owner of the New York Stock Exchange, were pressing the CFTC and Congress to put Hyperliquid under federal oversight. Their stated worry is market integrity: as commodity perpetuals there have swelled, including heavy weekend oil trading, they warn a large, lightly supervised venue could distort price discovery for benchmarks like crude. They also cite sanctions-evasion risk.

Their ask is that Hyperliquid register with the CFTC, which would force the platform to add customer identification and trade surveillance, the exact KYC layer it was built to avoid. The Policy Center rejected the framing, arguing that a traditional exchange matching buyers and sellers for fees differs structurally from an on-chain protocol.

The competitive angle is plain. Both CME and ICE have been shipping their own crypto derivatives, with CME launching bitcoin volatility futures and a Nasdaq-linked crypto index in early June 2026. Critics read the campaign as an effort to slow a rival through regulation rather than beat it on the order book.

The result is a tug-of-war, one camp lobbying to open a U.S. lane, another to force registration, with the CFTC holding the pen.

How US Traders Can Get Hyperliquid Exposure Today

The Hyperliquid app is still blocked for US users. What changed in 2026 is that you can now get regulated, onshore exposure to HYPE and to HYPE-based perpetuals without it. None of these is the same as trading on Hyperliquid, but a year ago there was nothing legal at all.

- Kalshi's "American Perpetuals": Kalshi lists CFTC-regulated perpetuals that track HYPE on its registered US exchange. It built them with Hyperliquid through the HIP-4 upgrade, so this is the closest you can get to a real HYPE perp without the blocked app.

- Spot HYPE ETFs: Bitwise and 21Shares launched spot HYPE funds in May 2026, and Grayscale's GHYP is working through SEC review. The funds hold HYPE and trade on US exchanges, so any brokerage or retirement account can buy price exposure with no wallet or on-chain steps.

- Coinbase to Deribit: A CFTC no-action letter lets Coinbase send US customers to perpetuals on its offshore Deribit affiliate, treated as foreign futures. You can post crypto or stablecoins as margin.

All of these are proxies. An ETF tracks HYPE's price, not your trading, and Kalshi's perpetuals run under Kalshi's rules, not Hyperliquid's liquidity or its 100-plus markets. None of them gets you into Hyperliquid itself.

For where to deploy capital now, see our rankings of the best decentralized perpetuals exchanges and best crypto futures exchanges, which cover the venues open in every market.

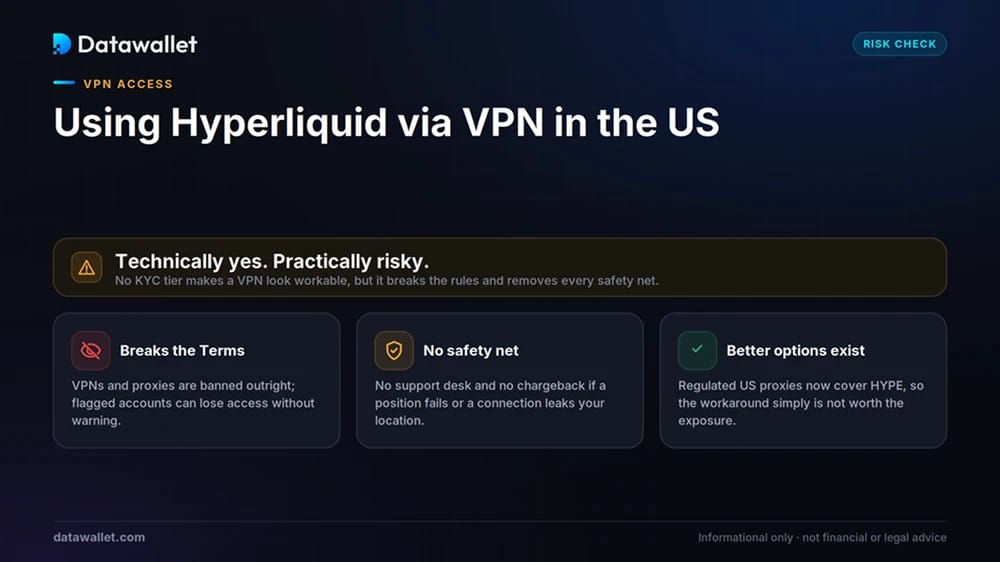

Can You Use Hyperliquid With a VPN in the US?

The missing KYC layer makes a VPN look more workable here than on a centralized exchange, where ID would expose your jurisdiction. In practice it is a bad move.

It breaks the contract first. Hyperliquid's terms expressly ban VPNs, proxies, and any location-masking tool, and bar misrepresenting your residency or citizenship. Flagged accounts can lose access, and since the restriction follows U.S. citizens anywhere, "I was traveling" is not a defense the terms accept.

The safety net is also thin. If the connection drops mid-position and leaks your real location, or access is pulled while you hold leverage, there is no support desk, no chargeback, no recourse. The protocol stays visible even when the front end is geofenced, luring restricted users into workarounds with nothing behind them. With regulated U.S. proxies now available, the math on circumvention only looks worse.

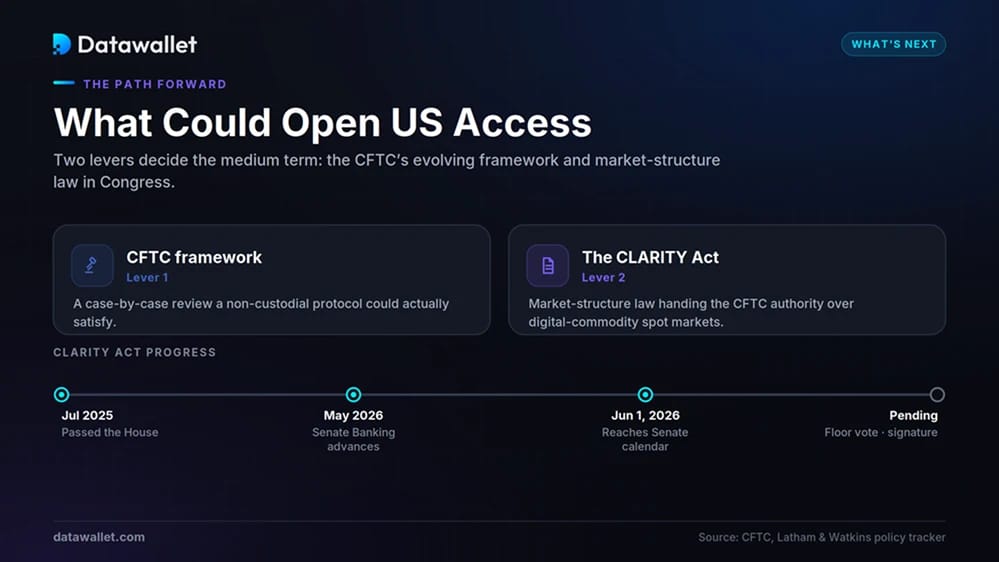

What Could Change for US Hyperliquid Access?

Two threads decide the medium term - the CFTC's evolving perpetuals framework and the market-structure bill in Congress.

On the legislative side, the Digital Asset Market Clarity (CLARITY) Act would give the CFTC exclusive authority over digital-commodity spot markets and protect developers who publish code without holding user funds. It also includes tailored rulemaking for intermediaries that are not truly decentralized.

The House passed it in July 2025 and the Senate Banking Committee advanced its version in May 2026. On June 1, 2026 the bill reached the Senate calendar for floor consideration, per the Latham & Watkins policy tracker. A floor vote, reconciliation, and a signature still stand between it and law.

The CFTC's case-by-case process is the nearer-term lever. If the agency builds a framework a non-custodial protocol can meet, or Hyperliquid stands up a compliant U.S. structure, the largest blocked market in crypto could open. That stays an "if," and the CME/ICE camp is working to attach full registration to any onshore path. The likely sequence: regulated proxies widen first, direct access later and on the regulators' terms, if at all.

Bottom Line

As of June 2026, you cannot trade on Hyperliquid directly in the United States. U.S. persons are Restricted Persons, geofencing enforces the block, and the terms forbid the VPN workarounds people reach for. That part holds.

Everything around the wall is moving. The CFTC has opened the U.S. perpetuals category for the first time, regulated HYPE perpetuals and spot HYPE ETFs now exist for Americans, and Hyperliquid's advocacy arm is pressing for a tailored DeFi framework while CME and ICE push to force registration.

The direct answer is still no. The useful one is that the country has moved from a flat ban to an active, contested negotiation, and this year's regulated on-ramps show where it is heading. For how the platform works, start with our Hyperliquid explained guide.