Compare the Top P2P Crypto Exchanges

1. Binance

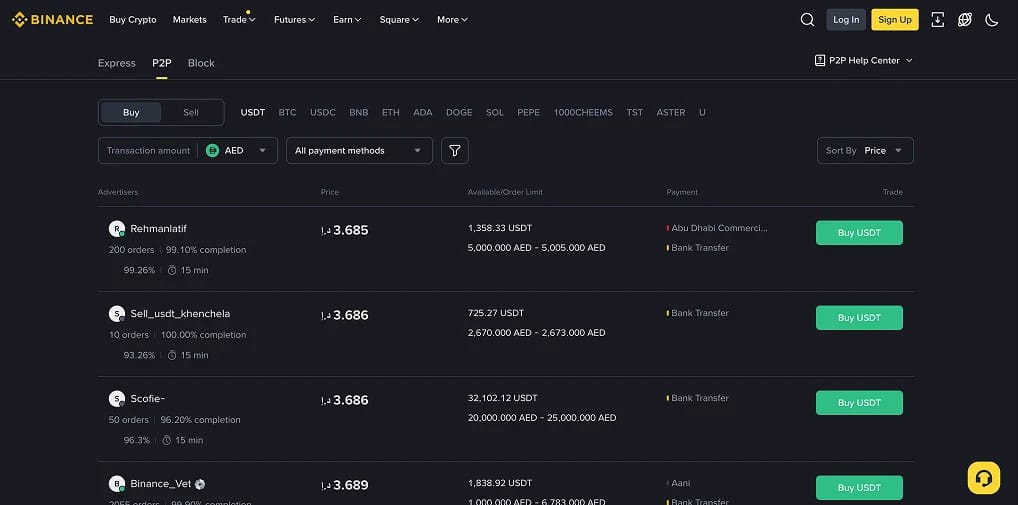

Binance is the desk we open first when we need a merchant to actually be there. It carries the deepest P2P book anywhere, covers 100+ fiat currencies, and lists several hundred local payment methods, which keeps it the default on-ramp in most markets that run on P2P. More merchants on a pair means a tighter spread, and on size that is the gap between a fair fill and a 2% haircut.

Trades clear through escrow at zero fees, merchant profiles show completion rate, release time and order count, and a real-name payment rule screens out a lot of mule traffic by forcing the paying account to match your verified name. When we let a payment window expire, the appeal flow was the clearest here. Note that SAFU covers platform failures, not a bad counterparty.

Binance's real exposure is regulatory. It pulled fiat P2P under regulator pressure in Nigeria, shutting its naira P2P desk during the 2024 crackdown that detained executives and triggered tax charges. Listings can thin fast, so we anchor on Binance but never rely on it alone.

Pros

- Deepest global P2P liquidity with the tightest quotes on larger orders.

- 100+ fiat currencies and hundreds of payment methods at zero platform fees.

- Real-name payment matching and the clearest appeal process on test.

Cons

- Has pulled fiat P2P under regulatory pressure, Nigeria being the clearest case.

- Strict real-name rules stall trades when your account name does not match.

- The P2P desk sits a few menus deep, which trips up newcomers.

2. OKX

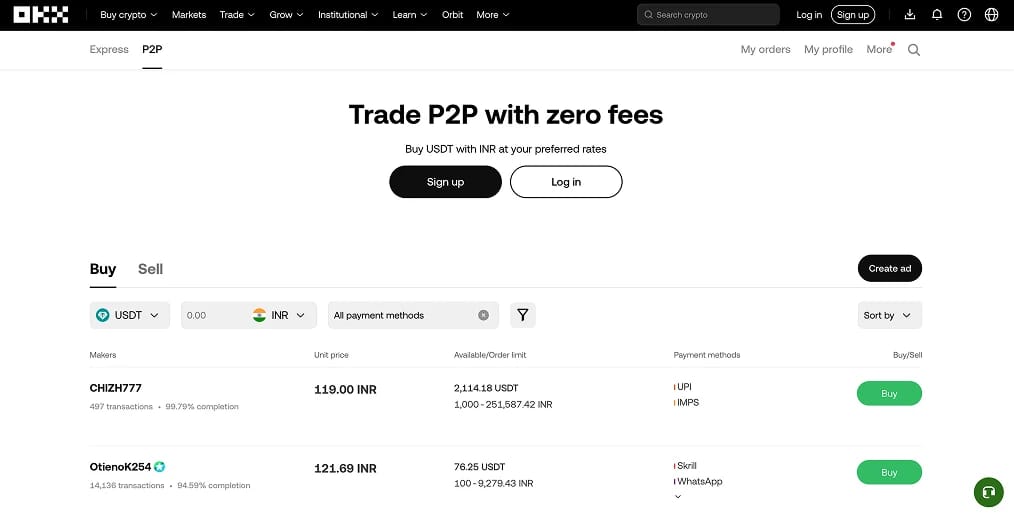

OKX ranks second on the part of P2P that protects you, not the part that prices you. Its Blue Shield programme vets merchants before they can post ads, and the T+N hold on P2P-bought funds cuts the odds of an instant freeze from a counterparty whose cash turns out to be tainted. That delay is the most useful anti-freeze feature on any major desk.

P2P fees are zero, and the desk genuinely trades the niche Asian and African pairs others skip, which is where its depth earns its keep. OKX publishes monthly proof-of-reserves, one of the cleaner disclosure records among large exchanges. In testing, matching lagged Binance slightly on thin pairs off-peak, so small orders saw wider spreads, though merchant quality and the dispute flow stayed consistently clean.

Past the on-ramp, the built-in Web3 wallet bridges straight from your trading account into DeFi and DEX swaps, sparing a second app on a phone already short on storage. Like every offshore desk, OKX answers to no local regulator, so your protection comes from its own escrow and vetting rather than a deposit guarantee. For a buyer who values freeze defence over raw depth, that combination is hard to beat.

Pros

- Blue Shield vetting plus a T+N hold, the strongest freeze defence here.

- Zero P2P fees and real depth in niche Asian and African fiat pairs.

- Monthly proof-of-reserves and a built-in Web3 wallet.

Cons

- Merchant depth on smaller pairs trails Binance off-peak.

- Spreads on sub-$200 orders widen outside business hours.

- The T+N release frustrates users expecting instant access.

3. Bybit

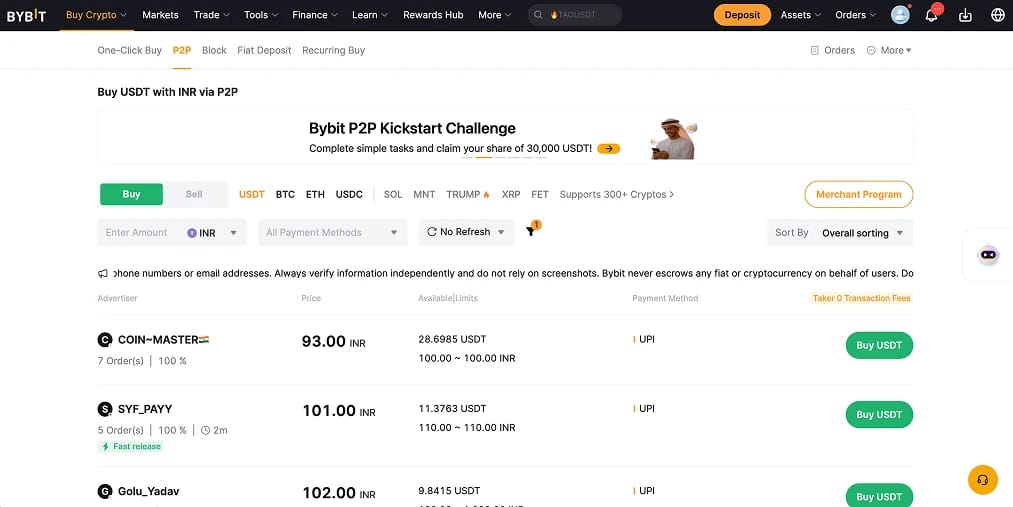

Bybit is the desk we point first-timers to, because the flow assumes the least. Every advertiser shows completed orders, completion rate, release time and reviews up front, and the filters screen by payment method and reputation in two taps. The buy sequence skips the menu-diving that trips people up elsewhere.

It covers 60+ fiat currencies at zero fees and stays responsive on mid-range Android over mobile data, which matters in the markets that lean on P2P most. On test, escrow released fast against high-reputation merchants and the in-app payment guidance was the clearest of the group. Bybit has pruned fiat in some frontier markets, so check the live book before assuming last month's route still works.

The trading stack underneath is deep, with spot, perpetuals, copy trading and Earn on idle USDT, so the platform grows with you once the P2P step is done. Our crypto futures exchange guide covers how its perps compare for anyone graduating from spot. Fiat coverage is still narrower than Binance, so in smaller markets you may need a second desk alongside it.

Pros

- The cleanest, most legible P2P flow for first-time buyers and sellers.

- Transparent merchant stats and fast, intuitive ad filtering.

- Zero P2P fees and a light app footprint on low-end phones.

Cons

- Narrower fiat coverage than Binance, with support dropped in some markets.

- Merchant depth on local pairs thins outside the largest markets.

- The wider product menu distracts users who only want USDT.

4. Bitget

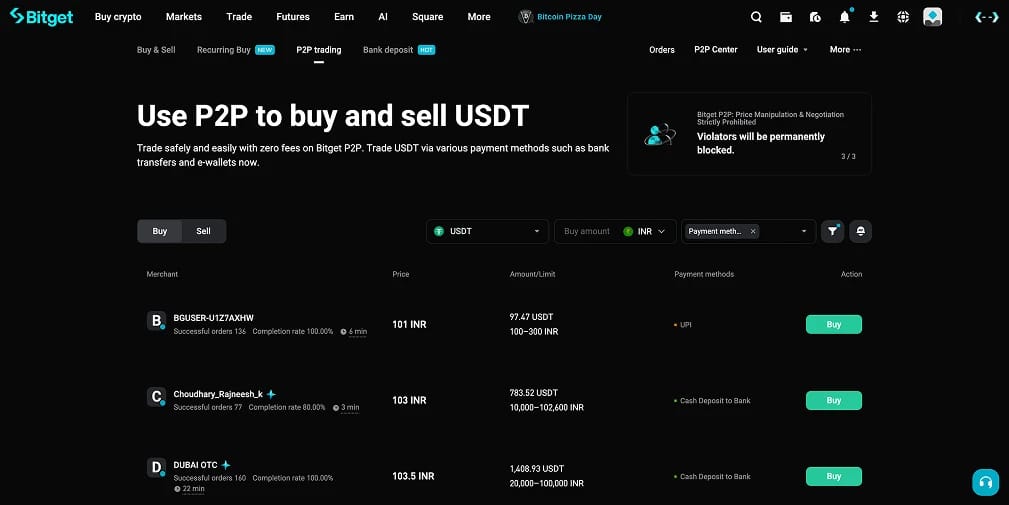

Bitget is the zero-fee desk that travels well into emerging markets with a reassuring balance sheet behind it. Its proof-of-reserves has shown a ratio near 169%, and the protection fund sits above $400 million, the kind of cushion that counts when no local regulator will take your call. The desk runs 100+ fiat currencies over bank transfer, mobile money and card at zero P2P fees.

It works best when the P2P trade is a funding step into the wider ecosystem rather than a one-off. Merchant depth is mid-pack, solid in local business hours and thinner late at night, so we check the book before a larger order. Card funding works but carries the usual 2% to 5% processor markup, which makes bank transfer or mobile money the cheaper first choice.

Copy trading is the reason most users stay in-app after their first USDT purchase, with a pool deep enough to filter by drawdown history rather than headline returns. Brand recognition is lower than Binance in some markets, so local dispute volumes are less battle-tested. As a funding rail with a genuine reserve cushion, though, it is one of the safer mid-tier picks here.

Pros

- Zero-fee P2P across 100+ fiat currencies with broad payment coverage.

- A 169% reserve ratio and a $400M+ protection fund as a platform cushion.

- Strong copy trading for users who stay after funding.

Cons

- Merchant depth is mid-pack and thins outside business hours.

- Card funding carries the usual 2% to 5% processor markup.

- Lower brand recognition means less-tested local dispute volumes.

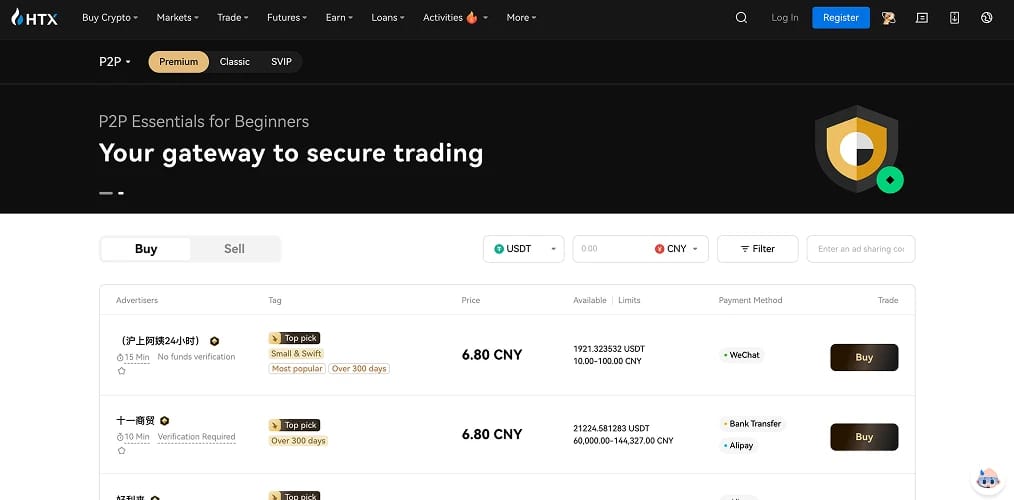

5. HTX

HTX, the former Huobi, holds fifth on the deepest Alipay and WeChat Pay merchant network of any major platform, a legacy of its Chinese roots. For Asian P2P, and for USDT routed over Tron where much of the region's stablecoin volume lives, it usually shows the tightest spreads and most active merchants at any hour. Our Alipay buying guide and China exchange guide cover the grey-zone context.

The desk takes Alipay, WeChat Pay, UnionPay and bank transfer through a merchant base over a decade deep, which is its real edge over newer venues. For users in tier-two Chinese cities funding through Alipay or WeChat Pay, that depth means faster fills and tighter USDT spreads than any Western-led desk manages.

Brand baggage is the price of that depth. The Tron association, Justin Sun's involvement and the rebrand all weigh on trust, and proof-of-reserves disclosures lag Binance and OKX. We treat HTX as a P2P venue where its merchant depth genuinely helps, not as long-term custody for size.

Pros

- Deepest Alipay and WeChat Pay P2P network in Asian hours.

- Strong Tron and USDT proximity, the dominant Asian stablecoin rails.

- Long-standing, familiar Chinese-language product.

Cons

- Reputation is softer than Binance or OKX after the rebrand.

- Proof-of-reserves disclosures are less consistent than top peers.

- KYC snags are more common, with slower dispute escalation.

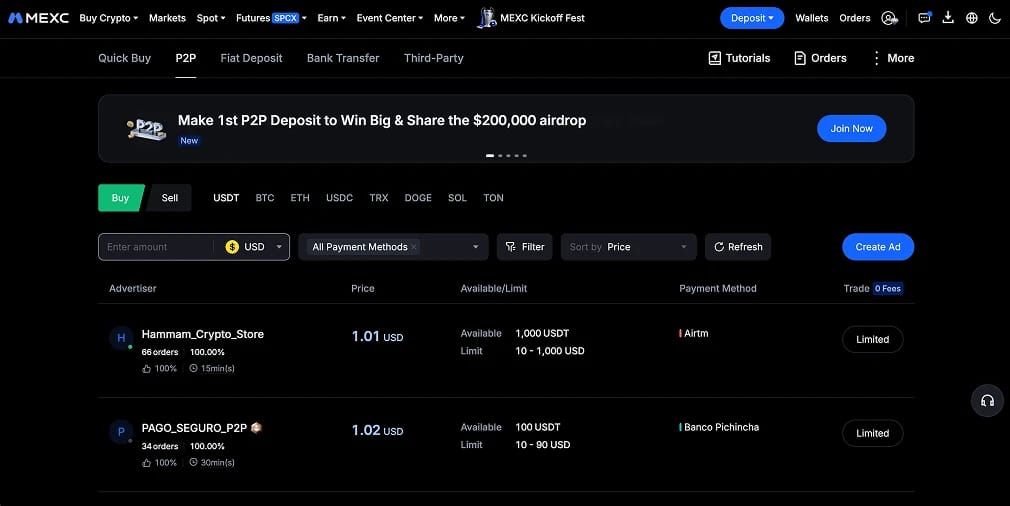

6. MEXC

MEXC closes the list as the budget on-ramp, best when P2P is just the step to get USDT into a low-cost trading account. P2P is free, spot runs 0% maker and 0.02% taker, and the catalogue is huge, so newly launched tokens often land here first. A low-KYC tier moves smaller amounts without full verification, which suits users wary of tying an ID to an offshore account.

What lets MEXC down is the desk itself. The merchant pool is younger and thinner than Binance or HTX, so we filter hard on completion rate and order count rather than trusting the promotional ads at the top of the book. On smaller pairs the book can empty out entirely outside peak hours.

Proof-of-reserves cadence also lags the leaders, which matters more for anything you hold than for a quick funding pass. As a cheap rail to move USDT into trading it does the job; as your only off-ramp in a pinch it is the weakest option here. Pair it with a deeper desk and it earns its place.

Pros

- Zero P2P fees plus 0% maker spot, the lowest all-in funding cost here.

- Huge asset selection with one of the fastest listing pipelines.

- Low-KYC tier for smaller deposits without full verification.

Cons

- Younger, thinner merchant pool, so vet order histories carefully.

- Proof-of-reserves transparency trails the top platforms.

- Better as a secondary funding venue than a primary off-ramp.

How to Choose a P2P Crypto Exchange

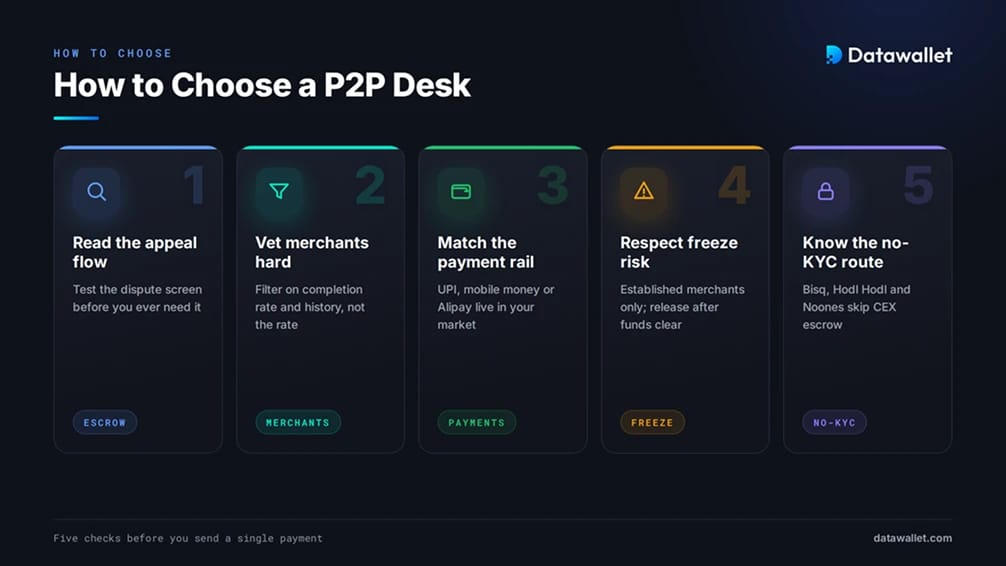

Features barely register. You are choosing whose escrow and dispute process you trust with a stranger on the other side. Five checks we run before sending a payment:

- Read the appeal flow before you need it: Open a trade with a top-rated merchant and study the dispute screen without filing one. You want clear evidence prompts, a set response window, and a human path if automation fails.

- Filter merchants on history, not rate: Trade only with advertisers showing high completion rates, fast release times and long order records. Verified badges like OKX Blue Shield carry weight. Treat any rate well above market as a warning, since cash that good usually needs moving fast.

- Match the payment method to your rails: UPI in India, bank transfer or mobile money in Nigeria, Alipay or WeChat Pay in China. Filter the live book for your currency and confirm a couple of dozen active merchants in local hours. An empty book means the platform is not usable for you.

- Respect the tainted-funds freeze risk: If a scammer pays you with stolen money, the victim's report can lead police to your account and your bank can freeze it, even though you did nothing wrong. No escrow stops this. Use established counterparties, release only after funds clear your account, and keep every order log.

- Consider a non-custodial desk to skip CEX escrow: No-KYC markets like Bisq, Hodl Hodl and Noones use multisig escrow instead of a company wallet. Liquidity is thinner and the curve steeper, but for privacy-focused or banking-excluded users they remove the platform as a point of failure.

How P2P Crypto Trading Is Regulated Across Major Jurisdictions

No single law governs P2P. It sits where each country's crypto stance, capital controls and money-laundering rules meet, which is why the same trade is routine in one market and risky in the next.

- Nigeria, the world's largest P2P market: Nigeria long topped global P2P volume after the 2021 bank ban pushed activity onto P2P desks. The Investments and Securities Act 2025, signed in March 2025, now recognises crypto as securities under the SEC, and exchanges must register, with early licences to Quidax and Busha. Enforcement bit too: Binance shut its naira P2P desk, and the EFCC can now pull telecom records. Our Nigeria exchange guide goes deeper.

- India, legal but unregulated: Trading is legal and crypto is a Virtual Digital Asset, but there is no dedicated P2P framework, so general criminal and AML law applies. Domestic exchanges register with FIU-IND under the PMLA, and the live risk for P2P users is the bank freeze covered below. See our India exchange guide and guide to buying USDT in India.

- China, where P2P is the workaround: The 2021 9.24 Notice bans crypto business and bars overseas exchanges from serving residents online, yet personal ownership is legal and CNY P2P over Alipay and WeChat Pay remains the main on-ramp. A November 2025 PBoC meeting named stablecoins as the next target, so treat the channel as provisional.

- Russia, tightening under sanctions: Crypto is tolerated for cross-border trade but squeezed at retail. A Bank of Russia framework routes trading through licensed intermediaries from July 2026, caps non-qualified investors near 300,000 rubles a year, and excludes privacy coins. Banks now flag and freeze accounts linked to P2P platforms.

- Pakistan, Vietnam and the wider Global South: These rank near the top of adoption (Pakistan and Vietnam placed third and fourth in the latest Chainalysis index), driven by remittances and currency hedging, with frameworks still being written. P2P stays the default because regulation has not caught up.

Across all of these markets, holding crypto is legal almost everywhere, but P2P sits in the unregulated space between that right and each country's payment and AML rules. The line drawn most consistently is against using crypto as money at home, not against buying or selling it.

How Is P2P Crypto Taxed?

P2P trades do not dodge tax just because no intermediary issues a statement. The obligation often shifts onto you instead, and treatment varies sharply by country.

- India puts the burden on the trader: VDA profits are taxed at a flat 30% plus 4% cess under Section 115BBH, with no loss offset. A 1% TDS under Section 194S applies above the annual threshold, and on P2P and international platforms the buyer must deduct and deposit it, not an exchange. An 18% GST on platform fees has applied since July 2025. Report it all in Schedule VDA.

- Nigeria now has a statute: The Nigeria Tax Administration Act 2025 establishes crypto taxation, much of it pushed onto licensed VASPs, with gains under capital gains tax. The enforcement machinery is still maturing, but the legal basis exists.

- Most other markets tax disposals under existing rules: With or without crypto-specific law, selling crypto for fiat is generally a taxable disposal, and trading at business scale attracts income tax. The absence of a dedicated regime is a gap, not a green light.

Wherever you trade, log every order, counterparty, fiat value and any tax withheld. As enforcement catches up with the law, it reaches backwards. None of this is tax advice, and a local professional earns the fee in any market with an active crypto tax regime.

P2P Crypto Adoption

P2P grew up as the on-ramp of necessity. Where banks blocked crypto, the local currency was sliding, or capital controls closed the official route, buying USDT from another person over a payment app was the one door left open.

That story still drives the data. The latest Chainalysis Global Crypto Adoption Index ranks India first, with Pakistan, Vietnam, Brazil and Nigeria all in the top six, and seven of the top ten in lower or upper-middle income brackets. Sub-Saharan Africa took in over $205 billion on-chain, Nigeria alone above $92 billion, skewed toward the small retail transfers where P2P lives.

Chainalysis dropped its dedicated P2P sub-index in 2025 as P2P's share of activity declined and direct on-ramps formalised. That does not mean P2P is shrinking where it matters; it is narrowing to markets with weak banking, unstable currencies or capital controls. Stablecoins power all of it, with USDT clearing over a trillion dollars a month and functioning, across much of the Global South, as a dollar savings account the banks cannot offer.

How to Buy Bitcoin via P2P

Buy USDT from a vetted merchant first, then swap into Bitcoin on spot, since USDT is where P2P liquidity concentrates. The sequence we use:

- Pick a desk with a live book in your currency. Open Binance or OKX, go to P2P, filter for your fiat and payment method, and check the rate against mid-market USDT before committing.

- Complete KYC with matching details. Use a government ID and make sure your account name matches the bank account or wallet you pay from. Mismatches are the top reason trades and verification stall.

- Buy USDT from a high-reputation merchant. Pick a long-history advertiser with a high completion rate and verified badge, pay, mark paid only after the transfer confirms, and wait for escrow. As a seller, release only once funds clear.

- Swap USDT for BTC with a limit order. Skip one-click convert, open BTC/USDT, and place a limit order. That usually saves 1% to 3% over the instant-buy spread.

- Decide where the BTC lives. Traders can leave it on the exchange; long-term holders should self-custody, checking address and network first. Our best crypto wallets guide covers the options.

The same desks run in reverse for cashing out, selling USDT to a merchant who pays your bank or mobile money account directly.

Final Thoughts

Choose a P2P platform by what protects you when a trade breaks, not by a fee that is almost always zero. Binance anchors on depth and payment coverage, OKX wins on merchant vetting and freeze defence, and Bybit is where we send first-time traders. Bitget, HTX and MEXC each earn a slot for reserve transparency, Asian depth, or the cheapest funding rail.

Keep a second desk verified, because P2P books in frontier markets change without notice. And track the regulatory file: Nigeria has moved to SEC licensing, Russia's intermediary rules land in July 2026, and India's freeze enforcement keeps tightening. The grey zone that makes P2P useful is the same thing that exposes you if you treat it carelessly.

Before moving size, run one small trade against a top-rated merchant end to end and confirm the off-ramp works for your bank. Ten minutes of testing beats any review, this one included.

Our Methodology

We evaluated the leading P2P desks by creating accounts, completing KYC, and funding real orders as both buyers and sellers across bank transfer, mobile money and instant-payment rails, then off-ramping back to fiat. Each platform scored across six criteria:

- Trust Score: Our proprietary rating (out of 5) weighting security history, proof-of-reserves transparency, regulatory standing, longevity and audit coverage.

- Escrow and Dispute Quality: We opened trades, read the appeal flow, and tested how each handled an expired payment window, scoring clarity, evidence prompts and response time.

- Merchant Vetting: We reviewed verification programmes, badge systems and the transparency of completion rates, release times and order histories.

- Fiat and Payment Coverage: We confirmed supported currencies and local payment methods, testing merchant depth and spread against mid-market USDT in local hours.

- Freeze and Reversal Defence: We assessed real-name rules, withdrawal holds and the guidance each desk gives to cut exposure to tainted-funds and reversal scams.

- Underlying Platform: We measured fees, asset selection and security so the venue holds up beyond the P2P trade.

We excluded platforms with no functional P2P book, persistently thin depth, or serious unremediated compliance failures. Testing ran across early 2026.