Perpetual futures sit at the center of global crypto trading, yet for nearly a decade US traders could only reach them through offshore platforms outside American rules.

Kalshi changed that in mid-2026 by listing the first perpetual contract approved by a US regulator. It launched with heavy volume and a different design from the high-leverage venues that dominate the category abroad.

For anyone weighing whether onshore perps are worth using, the details matter more than the headlines. Here is how Kalshi Perpetuals work, what sets them apart, and where the risks sit. 👇

What Are Kalshi Perpetuals (Perps)?

Kalshi Perpetuals are derivative contracts that let you take a leveraged position on a crypto asset's price, such as Bitcoin or Ethereum, without owning the asset and without a settlement date. You go long if you expect the price to rise and short if you expect it to fall.

Two features separate a perpetual from buying crypto. Leverage lets a smaller amount of collateral control a larger position, and the lack of expiry means a position stays open as long as enough collateral backs it.

Kalshi already runs the leading US prediction markets business, and perps are its first product outside the yes-or-no event contracts that built the company. The exchange now offers both regulated event contracts and regulated perpetuals in one account.

Kalshi frames the move as an evolution from prediction market leader into a next-generation derivatives exchange. A trader can bet on whether an event happens and take a directional, leveraged view on an asset's price from the same balance.

How Do Kalshi Perps Work?

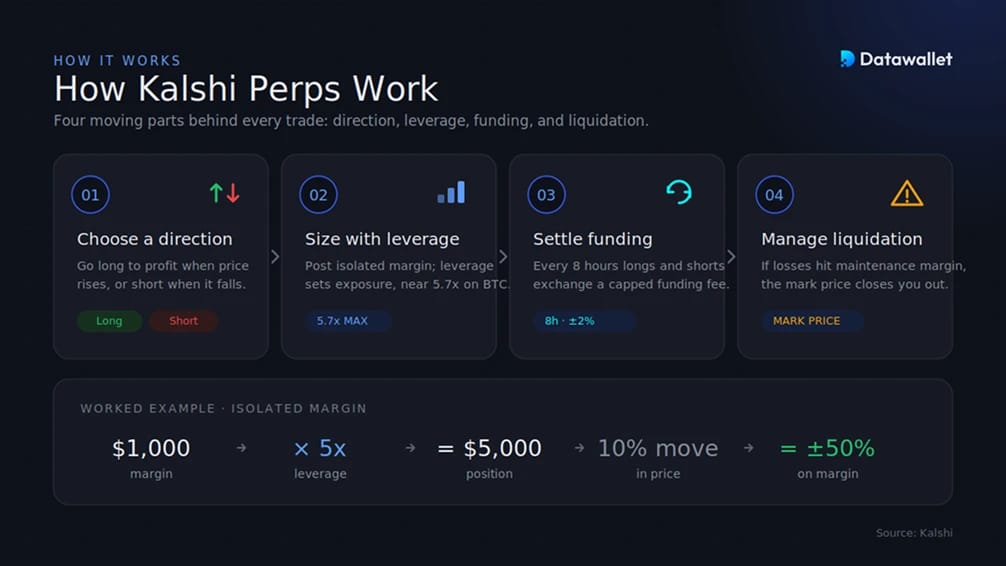

A Kalshi perpetual trade comes down to picking a direction, sizing the position with leverage, then managing two forces: the funding rate that ties the contract to spot, and the liquidation threshold that closes you out if the trade moves too far against you.

1. Direction: Long or Short

Every position starts with a side. A long profits when the asset rises and behaves like a leveraged version of buying. A short profits when it falls, which spot trading cannot do, since spot only rewards rising prices.

This two-sided design is the core appeal of perps. Traders can express a bearish view, hedge existing exposure, or position around volatility without selling any holdings.

2. Leverage and Margin

To open a position you post collateral, also called margin, and leverage decides how much exposure it controls. At 5x leverage, $1,000 of margin backs a $5,000 position, so a 10% move in the asset becomes a 50% swing in your collateral either way.

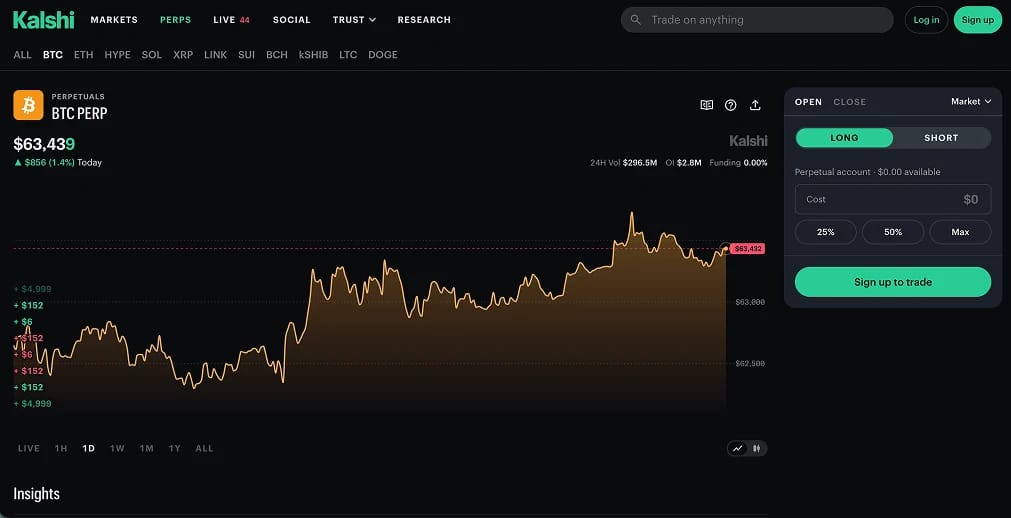

Kalshi uses isolated margin, where the collateral assigned to a trade is the amount at risk on it. Its maximum leverage is set conservatively and adjusts with conditions, with Bitcoin capped near 5.7x at launch and most altcoins lower. That contrasts sharply with offshore perpetual exchanges, which routinely offer 50x, 100x, or more.

3. The Funding Rate

Because perpetuals never expire, no settlement event pulls the contract price back toward the real market price. The funding rate handles that through a recurring payment between longs and shorts.

When the perpetual trades above spot, longs pay shorts, which makes holding a long costlier and nudges the price down. When it trades below spot, shorts pay longs and the price is pushed up. On Kalshi, funding settles every 8 hours, caps at ±2% per period, and shows in your transaction history. You can track live rates across the market on our crypto funding rates dashboard.

4. Liquidation

Liquidation happens when losses drain your collateral to a minimum called the maintenance margin, at which point the position closes automatically to stop the account going negative. Higher leverage shortens the move needed to trigger it.

Kalshi calculates liquidation against a mark price, an aggregated reference drawn from several spot markets rather than one exchange feed, which reduces the chance of being liquidated by a brief spike on a single venue. Our Bitcoin liquidation heatmap maps the price levels where cascades tend to form.

Kalshi Perps vs Spot Trading

The clearest way to understand perps is against simply buying crypto. Spot trading means owning the asset, with no leverage, no funding cost, and no forced closure. Perps trade the price instead, unlocking shorting and leverage while adding ongoing costs and liquidation risk.

Perps suit short-term, directional, or hedging strategies, while spot fits long-term accumulation. Our breakdown of perpetuals versus spot trading covers the trade-offs in more depth.

What Can You Trade on Kalshi Perps?

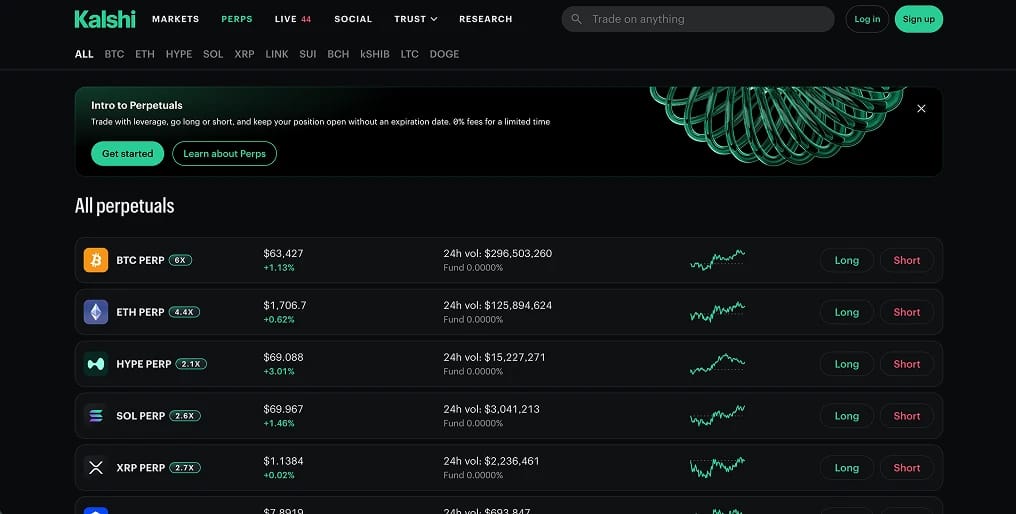

Kalshi launched its perpetuals with Bitcoin and widened the lineup quickly through the regulatory filing process. As of early June 2026, its official guide listed 13 CFTC-approved crypto perpetual contracts, with more in review.

The roster covers the major liquid assets, each with a maximum leverage that reflects how volatile and deep the underlying market is:

- Large caps: Bitcoin and Ethereum carry the highest leverage, around 5.7x and 4.3x at launch.

- Mid caps: XRP, Solana, Chainlink, Dogecoin, and Litecoin sit lower, generally between 2x and 3x.

- Smaller caps: Sui, Polkadot, Bitcoin Cash, Stellar, Hedera, and Shiba Inu carry the tightest leverage, often below 2x.

These figures are dynamic and can change without notice as Kalshi adjusts risk parameters. The exchange has confirmed it will not list perpetuals on agricultural commodities, a limit tied to the CFTC's view that the perpetual design does not suit every asset class.

Kalshi Perpetuals Statistics

Kalshi's perpetuals are only weeks old, yet the early data already ranks them among the most active products the exchange has shipped. The numbers below reflect the latest available figures and shift fast, since volume is notional and open interest changes with every open position.

- Launch ramp: Perps cleared $100 million in volume on day one, $1 billion inside a week, and more than $5.5 billion in notional within two weeks, the fastest product ramp in Kalshi's history.

- Daily volume: By mid-June, the BTC perpetual alone was turning over roughly $1.2 billion in 24-hour volume, with the ETH contract near $560 million and HYPE, SOL, and XRP posting eight-figure days.

- Open interest: The rollout pushed Kalshi's overall open interest to a record near $810 million, as perpetuals began accumulating standing positions that expiring event contracts never could.

- Markets live: Eleven crypto perpetual markets were trading by mid-June, led by Bitcoin and Ethereum, with further assets filed for approval.

- Leverage range: Maximum leverage tops out near 5.7x on Bitcoin and scales down for smaller, more volatile tokens, a fraction of the 50x to 125x common offshore.

Headline volume is notional, counting the full contract value including leverage rather than cash at risk, so treat it as a gauge of activity rather than dollars deposited.

Why Kalshi Perps Are Different

Perpetual futures have existed offshore since BitMEX listed the first Bitcoin perp in 2016, and the category has grown enormous. Offshore perpetual volume climbed from $28 trillion in annual notional in 2023 to more than $90 trillion in 2025, a market US traders were largely locked out of according to CNBC.

Kalshi's main differentiator is regulation. Listing perps on a CFTC-supervised exchange gives US traders onshore access with transparent funding, mark-price liquidation, and the protections of a regulated market.

The second is risk posture. Where offshore platforms compete on triple-digit leverage, Kalshi's single-digit caps and capped funding read as an institution-friendly design aimed at hedgers and professionals who had no compliant venue before.

The third is breadth. Kalshi is the only US exchange where a trader holds both regulated event contracts and regulated perpetuals in one account, blending probability-based and price-based exposure.

Kalshi Regulation & CFTC Approval

On May 29, 2026, the Commodity Futures Trading Commission issued an Order for Approval to KalshiEX, LLC for its BTCPERP contract, a perpetual that references Bitcoin's spot price and is treated as a futures product. Kalshi submitted it under Commission Regulation 40.3, with the order issued under the Commodity Exchange Act.

This was the first perpetual futures contract approved under the voluntary Regulation 40.3 process, which set the analytical template for every submission that follows. KalshiEX argued that a contract counts as a future based on whether it creates future payment obligations, not on whether it ends on a fixed date, and the Commission agreed.

CFTC Chairman Mike Selig, confirmed in late 2025, had committed to bringing crypto perpetuals onshore and called the approval a historic step, grounding the decision in the depth and round-the-clock nature of the Bitcoin spot market.

One caveat matters for accuracy. Kalshi markets the product as America's first perpetuals, but the CFTC earlier cleared Bitnomial to offer a similar contract with a 25-year limit, which made it not truly perpetual. Kalshi's BTCPERP is the first with no end date at all.

Kalshi and the Competitive Landscape

The launch did not happen in isolation. On the same day, the CFTC cleared a path for a Coinbase affiliate to connect US customers to global perpetual and options markets, signaling it intends to open the lane to multiple firms rather than one winner.

Not every incumbent welcomes the shift. On June 18, 2026, CME Group, the largest US futures exchange operator, sued the CFTC and Chairman Selig to void the approvals, arguing perpetuals are swaps under the Dodd-Frank Act rather than futures. The suit names neither Kalshi nor Coinbase, and the CFTC dismissed it as frivolous, but it leaves the legal footing of US perps unsettled for now.

Rival prediction market Polymarket has been moving toward its own 24/7 long-short trading, part of a broader convergence where event-contract platforms add leveraged derivatives. Offshore, the deep liquidity still sits with Hyperliquid, Binance, and Bybit, so Kalshi's early edge is regulatory rather than order-book depth.

The traction came fast. Kalshi's perpetuals saw over $100 million in volume on day one, crossed $1 billion within a week, which the company called its fastest-growing product ever, and topped $5.5 billion in notional within two weeks.

The next step is non-crypto perps. Co-founder Tarek Mansour has said Kalshi is in talks with regulators about other asset classes, and a June 12 CFTC no-action letter pushed other contract markets to convert perpetual-style products into true perpetuals, pointing toward commodities and equity indexes next.

Who Is Behind Kalshi?

Kalshi was founded in 2018 by Tarek Mansour and Luana Lopes Lara, who built it into the first federally regulated prediction market exchange in the US and created the event contract as an asset class. Mansour, the CEO, previously traded at Goldman Sachs and Citadel and studied at MIT.

The company spent close to two years proving to the CFTC that event contracts were not gambling, winning approval in 2020. That groundwork is what later made the perpetuals approval possible on the same designated contract market license.

Growth has been steep. A March 2026 round led by Coatue Management valued Kalshi near $22 billion, double its valuation months earlier, with backers including Sequoia, Andreessen Horowitz, Paradigm, and ARK Invest.

The company still faces friction. Kalshi has fought state-level challenges including a Nevada ban and Arizona criminal charges tied to its event-contract operations, disputes separate from perpetuals but part of the backdrop it operates in.

Risks of Trading Kalshi Perpetuals

Kalshi perpetuals are regulated, but regulation does not remove the dangers of leveraged trading. Understand these risks before committing capital.

- Leverage Amplifies Losses: Even at conservative caps, leverage magnifies gains and losses, and a small adverse move can wipe out a position's collateral.

- Liquidation Risk: If losses hit the maintenance margin, the position closes automatically. Higher leverage shortens the distance to that point, and closures can happen without warning.

- Negative Balance Exposure: Kalshi's own disclosures note auto-liquidation is not a guaranteed stop-loss. In gaps, extreme volatility, or thin liquidity, a position can close at a worse price and leave a negative balance you must cover.

- Funding Costs Accumulate: In a one-sided market, paying funding every 8 hours can erode returns by several percent of notional over time, separate from price movement.

- Crypto Volatility: The underlying assets swing sharply, and sudden moves can trigger liquidations faster than a trader reacts, especially without stop-loss orders.

- Product Maturity: Onshore perpetuals are new. Contracts, leverage settings, and the asset roster are still evolving and can change without notice.

- Regulatory Overhang: The CFTC approved the product, but CME Group is suing to void that approval, Kalshi's wider business faces state-level disputes, and future rule changes could still reshape how the platform runs.

- Liquidity Depth: As a new entrant, Kalshi's order books are thinner than the largest offshore venues, which can mean wider spreads and more slippage on bigger orders.

Final Thoughts

Kalshi Perpetuals are the clearest sign yet that perps are moving from the offshore margins of crypto into the regulated US core. The early volume shows real demand, and the CFTC framework gives the product legitimacy offshore venues never carried.

The design choices matter as much as the approval. Conservative leverage, capped funding, and mark-price liquidation make Kalshi's version look like institutional infrastructure rather than a high-leverage casino, which is the point.

What remains open is depth and breadth. Whether Kalshi can build books that rival offshore liquidity, and whether it can extend perpetuals beyond crypto into commodities and indexes, will decide if this is a lasting shift or an impressive opening sprint.