Crypto Adoption Statistics & Trends in 2026

Summary: Cryptocurrency adoption entered 2026 with a larger, more mature user base compared to previous years. Global ownership reached 741 million people in 2025, while Bitcoin and Ethereum remained the main entry points with 365 million and 175 million owners, respectively.

Adoption is no longer limited to spot trading. Prediction markets reached nearly $24 billion in monthly volume, tokenized real-world assets surpassed $26.71 billion in distributed value, and traditional asset perpetuals showed rising demand for crypto-based exposure to stocks and commodities.

Institutional access also expanded through ETFs and public-company treasuries. Spot Bitcoin ETFs held about $102 billion in assets, while Strategy reported 843,706 BTC and BitMine reported 5.42 million ETH, showing crypto adoption now spans retail, DeFi and public markets.

Top 10 Crypto Adoption Statistics & Trends

1. Global Crypto Ownership Reached 741 Million Users in 2025

Crypto adoption entered 2026 from a much larger base: Crypto.com estimated 741 million global cryptocurrency owners in 2025, up 12.4% from 659 million in 2024. That growth was slower than full bull-market surges, but the absolute user base now rivals the population of a large continent.

The composition also matured. Bitcoin owners rose 8.3% to 365 million, representing 49.3% of global owners, while Ethereum owners rose 22.6% to 175 million, or 23.6%. That split suggests adoption is broadening beyond Bitcoin-only exposure into smart-contract, staking, tokenization, and DeFi access.

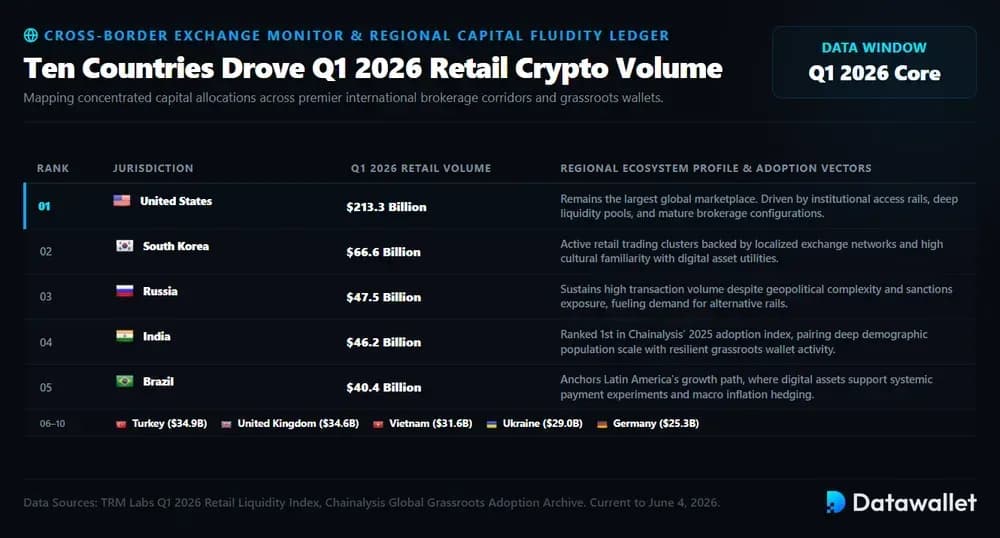

2. Ten Countries Drove Q1 2026 Retail Crypto Volume

Country adoption is best read through multiple lenses: Chainalysis ranks grassroots adoption, while TRM’s Q1 2026 data shows where retail exchange and wallet volume concentrated.

The top Q1 2026 retail-volume markets were ranked as:

- United States: With $213.3 billion in Q1 retail volume, the US remained the largest absolute market, reflecting deep liquidity, institutional rails, and mature brokerage access.

- South Korea: South Korea ranked second with $66.6 billion, showing how active retail traders, exchange infrastructure, and high familiarity with digital assets sustain adoption.

- Russia: Russia recorded $47.5 billion in Q1 retail volume, placing third despite geopolitical complexity, sanctions exposure, and persistent demand for alternative transaction rails.

- India: India reached $46.2 billion and also ranked first in Chainalysis’ 2025 adoption index, combining massive population scale with grassroots crypto usage.

- Brazil: Brazil generated $40.4 billion, reinforcing Latin America’s role as a high-growth region where crypto supports investing, payments experimentation, and inflation hedging.

- Turkey: Turkey reached $34.9 billion and remained a standout market, where currency pressure, retail trading culture, and exchange access support persistent digital-asset activity.

- United Kingdom: The UK posted $34.6 billion, indicating that regulated exchange access and institutional finance links keep developed-market adoption commercially relevant.

- Vietnam: Vietnam reached $31.6 billion and ranked fourth in Chainalysis’ adoption index, reflecting strong retail participation despite a smaller economy than most leaders.

- Ukraine: Ukraine recorded $29.0 billion, continuing its high adoption profile after years of crypto use in donations, cross-border transfers, and financial resilience.

- Germany: Germany completed the top ten with $25.3 billion, showing that European retail activity remains significant even under stricter regulatory and tax frameworks.

3. Bitcoin Ownership Reached 365 Million; Ethereum Hit 175M

Token usage still clusters around reserve assets and network tokens, but 2026 holder surveys show meaningful portfolio diversification into faster chains, stablecoins, and meme assets.

The most commonly held tokens showed this hierarchy:

- Bitcoin: Bitcoin remains the dominant holding: Crypto.com estimated 365 million BTC owners globally, while Security.org found BTC in 74% of US crypto portfolios.

- Ethereum: Ethereum had 175 million estimated global owners in 2025, and 53% of US crypto holders reported owning ETH in Security.org’s 2026 survey.

- Dogecoin: Dogecoin remained the most widely held meme coin, appearing in 25% of US crypto holders’ portfolios and preserving mainstream retail recognition.

- Solana: Solana appeared in 20% of US crypto portfolios, supported by faster settlement, consumer apps, meme trading, and expanding DeFi activity.

- USDC: USDC reached 18% US holder penetration, highlighting stablecoins’ importance for trading, cash parking, transfers, and fiat-linked crypto activity.

- Shiba Inu: Shiba Inu was held by 17% of surveyed US crypto owners, showing that meme assets still command meaningful retail attention.

- Cardano: Cardano appeared in 13% of US holder portfolios, giving it a smaller but still material position among major smart-contract tokens.

- XRP: XRP reached 11% US holder penetration, helped by long-standing brand recognition, payments narratives, and renewed ETF-related speculation.

4. Prediction Markets Hit Nearly $24 Billion Monthly Volume

Prediction markets are perhaps 2026’s clearest crypto-adjacent adoption heroes. Pew Research found combined monthly volume on Kalshi and Polymarket rose from below $5 billion in September 2025 to about $24 billion in April 2026, with sports, politics, and crypto driving participation.

TRM Labs similarly tracked prediction market volume rising from $1.2 billion in early 2025 to more than $20 billion in January 2026, alongside 800,000-plus monthly unique wallets. Growth brought scrutiny too, including suspicious-trading reviews and new insider-trading controls announced by Kalshi and Polymarket.

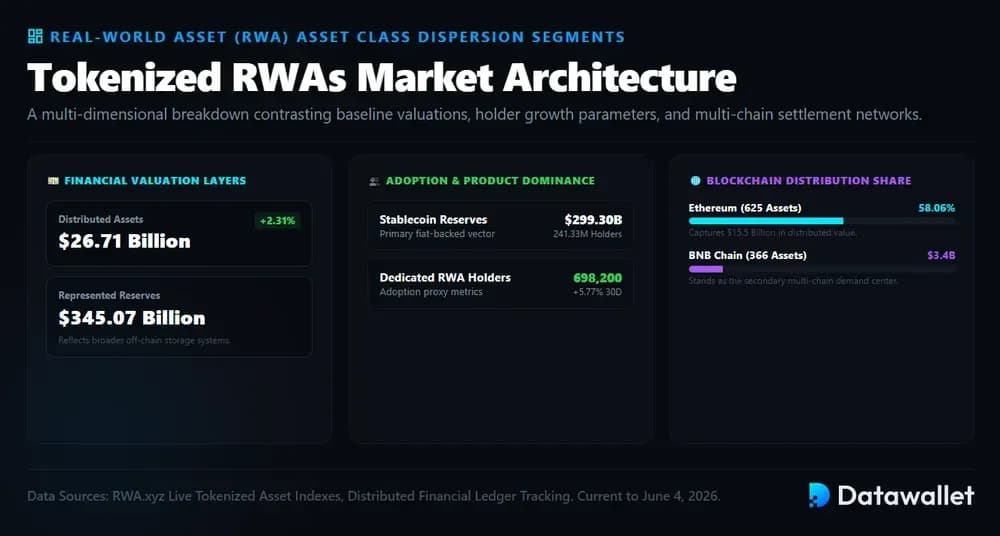

5. Tokenized RWAs Reached $26.71 Billion Distributed Value

RWA tokenization is one of the leading bridges between crypto adoption and institutional finance, with real assets, stablecoin reserves, and yield products increasingly tracked onchain.

Current RWA.xyz market data breaks down as follows:

- Distributed Value: RWA.xyz showed $26.71 billion in distributed asset value, up 2.31% over 30 days, indicating continuing net growth in tokenized real-world assets.

- Represented Value: Represented asset value was far larger at $345.07 billion, showing that tokenized exposure increasingly mirrors sizable off-chain reserves and financial assets.

- Asset Holders: Total RWA asset holders reached 698,200, up 5.77% over 30 days, a useful adoption proxy beyond headline asset value.

- Stablecoins: Stablecoin value reached $299.30 billion, while stablecoin holders reached 241.33 million, confirming fiat-backed tokens as the most adopted RWA-like crypto product.

- Ethereum: Ethereum hosted $15.5 billion in RWA value across 625 assets, giving it 58.06% market share and the clearest institutional-tokenization lead.

- BNB Chain: BNB Chain held $3.4 billion across 366 RWAs, ranking second by value and showing multi-chain demand beyond Ethereum.

6. Traditional Asset Perps Reached $31 Billion Monthly Volume

Crypto adoption expanded into synthetic exposure to stocks, commodities, indices, and foreign exchange. Crypto.com Research found onchain traditional-asset trading volume jumped 162%, from $11.8 billion in December 2025 to $31.0 billion in January 2026, led by perps tied to commodities, indices, and equities.

The broader perpetuals market remains enormous. Reuters reported perpetual futures volume reached $61.7 trillion in 2025, while CoinGecko found perp DEX monthly average volume rose to $611.57 billion in 2026. Kraken also launched tokenized equity perpetual futures for eligible non-US clients in 110-plus countries.

7. Spot Bitcoin ETFs Held About $102 Billion AUM

ETF adoption continued to normalize crypto exposure through traditional brokerage accounts. By April 2026, reported US spot Bitcoin ETF assets under management were around $102 billion, with roughly $58.5 billion in net inflows since the products launched in January 2024.

The trend extended beyond Bitcoin. Reuters reported global crypto ETFs attracted a record $5.95 billion in the week ending October 4, 2025, including $3.55 billion into Bitcoin, $1.48 billion into ether, $706.5 million into Solana, and $219.4 million into XRP products.

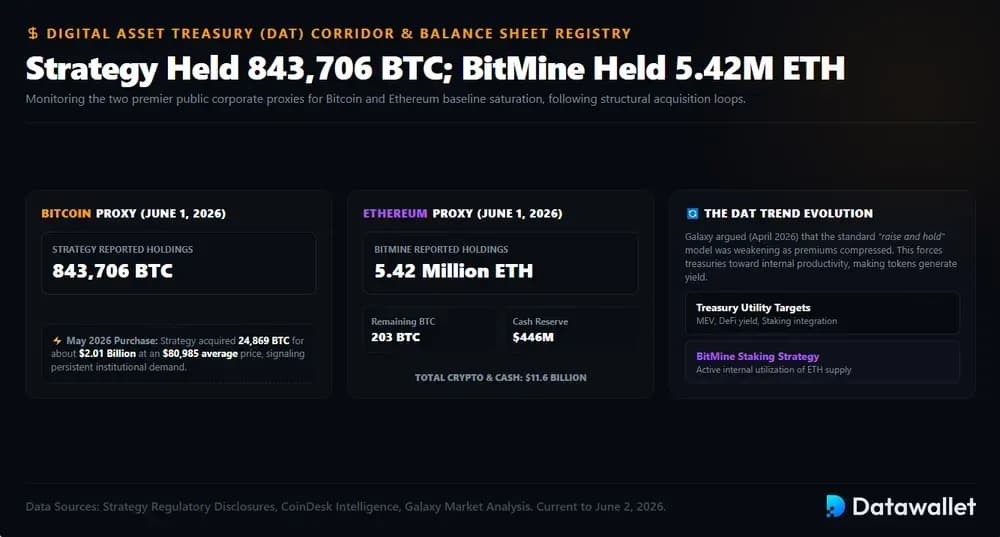

8. Strategy Held 843,706 BTC; BitMine Held 5.42M ETH

Digital asset treasury companies are another important adoption channel, converting public-equity capital into crypto exposure. Strategy reported 843,706 BTC as of June 1, 2026, while CoinDesk reported a May 2026 purchase of 24,869 BTC for about $2.01 billion at an $80,985 average price.

BitMine pushed the Ethereum version of the model. Its June 1, 2026 update reported 5.42 million ETH, 203 BTC, $446 million in cash, and $11.6 billion in total crypto and cash holdings. The company said it owned about 4.49% of total ETH supply.

The DAT trend is also evolving. Galaxy argued in April 2026 that the simple “raise and hold” model was weakening as premiums compressed, pushing treasuries toward staking, MEV, DeFi yield, and balance-sheet productivity. BitMine’s staked ETH strategy fits that shift.

9. DeFi TVL Fell To $83.3 Billion After Hacks

DeFi adoption faced a harsher 2026 risk reset. The Wall Street Journal reported DeFi TVL fell from $99.5 billion to $83.3 billion after major incidents involving Aave, KelpDAO, and Drift, showing that liquidity can retreat quickly when protocol or oracle confidence weakens.

Yet usage did not disappear. DefiLlama showed Ethereum still holding $38.842 billion in TVL, while Solana held $4.97 billion and posted heavy DEX and perpetuals activity. That split suggests adoption is moving from passive TVL toward higher-velocity trading and application usage.

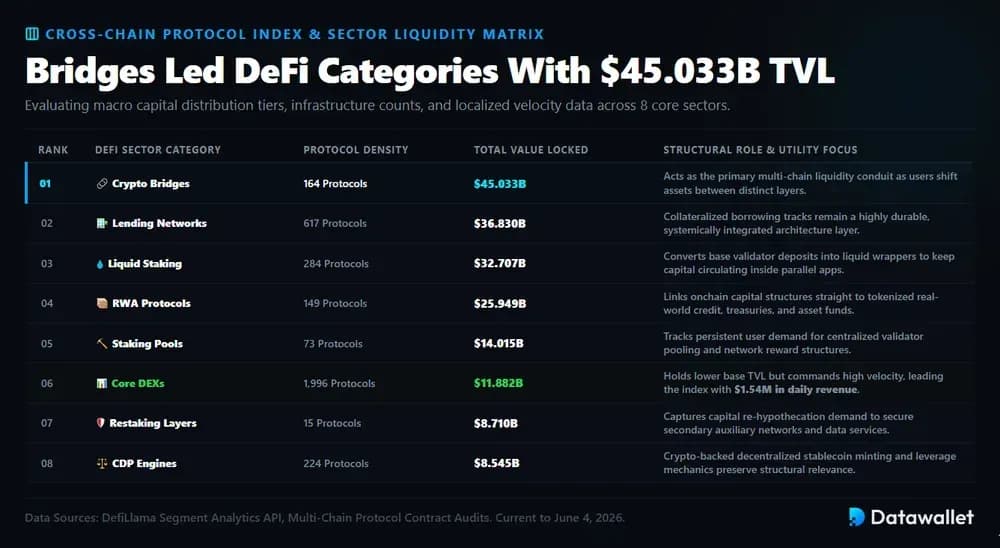

10. Bridges Led DeFi Categories With $45 Billion TVL

DeFi usage in 2026 was not only trading: DefiLlama category data shows the largest capital pools sitting in bridges, lending, liquid staking, and RWAs.

The largest DeFi sectors by current TVL were:

- Bridge: Crypto bridges with $45.033 billion across 164 protocols, reflecting the importance of cross-chain liquidity as users move assets between ecosystems.

- Lending: Lending protocols ranked second with $36.83 billion across 617 protocols, showing that collateralized borrowing remains one of DeFi’s most durable use cases.

- Liquid Staking: Liquid staking held $32.707 billion across 284 protocols, converting validator deposits into tradable tokens that can circulate through DeFi.

- RWA: RWA protocols reached $25.949 billion across 149 protocols, connecting onchain capital to tokenized treasuries, credit, funds, and other real-world assets.

- Staking Pool: Staking pools held $14.015 billion across 73 protocols, reflecting continued user demand for pooled validator access and network reward participation.

- DEXs: Decentralized exchanges held $11.882 billion across 1,996 protocols, but generated the highest listed daily revenue at roughly $1.54 million.

- Restaking: Restaking protocols held $8.71 billion across 15 protocols, showing demand for reusing staked assets to secure additional networks and services.

- CDP: Collateralized debt-position protocols held $8.545 billion across 224 protocols, keeping crypto-backed stablecoin minting and leverage structurally important.

A Brief History of Cryptocurrencies

Cryptocurrency grew from a cypherpunk payment experiment into a global financial sector covering exchanges, smart contracts, NFTs, DeFi, memecoins, prediction markets, ETFs, corporate treasuries and politically connected crypto businesses.

1. Bitcoin Proved Peer-To-Peer Money Between 2008 And 2014

Bitcoin’s first era established the core myth, technology and risks: pseudonymous money, public ledgers, real-world payments, darknet usage and fragile early exchanges.

Key milestones from the first Bitcoin cycle:

- Whitepaper: Satoshi Nakamoto published Bitcoin: A Peer-to-Peer Electronic Cash System in 2008, proposing online payments without banks or trusted intermediaries.

- Genesis: Bitcoin’s genesis block was mined on January 3, 2009, embedding a newspaper reference to bank bailouts during the financial crisis.

- Hal Finney: On January 12, 2009, Satoshi sent 10 BTC to cryptographer Hal Finney, creating Bitcoin’s first recorded person-to-person transaction.

- Pizza: On May 22, 2010, Laszlo Hanyecz paid 10,000 BTC for two pizzas, turning Bitcoin into a real-world payment asset.

- Silk Road: From 2011 to 2013, Ross Ulbricht’s Silk Road used Bitcoin for darknet commerce, linking early crypto adoption with censorship resistance and illegal markets.

- Mt. Gox: In 2014, Mt. Gox filed for bankruptcy after losing 750,000 customer Bitcoins and 100,000 of its own, damaging exchange trust.

- OneCoin: Beginning in 2014, OneCoin highlighted the fraud risks associated with cryptocurrency, with US prosecutors saying that millions of investors contributed more than $4 billion to the project led by the Bulgarian "Cryptoqueen" Ruja Ignatova.

Lesson: By 2014, Bitcoin had proven decentralized money could work, but custody failures, scams and illicit use became permanent regulatory concerns.

2. Ethereum Opened The Smart-Contract Era After 2015

Ethereum changed crypto from a payment network into programmable infrastructure. Founded by Vitalik Buterin in 2013 and launched on July 30, 2015, it let developers create tokens, decentralized applications, DAOs and financial protocols directly onchain.

The first major stress test came in 2016, when The DAO exploit drained about 3.6 million ETH and forced a controversial Ethereum hard fork that transitioned the network from proof-of-work to proof-of-stake. The split created Ethereum and Ethereum Classic, making governance a core blockchain debate.

Then came speculative infrastructure. ICOs raised about $5.6 billion in 2017, Bitcoin Cash forked from Bitcoin on August 1, 2017, and BitMEX’s 2016 XBTUSD perpetual swap introduced crypto’s defining derivatives product.

3. NFTs, DeFi And Collapse Defined The 2020s Cycle

The 2020s turned crypto into a consumer, trading and leverage machine, but also exposed how quickly speculative structures can unwind.

Key milestones from the boom-and-bust cycle:

- DeFi: Compound’s COMP launch helped ignite DeFi Summer in 2020, while Uniswap’s automated market maker model made decentralized trading mainstream.

- NFTs: NFT sales reached $25 billion in 2021, turning digital art, collectibles and gaming assets into one of crypto’s biggest consumer adoption stories.

- Terra: In May 2022, TerraUSD lost its dollar peg and Luna collapsed, showing the danger of algorithmic stablecoins and reflexive token designs.

- FTX: FTX filed for bankruptcy on November 11, 2022, after customers rushed to withdraw $6 billion in 72 hours.

- SBF: In 2024, Sam Bankman-Fried was sentenced to 25 years in prison for stealing $8 billion from FTX customers.

- Pump.fun: Launched in January 2024, Pump.fun made memecoin creation instant on Solana and became a major driver of retail speculation.

- Perps: Perpetual futures kept growing after offshore dominance, and US regulators allowed regulated crypto perps through Coinbase and Kalshi in 2026.

Lesson: By the mid-2020s, crypto had split into serious infrastructure, high-speed speculation and repeated consumer-protection crises.

4. Politics And Trump Projects Reshaped Crypto By 2026

The 2024 election made crypto politically central. The SEC approved US spot Bitcoin ETPs in January 2024, while Polymarket’s presidential election market processed billions in volume and brought crypto prediction markets into mainstream political coverage.

After returning to office, Donald Trump signed an order establishing a Strategic Bitcoin Reserve and US Digital Asset Stockpile in March 2025. His $TRUMP memecoin launched before inauguration, while Melania Trump also launched a separate memecoin.

World Liberty Financial became the most visible Trump-family crypto venture. It announced the USD1 stablecoin in 2025, sought a US trust bank license in January 2026, explored USD1 use in Pakistan, and fought Justin Sun in 2026 litigation.

How is Crypto Regulated Worldwide

Crypto regulation in 2026 is still fragmented: securities rules, commodities rules, AML registration, stablecoin supervision and tax reporting often sit with different agencies, while tax rates depend heavily on residency, holding period and transaction type.

United States

The US does not have one single crypto regulator. The SEC oversees crypto assets that qualify as securities, while the CFTC treats virtual currencies such as Bitcoin as commodities for derivatives and anti-fraud enforcement. FinCEN also requires many crypto intermediaries to register as money services businesses.

The IRS taxes digital assets when users sell, exchange, spend, receive or earn them. Crypto disposals generally create capital gains or losses, while staking, mining, airdrops and payment income may be taxed as ordinary income. Digital asset reporting is also becoming more formalized through expanded broker reporting.

For individuals, short-term crypto gains are usually taxed at ordinary income rates, while long-term gains follow federal capital gains brackets of 0%, 15% or 20%, depending on income. High earners may also owe the 3.8% net investment income tax, plus any state-level taxes.

United Kingdom

The UK is moving from AML registration toward a fuller authorization regime. The FCA currently registers crypto firms under money laundering rules and supervises financial promotions, while the Bank of England is focused on systemic stablecoins and payment-system risk.

The new UK cryptoasset regulatory regime is expected to start on October 25, 2027. Firms will be able to apply from September 30, 2026 to February 28, 2027, covering activities such as trading platforms, custody, intermediation, lending and staking.

For tax, HMRC generally treats crypto disposals as Capital Gains Tax events. From April 6, 2026, gains above the £3,000 annual allowance are taxed at 18% within the basic-rate band and 24% above it; staking or mining rewards may be income.

European Union

The EU has the clearest regional crypto framework through MiCA, but taxation remains national. Supervision involves EU bodies and local regulators.

Important EU regulation and tax points include:

- MiCA: ESMA says MiCA creates uniform EU rules for crypto-asset issuers and service providers, covering authorization, disclosure, transparency, supervision and transaction rules across member states.

- Stablecoins: The EBA supervises key parts of MiCA for asset-referenced tokens and e-money tokens, while national authorities supervise most crypto-asset service providers locally.

- Licensing: By April 2026, more than 185 crypto-asset market operators had reportedly obtained MiCA licenses, showing the framework was moving from transition into practical authorization.

- Germany: BaFin supervises crypto activities, while private crypto gains are generally tax-free after one year; short-term gains above the allowance can face income tax.

- France: AMF oversees digital-asset service providers, while occasional crypto gains are generally taxed at a 30% flat tax, with professional activity potentially taxed differently.

- Portugal: Banco de Portugal handles crypto AML registration, while crypto held over 365 days is generally tax-exempt and short-term gains can be taxed at 28%.

- Italy: OAM registers crypto operators, while 2026 crypto capital gains taxation is widely reported at 33%, with separate treatment for some euro-denominated e-money tokens.

Asia

Asia ranges from strict bans to highly regulated hubs. Tax treatment is equally split between income-tax systems, capital-gains exemptions and high flat taxes.

Major Asian regulatory approaches include:

- Japan: The FSA regulates crypto-asset exchange service providers. Crypto gains are generally treated as miscellaneous or business income, with current combined rates reaching roughly 55% before proposed reform.

- Singapore: The MAS licenses digital payment token providers under strict standards. IRAS generally does not tax capital gains, but trading income can be taxable depending on facts.

- India: FIU-IND brings virtual digital asset providers under AML rules. Crypto gains are taxed at 30%, with 1% TDS on qualifying transactions and limited loss-offset flexibility.

- South Korea: The FSC and FIU oversee virtual-asset platforms. Crypto taxation has been delayed repeatedly, with a 22% tax on gains currently scheduled for January 1, 2027.

- Hong Kong: The SFC licenses virtual-asset trading platforms and intermediaries. The IRD is preparing CARF reporting, while business crypto profits can be taxable under profits-tax principles.

- China: The PBOC maintains one of the strictest regimes, treating virtual-currency business activities as illegal financial activity while continuing to support the digital yuan.

Rest of the World

Outside the US, UK, EU and Asia, crypto rules are increasingly built around licensing, AML reporting, exchange authorization and tax transparency.

Important global examples include:

- Canada: The CSA coordinates securities regulation, while FINTRAC handles AML registration. The CRA taxes crypto as business income or capital gains, depending on activity.

- Australia: ASIC applies financial-services law where digital assets are financial products, while AUSTRAC handles exchange AML registration. The ATO generally treats crypto as a CGT asset.

- UAE: Dubai’s VARA regulates virtual assets, while federal and free-zone regulators cover other activities. Individuals generally face no personal income or capital gains tax on crypto.

- Brazil: The Banco Central do Brasil is implementing VASP rules from February 2026. Crypto gains can be taxable, with reporting handled through Receita Federal rules.

- South Africa: The FSCA licenses crypto asset service providers. SARS says normal income tax rules apply, and CARF takes effect from March 1, 2026.

- Switzerland: FINMA regulates crypto services using risk-based financial-market rules. Private capital gains are generally exempt from income tax, but crypto is usually declared for wealth-tax purposes.

What are the Risks of Cryptocurrencies?

Cryptocurrencies can offer ownership, liquidity and open access, but users face unusual risks from volatility, fraud, custody failures, regulation, leverage and irreversible transactions.

The biggest cryptocurrency risks include:

- Volatility: Crypto assets can move sharply in short periods, and FINRA warns they are often extremely volatile, speculative and difficult to value reliably.

- Scams: Fraudsters exploit crypto popularity through fake platforms, romance scams, impersonation, phishing and guaranteed-return pitches, according to SEC investor warnings.

- Hacks: Chainalysis reported over $2.17 billion stolen from crypto services through various smart contract exploits by mid-2025, already exceeding all of 2024’s service-theft total.

- Custody: Losing private keys can mean permanent loss, while exchange or custodian failures may leave users without full insurance or recovery protection.

- Regulation: Crypto users can interact with unregistered or lightly supervised entities, meaning investor protections may be weaker than in regulated securities markets.

- Liquidity: Some tokens trade actively only during hype cycles, leaving holders exposed to slippage, failed exits or collapsing prices when demand disappears.

- Leverage: Perpetual futures, margin trading and DeFi borrowing can amplify gains, but forced liquidations can wipe out positions during fast market moves.

- Stablecoins: Stablecoins can lose pegs, depend on issuer reserves and face redemption stress, making them less risk-free than their dollar labels suggest.

- Crime: Chainalysis estimated illicit crypto addresses received at least $40.9 billion in 2024, with scams, stolen funds and ransomware remaining major concerns.

- Taxes: Crypto sales, swaps, payments, staking rewards and airdrops can trigger taxable events, creating reporting burdens and penalties for inaccurate filings.

Crypto Adoption Projection

The adoption case is increasingly institutional rather than speculative. BlackRock’s Larry Fink and Rob Goldstein argue tokenization can bridge traditional and digital markets, while NYSE President Lynn Martin says tokenized securities infrastructure must preserve investor trust, transparency and protections as capital markets move onchain at scale.

Consumer adoption should shift from exchange sign-ups to usable payments apps and identity tools. Coinbase’s Brian Armstrong listed stablecoins, payments and “bringing the world onchain” as 2026 priorities, while Binance’s CZ warned weak privacy still blocks everyday and institutional crypto use in practice today at scale.

Payment adoption will likely be contested, not linear. Federal Reserve Governor Christopher Waller calls stablecoins useful payment competition, while Bank of England policymaker Megan Greene expects tokenized deposits to overtake them. Ripple’s Brad Garlinghouse frames stablecoins, tokenization and AI as institutional adoption rails for finance.

Overall, the projection is broader but slower adoption: ETFs and tokenized securities should onboard institutions, stablecoins should test payments and corporate treasury workflows, and privacy, regulation, interoperability and consumer protection will decide whether crypto becomes everyday infrastructure rather than a parallel speculative market for specialists.

Final Thoughts

Crypto adoption in 2026 is broader than ownership alone. With 741 million global owners, spot Bitcoin ETFs approved in the US, and Ethereum ownership growing faster than Bitcoin, access is becoming more mainstream.

The next phase is about real utility. Tokenization, stablecoins, DeFi, prediction markets and digital asset treasuries show crypto moving from speculative cycles toward settlement, payments, market access and corporate balance-sheet strategy.

Still, adoption depends on trust. Hacks, scams, tax complexity, custody failures and uneven regulation remain major barriers, so the winners will likely be products that feel safer, simpler and more useful than traditional alternatives.

Our Methodology

Our research combines crypto ownership reports, exchange-volume data, ETF flows, DeFi dashboards, RWA datasets, regulatory materials, tax authority guidance, institutional research and reputable news reporting to evaluate crypto adoption statistics and trends in 2026.

How the data was compiled:

- Ownership Data: Used Crypto.com, Security.org and adoption-focused research to estimate global crypto users, Bitcoin ownership, Ethereum ownership and portfolio-level token penetration.

- Country Rankings: Compared Chainalysis-style adoption research with TRM Labs retail-volume data to identify the countries showing the strongest crypto usage and transaction activity.

- Token Trends: Reviewed ownership surveys, market trackers and token-specific datasets to understand which crypto assets are most widely held by retail users.

- DeFi Dashboards: Used DefiLlama and category-level protocol data to evaluate TVL, leading DeFi sectors, chain activity, lending, DEXs, bridges, staking and restaking.

- RWA Research: Used RWA.xyz, issuer data and institutional commentary to measure tokenized real-world asset growth, stablecoin scale, holder counts and blockchain distribution.

- ETF Data: Reviewed ETF flow reports, asset-management updates and market coverage to assess how spot Bitcoin, Ethereum and altcoin ETFs are expanding access.

- Treasury Companies: Used Strategy, BitMine, Galaxy and reputable news coverage to compare digital asset treasury holdings, corporate balance-sheet strategies and staking activity.

- Regulatory Sources: Reviewed materials from the SEC, CFTC, IRS, FCA, HMRC, ESMA, EBA, MAS, FSA, FINMA and other authorities for jurisdiction-specific rules.

- Risk Review: Compared official investor warnings, enforcement actions, hack reports, exchange failures, stablecoin incidents and DeFi exploits to explain the main risks users face.

Snapshot Caveat: Many statistics come from live dashboards or fast-moving reports, so values can change as prices, flows, ownership, TVL, regulation and liquidity conditions shift.

Frequently asked questions

.webp)